Market Analysis

The market’s focus has been on S. America’s soybean prospects and the ongoing US/China trade talks that had a positive vibe until this week. A possible Chinese step-back over a previously negotiated intellectual property issue prompted a renewed US threat of increasing the tariff on $200 billion of Chinese exports to the US to 25% beginning on Friday. With the Chinese still scheduled to arrive in DC later this week, some optimism has surfaced that the talks may still get back on track for a solution.

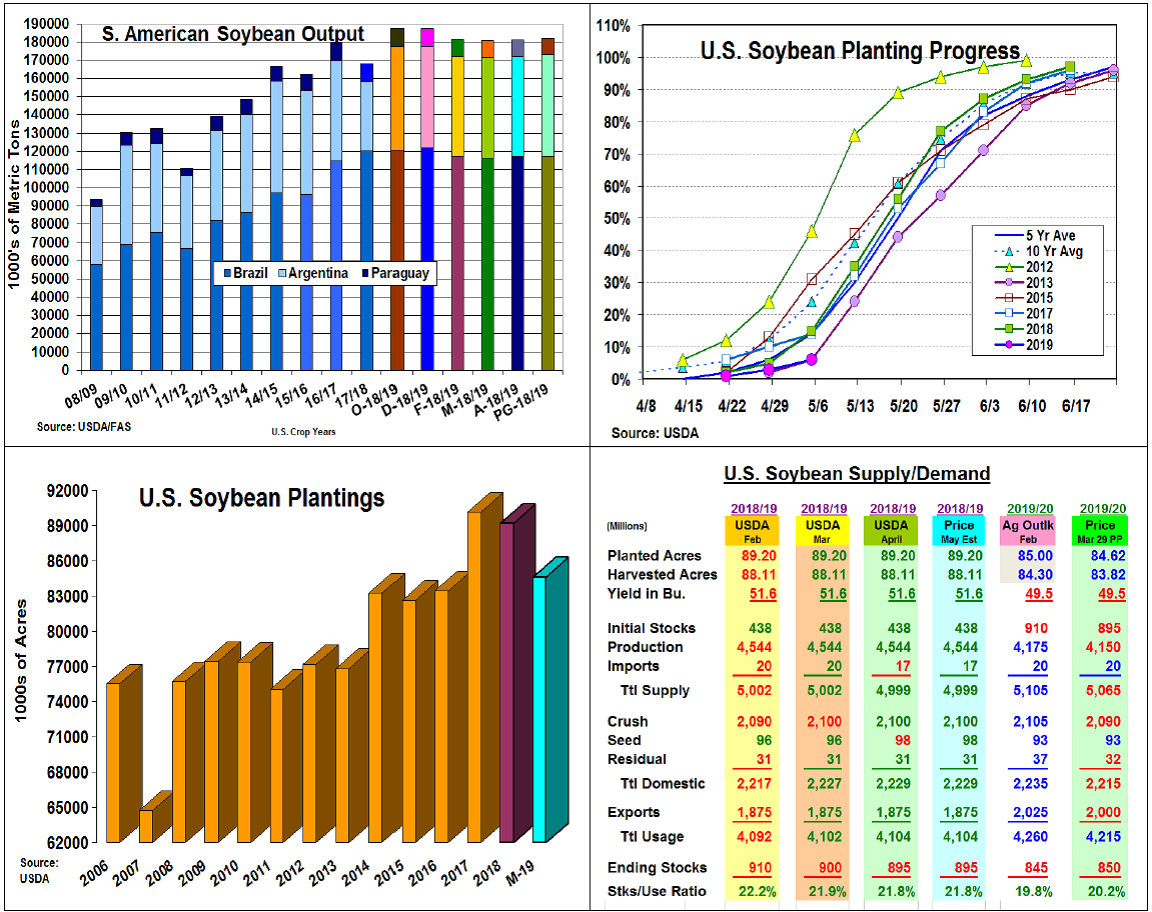

After dryness impacted early planted soybeans in Brazil in December and early January, renewed rains across both counties stabilized Brazil’s output at 117 mmt and likely will boost Argentina crop 1 mmt last month and 1 mmt this month. Overall, S AM output will still be down 5 mmt from October estimates, but 2 mmt higher than 2016/17’s previous S Am high level suggesting minimal impact on world supplies this month.

This spring’s cold & heavy rainfall across the Midwest’s growing areas have delayed corn, spring wheat, and soybean plantings. This week’s US bean seedings were just 6%. This was only a 3% increase from last week and ties 2019 with 2013’s slowest first week in May planting level in the data. Soybeans heartiness to heat & dryness has prompted producers to switch to beans in the past if plantings remain delayed. 2019’s seedings will need to mimic 2013’s pace to generate much price excitement.

March’s monthly US Fats and Oils soybean crush of 179.5 million bu. keeps the US pace on target to hit DC’s yearly forecast. Soybean shipments have slipped behind, but the US/China talks remain this demand’s biggest factor. The World Board may just leave demand & stocks unchanged. The USDA normally uses its Ag Outlook de-mand & yield levels, but they must use the US planting intentions for 2019/20 balance table. This suggests US 2019/20 bean stocks likely begin at about 850 million bu.

(Click on image to enlarge)

What’s Ahead

A production problem will need to occur someplace in the world for a major price improvement in soybean prices given the current US and S. American supplies. China’s African Swine Fever may also reduce this major buyer’s protein demand if this disease outbreak continues. Use 25-40 cent price recoveries to have 80-85% of your 2018/19 crop marketed and begin 15-20% of 2019/20 marketings.

Comments

Log in or sign up to join the conversation.