Market Analysis

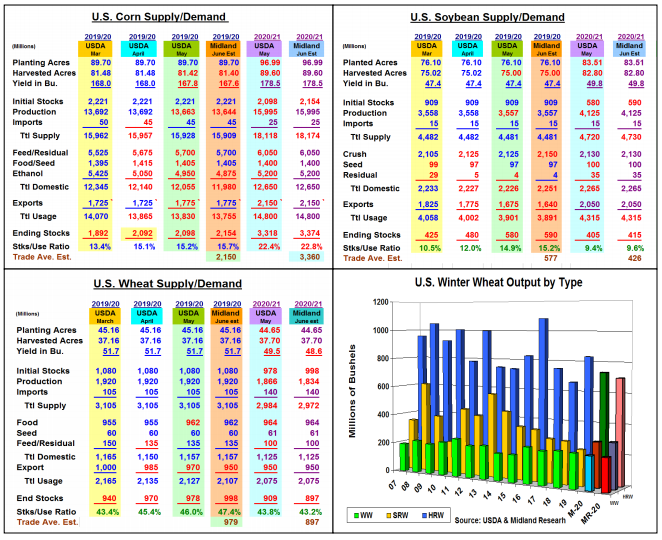

After May’s major US & World new-crop supply/demand updates, the upcoming June 11 monthly balance sheet changes traditionally are modest. Despite last year’s dramatic cut in the US 2019/20 corn yield (-10 bu. to 166), we don’t expect any changes in either corn (CORN) or soybeans (SOYB) new-crop output levels as the USDA awakes the upcoming June 30 US acreage report. Recent domestic monthly crush and processing data along the current US export activity could however make some changes in old-crop US demand levels. The USDA will also issue their 2nd US W. Wheat crop (WEAT) report later this week.

First, the USDA could shrink the US old-crop corn crop (15-19 mil bu.) because of lost ND output. Next, April’s modest 245 million ethanol corn use because of better plant efficacies suggests this demand could be shaved 75- 100 million bu. even with last week’s US biofuel output at 73% of May 2019 rate. Recent sales suggest the USDA forecast is attainable, but shipments need to pick-up. With no feed or export changes, a 2.154 billion bu. 19/20 stock level is expected that is carried over to 20/21 year.

April’s record US soybean crush of 183.4 million bu (6 of the 1st 8 months) suggests this demand could be raised 25 million to 2.15 billion bu. However, Chinese tensions and the current remaining weekly export pace of over 28 million bu. suggest this oversea demand maybe cut 35 million bu. resulting in 590 million 2019/20 stocks level.

This spring’s freeze and ongoing drought in the Western Plains suggests a possible further drop in hard red’s crop to 700 million bu. while soft red is up 3 million and white wheat is down 2 million bu. from last month. Overall, June’s US winter wheat crop could be 1.223 billion bu. Slow US old-crop shipments suggest a 20 million jump in 2019/20 ending stocks countering a smaller US new-crop output. However, the Black Sea and the EU wheat prospects are big price factors this time of year to keep an eye on.

What’s Ahead:

Recent Chinese bean purchases and some US crop concerns have advance corn & soybean prices into previous sales level. Utilize the current July corn price above $3.30 to up old-crop sales to 75% & begin Dec 20/21 sales with 15% hedge in $3.44-$3.48 range. Old-crop soybean sales should also be upped to 85% at current levels with a 15-20% Nov 2020 hedge beginning in $8.80-$8.85 range.

Comments

Log in or sign up to join the conversation.