Market Analysis

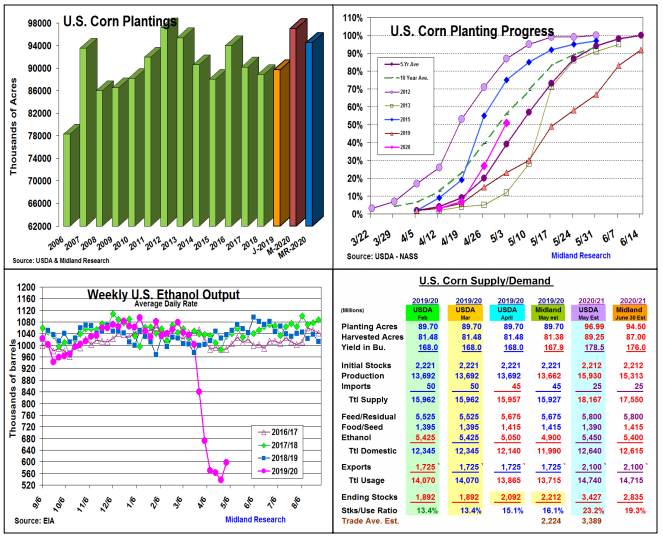

The ongoing effect of the coronavirus on energy, meat and food prices, and this spring’s US planting weather have been the main factors for the corn (CORN) market over the past 3-4 weeks. Storage concerns on the expiring US futures oil contract leading to the first-ever negative price close in this market and higher Covid-19 infections at US meatpacking plants causing closures and reduced slaughter rates were major factors impacting the corn market. This year’s strong early start to America’s planting season vs. 2019’s extremely delayed period also has hung over corn prices.

As of May 3, this year’s corn planting pace is nearly 2 ½ times higher than last year at 51% and 12% stronger than the 5-year average. Like 2019, the WCB has had a quicker start with IA (78%), MN (76%) & NE (61%) leading the way vs. the ECB. However, IL (56%) & IN (33%) seedings are 5 & 10 times 2019’s paces for early May. Freezing temps this weekend across the N & E US may have the biggest impact on 2020’s corn prospects to date.

The rapid decline in US ethanol output because of the widespread US stay-at-home directives cutting US gasoline use has been a major negative factor. After dropping about 50% of last year’s pace, ethanol’s 11.4% rise this week and 2 million barrel drop in US stocks (in 2 weeks) are encouraging signs as many states are beginning to relax their restrictions. However, this old-crop demand could be sliced another 150-200 million bu. Reduced slaughtering rates has prompted concern about corn’s feed demand, but feed inefficiencies of higher weights and corn substitutions for reduced DDG supplies suggests no change in this demand this month. A pick-up in sales and dryness slicing Brazil’s 2 nd crop likely keeps US 2019/20 exports unchanged.

Traditionally, the USDA’s May new-crop corn balance sheet utilizes their Ag Outlook demand, yield ideas & their March plantings. With a higher old-crop carryover & 97 million seedings, 2020/21 stocks could balloon over 3.4 billion bu, the highest since the 1980s. The need to switch to other 2020 crops remains paramount for corn’s price.

What’s Ahead:

Even with a 2.5 million lower planting level, a yield near the highest of the last three years and the USDA’s 1 billion bu. higher 20/21 demand idea, growing season weather concerns both in the US & S America will be needed for a major upturn in corn prices. Utilize July values in $3.30-$3.35 range to up old-crop sales to 75%. Also, begin 2020/21 Dec sales with 15% hedge in the $3.44-$3.49 range.

Comments

Log in or sign up to join the conversation.