Market Analysis

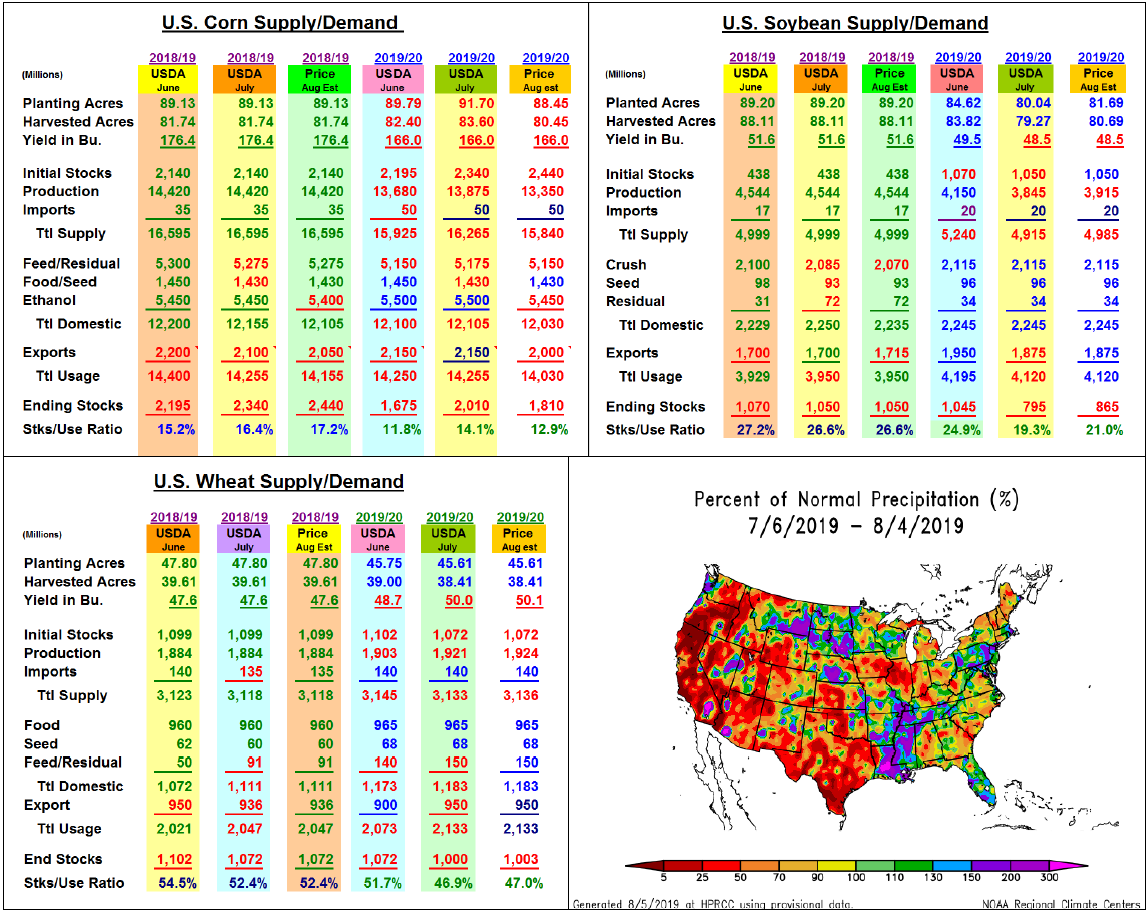

Going into the August 12 crop report, the trade chatter remains on 2019’s corn and soybean plantings because of the resurvey of Midwest acreage. After a cold, wet spring extended in June this year, the USDA decided to ask producers how they finalized plantings in 14 states. Given early June’s planting paces, the major changes will likely occur in the ECB and the NW Midwest. We anticipate 3.25 million lower US corn plantings to 88.45 million acre with 2.15 million occurring the Eastern Midwest. With the USDA paying its 2019 market facilitation payment based upon planted acres, many in the ECB decided to plant soybeans vs. taking PP according to roadside reports. This suggests 2019’s bean area may increase1.65 million acres to 81.69 million. Previous US August crop reports have been based upon observation plot plant counts and producer yield ideas. The USDA’s financial decision to delay their counts till September and 2019 lateness suggests the current revised US corn & bean yields will likely be continued until more definitive field information surfaces. For corn, this approach suggests a 525 million lower crop size of 13.35 billion bu. Given the recent sluggish in overseas demand and low margins in our domestic ethanol industry, old-crop stocks could rise 100 million bu. & these demand levels could be shaved for the new year. Overall, corn’s 19/20 stocks could drop to 1.81 billion bu. For beans, 2019’s output could increase by 70 million to 3.915 billion from higher seedings. Late season export shipment strength likely balances a slight slowdown in crush leaving old-crop stocks unchanged. Higher output likely means 70 million bu. higher 19/20 stocks. For wheat, Northern WW prospects may boost this variety, but PNW and northern ND dryness may slip spring wheat’s output. Overall, US output may rise slightly to 1.294 billion with stocks up 3 million to 1.003 billion bu.

(Click on image to enlarge)

What’s Ahead:

The USDA’s August acreage update will be helpful, but it might not be the final step in 2019’s harvested corn & bean acres. The current extensive dryness across Iowa and Illinois is a significant yield factor if it continues during August. We and the Pro Farmer Crop Tour will be visiting fields in IL and across the Mid-west in the coming weeks. Given the lateness of plantings, let's hope we find something to count. Hold sales. What’s Ahead: The USDA’s August acreage update will be helpful, but it might not be the final step in 2019’s harvested corn & bean acres. The current extensive dryness across Iowa and Illinois is a significant yield factor if it continues during August. We and the Pro Farmer Crop Tour will be visiting fields in IL and across the Mid-west in the coming weeks. Given the lateness of plantings, let's hope we find something to count. Hold sales.

Comments

Log in or sign up to join the conversation.