By Eli Levy of Cannon Trading

FOMC Decision Day · Warsh's First Meeting

A record Dow, a cracking AI trade, and a Fed chair who may scrap the dot plot — all colliding at two o'clock.

Tuesday split in two: the Dow cleared 52,000 for the first time as crude crashed 5%, yet the S&P and Nasdaq closed red with the chips. Today Kevin Warsh runs his first FOMC — and is expected to withhold the projections the entire rates market trades off.

S&P 500

7,511.35

−0.57%

Nasdaq

26,376

−1.15%

Dow

51,999.67

+0.64%

WTI

$76.71

−5.0%

Gold

$4,353

+0.0%

US 10Y

4.44%

−3bp

VIX

16.41

+1.3%

TODAY FOMC statement 2:00pm ET · Warsh presser 2:30pm · HOLD 3.50–3.75% priced ~97% · the tell: is the dot plot withheld? · S&P futures 7,516, flat into the print

ACT I Trade Today

What's the setup, and what do you do before the bell.

02

The 90-Second Read

REGIME

Rotation, Frozen

Pre-FOMC

What changes it: a balanced Warsh presser that doesn't slam the door on cuts lets the oil-down relief broaden and the AI complex steady. A chair who deletes the dots and talks tough on a still-4% headline is the air-pocket the calm index isn't hedged for. The other live wire is the Iran signing — agreed is not delivered.

It was a rotationTuesday was not a rally. The Dow printed a record near 52,000 as oil collapsed, but the S&P slipped 0.57% and the Nasdaq Composite fell 1.15% as the AI complex broke — Intel, Lumentum and Monolithic Power each down 8%+. Financials rose 1.5% while Technology lost 2.3%. Money rotated; it did not leave.

The Fed, not the rateA hold at 3.50–3.75% is ~97% priced. The story is communication: CNBC reports Warsh is expected to withhold the dot plot at his first meeting. No projections means the 2:30 presser is the only signal — an unscripted new chair as the entire event.

Oil did the Fed's jobWTI crashed 5% to the mid-$76s and Brent broke below $80 after the U.S. agreed to let Iran sell oil immediately. It is the cleanest disinflation lever into a hot-CPI meeting — but Barclays keeps a $100 forecast and crude's own vol gauge jumped 11%.

The calm is a costumeThe VIX sits at a sleepy 16-handle, yet Nasdaq volatility (VXN) spiked to 26.95. Headline calm is masking a tech-vol storm under the surface. Crypto leaked too — Bitcoin back to ~$65.8k.

Frozen into the printS&P futures sit at ~7,516, dead flat after the close. Desks flag the prior-high zone as overhead and the ~7,450 area as the line that, if lost, accelerates the tech unwind. Yields slid into the meeting, the 10Y at 4.44%.

03

The Scoreboard

Every quoted price has its one home here: the levels grid, then the sentiment & flow gauges, the flow read, and yesterday's calls graded. Index rows are the Tuesday June 16 close; commodities, vol, FX and crypto are the latest live prints (CNBC, evening ET).

Market | Last | Chg | Note |

|---|---|---|---|

S&P 500cash, Jun 16 close | 7,511.35 | −0.57% | Red as chips cratered; prior close 7,554 |

Nasdaq Compositecash, Jun 16 close | 26,376.34 | −1.15% | AI/semis led the tape lower |

Nasdaq-100cash, Jun 16 close | 29,968.13 | −1.89% | Worst of the majors; futures 29,999 |

Dowcash, Jun 16 close | 51,999.67 | +0.64% | Record — first print above 52,000 |

Russell 2000cash, Jun 16 close | 2,939.20 | −0.87% | Small-caps with the risk-off, not the Dow |

WTI crudelatest | $76.71 | −5.0% | Iran-supply shock; Brent below $80 |

Gold / Silverlatest | $4,353 / $70.12 | +0.0% / −0.1% | Haven bid holds on a down-tech day |

Nat gaslatest | $3.262 | +3.7% | The one commodity bid as oil fell |

US 10Y / 2YJun 16 close | 4.443% / 4.058% | −3 / −1 bp | Yields eased into the Fed; 2s10s +38 bp, 5Y 4.17%, 30Y 4.95% |

DXY / EUR / JPYlatest | 99.56 / 1.161 / 160.5 | −0.1% | Dollar soft; yen pinned near 160 |

Bitcoin / Etherlatest | $65,784 / $1,796 | −1.2% / −1.5% | Risk-sensitive complex leaked with tech |

VIX / VXN / Oil-VIXlatest | 16.41 / 26.95 / 53.1 | +1.3% / +4.0% / +11% | Index calm; Nasdaq and crude vol screaming |

Sentiment & flow gauges

Gauge | Reading | Read |

|---|---|---|

CNN Fear & Greed | ~41 | FEAR — the tape never bought the relief at the gauge level (last published) |

AAII bulls / bears | 30.4 / 47.7 | Retail washed-out bearish into the decision |

NAAIM exposure | ~79 | Active managers still net-long — room to cut, not add |

CBOE put/call | ~1.1 | Hedging finally building, unlike last week's complacency |

FedWatch — June hold | ~97% | Hold near-certain; the debate is the dots and the 2026 tail |

Sentiment gauges are the latest published readings (JS-rendered sources); the market levels above are live, page-verified.

The flow read — the calm is composition, not consensus

For a week the divergence was “saying vs doing” — cautious surveys, complacent options. Tuesday moved that divergence inside the index. A 16-handle VIX says all-clear, but VXN at 27 and a 2.3% drop in the Technology sector say the AI trade is being de-risked hard while financials and the Dow hold the headline up. The S&P looks calm because two engines are pulling in opposite directions, not because the market agrees on anything. Either Warsh steadies the tech tape this afternoon, or the rotation becomes a drawdown the index print has been hiding.

Yesterday's calls, graded

HIT

“Oil is the disinflation lever.” WTI fell another 5% to the mid-$76s and Brent broke below $80 — the cleanest easing of the inflation backdrop into the meeting.

FADED

“The everything-rally rolls on.” It didn't. The relief narrowed to a rotation — the Dow made a record while the S&P and Nasdaq closed red. The broad bid we flagged as “leaning into the decision” thinned to the value side only.

HIT

“Gold's quiet dissent.” On a day the AI complex broke, gold still held its bid in the $4,350s. The debasement trade refused to unwind — again.

OPEN

“The hawkish surprise is the only un-owned outcome.” Live at 2:00 PM today. A 16-VIX and ~97% hold odds still leave the 2026-hike tail under-hedged.

04

Calendar & Scenario Map

Time (ET) | Event | Why it matters |

|---|---|---|

8:30 AM | Housing starts / building permits | Second-tier; a soft print feeds the slowdown case ahead of the Fed |

10:30 AM | EIA crude inventories | First inventory read since the Iran deal — can extend or fade the oil crash |

2:00 PM | FOMC statement & (maybe) projections | Hold ~97% priced; the surprise is whether the dot plot appears at all |

2:30 PM | Warsh press conference | His debut and, with dots possibly withheld, the entire signal |

Thu | Weekly jobless claims | The labor data the lone-dove cut case hinges on |

Binary 1 — the FOMC decision2:00 PM · consensus HOLD ~97% · prior 3.50–3.75%

SOFT — relief broadens

Hold delivered; Warsh frames the oil drop as doing the Fed's tightening for it and keeps optionality open. Even with no dots, a balanced tone lets tech steady and the rotation turn into a broadening. Yields and the dollar drift lower; the peace-and-disinflation trade resumes.

HOT — the air pocket

Hold paired with a chair who won't rule out a 2026 hike against a 4% headline — or a withheld dot plot read as hawkish opacity. Front-end yields back up, the AI unwind from Tuesday extends, and the index can no longer hide the rotation. This is the un-hedged tail.

Binary 2 — the Iran signingthis week · Switzerland · oil −5% on the framework

SOFT — signed & delivered

The framework is formalized, Iranian barrels start clearing, and crude holds sub-$80. The disinflation lever stays pulled, giving Warsh cover and keeping the energy leg of CPI quiet.

HOT — a slip at the table

Agreed is not delivered. A delay or a walk-back re-bids crude in the same window as the decision — exactly the re-arming of the oil-inflation trade that crude's 11%-higher vol gauge is already pricing.

05

Levels & Structure

The structural story is the split. The S&P closed 7,511 with futures a hair above it; 7,600 is the overhead the Dow-led bid keeps testing, while the ~7,450 area is the shelf that, if it breaks, lets the chip-led unwind set the index direction. The cleaner damage is in the Nasdaq-100 at 29,968 — the AI complex is where Tuesday's selling concentrated and where a hawkish Warsh would bite first. In crude, WTI's mid-$76s sits on the $75 line with ~$72 the next air pocket below; gold holds its bid with the 10Y at 4.44% as the macro anchor underneath it all.

Two cross-checks frame the day. Breadth is the first: the Dow's record sits on a Russell 2000 that fell with the chips, so the rally's leadership is a handful of value names, not the broad market — a narrow record is a fragile one. The second is the dollar at 99.6 and a 2s10s curve at +38 basis points; neither is flashing stress, which is why a hawkish presser would have room to move both before the tape forces the Fed's hand. Until 2:00 PM, the levels are a coiled spring: the index can hold its range on the value bid, but the direction out of it belongs to Warsh.

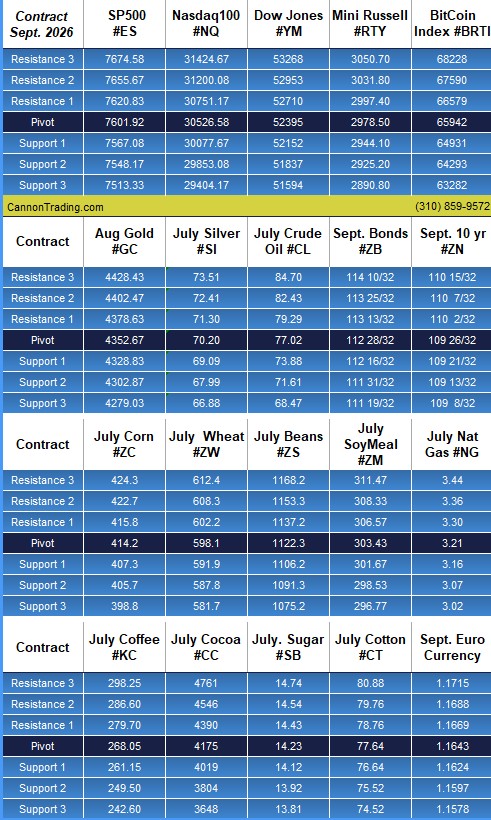

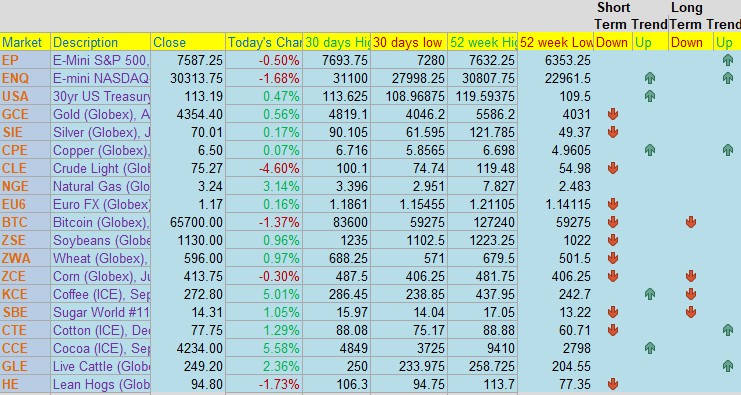

Cannon Daily Levels — key support/resistance grid (1 of 2).

Cannon Daily Levels — key support/resistance grid (2 of 2).

ACT II The Read

Who's driving the tape, and why.

06

Institutional Positioning

New or moved voices only. Each named voice gets one full treatment here; everywhere else is a name-reference. Standing calls with no fresh note sit in the Desk Shift Tracker below.

Michael Hartnett· BofA · Flow ShowFLOW

Hartnett's June 13 Flow Show kept its Bull & Bear Indicator on a SELL signal for a fourth straight week, with a record +$12.3B into tech funds in the week to June 10. That inflow is the problem: the crowd that chased the AI trade into Friday met a 2.3% tech drawdown on Tuesday. He still frames 2026 as a 1994 analog — easing into a jobless recovery that ends in abrupt hikes — the template that fits a Warsh who deletes the dots.

Savita Subramanian· BofA · Equity & Quant StrategyTAKE PROFITS

Subramanian told clients on June 10 to take profits, flagging that roughly 70% of her bear-market precursor signals have now triggered, with a year-end S&P target of 7,100 — below where the index already trades. Tuesday's narrow, rotation-only tape is exactly the deteriorating-leadership signal her checklist watches for.

Scott Chronert· Citi · US Equity StrategyRAISED

The other side of the desk: Chronert lifted Citi's year-end target to 8,100 from 7,700, built on earnings rather than multiples — ~$350 of 2026 S&P EPS and “high confidence in continued beats.” His bull case is that the AI capex cycle keeps compounding earnings straight through the volatility that hit the chips on Tuesday.

Ed Yardeni· Yardeni ResearchSTREET HIGH

Yardeni holds the Street's highest target at 8,250, leaning on the same productivity-and-earnings “Roaring 2020s” thesis. With the index near 7,500, his and Chronert's calls frame the bull ceiling that a clean Warsh hold would let the tape work toward.

07

Desk Shift Tracker

All tracked voices with a read this cycle, sorted by influence score. DARK = a high-score voice whose silence into FOMC week is itself the signal.

Voice | Firm | Score | Shift this cycle |

|---|---|---|---|

Rick Rieder | BlackRock | 7.95 | DOVE Lone holdout still calling two 2026 cuts — increasingly offside the hawkish repricing |

Jeffrey Gundlach | DoubleLine | 7.65 | HAWK Warns the next CPI “starts with a four”; cuts off the table — see Macro |

Tony Pasquariello | Goldman Sachs | 7.50 | DARK No fresh note into Warsh's first meeting — conspicuous from the flow desk |

Michael Hartnett | BofA | 7.35 | FLOW SELL signal, 4th week; record tech inflows — see card |

Torsten Slok | Apollo | 7.10 | HAWK June 15: markets now pricing hikes, not cuts — see Macro |

Scott Rubner | Citadel Sec. | 6.70 | DARK No July-inflows note this run — notable given the seasonal window he usually flags |

Mike Wilson | Morgan Stanley | 6.40 | HELD 7,800 target; “rolling recovery” rotation thesis — Tuesday's value bid fits it |

Jan Hatzius | Goldman Sachs | 6.35 | HAWK Scrapped all 2026 cuts; ~20% odds of a hike — see Fed Watch |

David Kostin | Goldman Sachs | 6.20 | HELD 7,600 year-end (Kostin/Snider); no fresh revision |

Tom Lee | Fundstrat | 6.15 | BULL “The bottom is in”; sees the backdrop helping earnings |

Andrew Tyler | JPMorgan | 5.90 | DARK No fresh tactical note in a week with both FOMC and a moving oil tape |

Savita Subramanian | BofA | 5.55 | BEAR Take profits, 7,100 — see card |

Scott Chronert | Citi | 5.40 | RAISED 8,100 on earnings — see card |

Ed Yardeni | Yardeni Res. | 5.30 | BULL Street-high 8,250 — see card |

08

Macro Pressure Map

Oil — the lever and its tail. The U.S.–Iran framework to let Tehran sell oil immediately knocked WTI down 5% and Brent under $80, the single largest disinflationary input into today's meeting. But the move is not clean: Barclays is keeping its $100 crude forecast on the view the deal “won't solve supply overnight,” and crude's own volatility gauge jumped 11% on the same day spot fell — the options market is pricing a re-bid, not a peace dividend.

Inflation — still the binding constraint. Apollo's Torsten Slok, in his June 15 Daily Spark, argues the market has crossed from debating cuts to pricing hikes, with tariffs, high oil and AI-capex demand keeping core inflation sticky above 3%. DoubleLine's Jeffrey Gundlach (see Tracker) is blunter, warning the next CPI handle “starts with a four.” That is the wall every dovish target on the Street keeps running into.

Growth & the dollar. The split runs through the growth call too: BCA's Peter Berezin still carries recession odds near three-in-four, while Fundstrat's Tom Lee says the bottom is in. The dollar, meanwhile, drifted to 99.6 — soft enough to ease financial conditions at the margin, one more reason a hawkish Warsh would land against the grain of the tape.

09

Portfolio Positioning

Tuesday was a live demonstration of the rotation the bulls have been promising: out of mega-cap AI, into financials, value and the Dow. Financials gained 1.5% and the Dow made a record while the chip complex — Intel, Lumentum, Monolithic Power, Coherent — fell 7–9%. For allocators, the question into the Fed is whether to treat that as the start of a healthy broadening or the first crack in the only leadership the market has had.

The pressure point remains the private-AI complex. Michael Burry said he is tempted to bet against SpaceX but is passing on the expensive options — a telling hesitation, since even a famous bear won't pay up to short the most crowded private name, while an analyst pegs EchoStar's value at $161-plus a share largely on its SpaceX stake. The AI-adjacent trade is where conviction and valuation are most stretched, and where a hawkish surprise would do the most damage. Positioning into 2:00 PM is defensive by survey (AAII bears at 48%) but still long by exposure (NAAIM ~79) — the gap that a decisive Warsh resolves in one direction or the other.

10

Fed Watch

The rate is a non-event: CME FedWatch puts a hold at 3.50–3.75% near 97%. Everything that matters is in the communication. CNBC reports that Kevin Warsh — in his first meeting since taking the chair on May 22 — is expected to withhold the dot plot, breaking from the Fed's practice of publishing the rate-path projections. Strip out the dots and there is no anchor for the front end; the 2:30 presser becomes the only guidance, delivered live by a new chair on day one.

The desk consensus has hardened hawkish underneath that hold. Goldman's economics team (Jan Hatzius, see Tracker) has scrapped its 2026 cuts entirely and now puts roughly one-in-five odds on a 2026 hike; JPMorgan carries a hike into its 2027 baseline; and prediction markets have pushed 2026-hike odds toward the coin-flip. The lone major-bank holdout is Citi's Andrew Hollenhorst, still calling cuts in September, October and December — contingent on a labor market that has not yet cracked. Against that backdrop, the market has priced the decision as resolved and the path as benign. Both of those are exactly what an unscripted Warsh, with no dots to hide behind, could unsettle. For a market that spent the week pricing the Iran peace and looking past the Fed, the asymmetry is uncomfortable: the good news is already in the tape, and the risk is still on the calendar.

ACT III The Edge

What the consensus is missing.

11

What the Consensus Is Missing

The index calm is a composition trick, not a verdict

A 16-handle VIX is being read as a market that has made its peace with the decision. It hasn't. On the same tape, Nasdaq volatility ran to 27 and the Technology sector fell 2.3% while financials and the Dow held the index up. The S&P looks quiet only because two halves are canceling out — a violent AI de-risking masked by a value bid. The hedge nobody is buying is for a tech-led air pocket that the headline vol says can't happen, precisely because the headline vol is averaging away the storm underneath it.

Deleting the dots is itself the surprise

The debate has been which way the dot plot leans. The market hasn't priced the possibility that there is no dot plot at all. If Warsh withholds the projections, he removes the single reference point the entire rates curve is built around and hands all of the signal to an unscripted presser on his first day. That is not a dovish or hawkish event — it is a regime change in how the Fed communicates, and a ~97% “hold, non-event” market is positioned for neither the uncertainty nor the headline risk it creates.

The crude options market is already fading the Iran deal

Equities took the 5% oil crash as a clean disinflation win. The people who actually hedge crude did the opposite: oil's volatility gauge jumped 11% on the very day spot collapsed, and Barclays kept its $100 forecast. That is the options market pricing a re-bid, not a peace dividend — a tell that the “agreed but not delivered” signing risk is live in the same window as the Fed. The disinflation lever everyone is leaning on has a fat tail that only one market is paying to insure.

Comments

Log in or sign up to join the conversation.