A stand-off over production cuts between Saudi Arabia and Russia, the world's two largest oil producers by volume after the US, has sent oil prices plunging and had a ripple effect across markets. Investors had expected the so-called OPEC+ group, of which Saudi Arabia and Russia are the key players, to agree to cuts of somewhere between 750,000 barrels per day (bpd) and 1.5m bpd in a bid to stabilize the oil price in the face of slumping demand due to the coronavirus.

Reports suggested that Saudi Arabia had threatened to walk away from any production cuts at all if Russia did not agree to the full 1.5m bpd cut that Saudi Arabia proposed.

Seemingly angered that US shale oil producers outside of OPEC would benefit from the likely price rise without having to reduce production (because the US is not a member of OPEC+) , and emboldened by low production costs and stronger domestic finances, Russia effectively called Saudi Arabia's bluff.

In response, Saudi Arabia performed a sharp pivot and instead of cutting production is flooding the market with increased production at major price discounts in a bid to maintain market share.

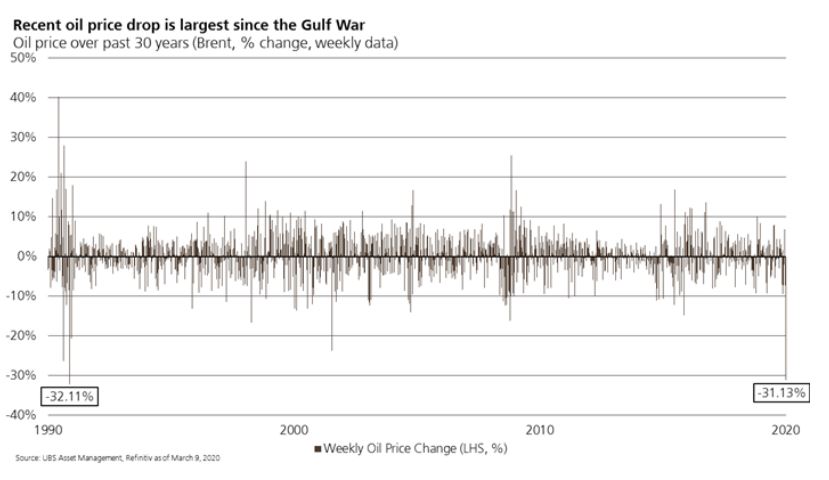

Having already assumed that the OPEC+ meeting would result in production cuts, major oil benchmarks dropped around 10% on Friday, and have now slumped around 30% as a simultaneous demand and supply shock have their inevitable consequence.

News of the arrest of two members of the Saudi royal family over the weekend as King Salman seeks to smooth the transition of power to his son, will hardly help short-term investor sentiment about political stability in the Kingdom and its connection to the oil price.

What to expect?

So is this a structural break in the relationship between the two ex-US oil power brokers – or a short-term misunderstanding that can be rectified?

There is clearly deep frustration on both sides at how last week's OPEC+ meeting developed. Russia may be able to withstand lower oil prices significantly better than it could historically, but a very low oil price is not good for either Russia or Saudi Arabia.

In our view, developments do not completely preclude production cuts in the coming quarters, particularly given the strong relationship between Vladimir Putin, King Salman and Crown Prince Mohammed bin Salman. And after recent price action, there is now scope for those cuts to surprise the market positively. But such a deal is far from a given. The worrying aspect is the 'tit for tat' production ramp up by Saudi Arabia and the apparent end of OPEC+ as a major driver of oil price stability.

Economic implications

These developments come at a time of already considerable investor fragility as the coronavirus' spread in the US and Europe accelerates. Given that fragility, the spillover from commodity markets is potentially significant.

Economically, the drop in oil prices reduces the spending power of a number of oil-producing countries – albeit that this is countered to a degree by the boost to the disposable income of global consumers and to the margins of major oil importers such as China and India. However, we believe that any boost is unlikely to be material in the short-term face of the coronavirus.

Both growth and inflation expectations are likely to be hit globally – with government bond yields sent to fresh all-time lows. The drop in prices is likely to hit the US, the world's largest exporter of oil, harder than elsewhere – leading to a drop in capital expenditure and employment from the economically important shale oil industry.

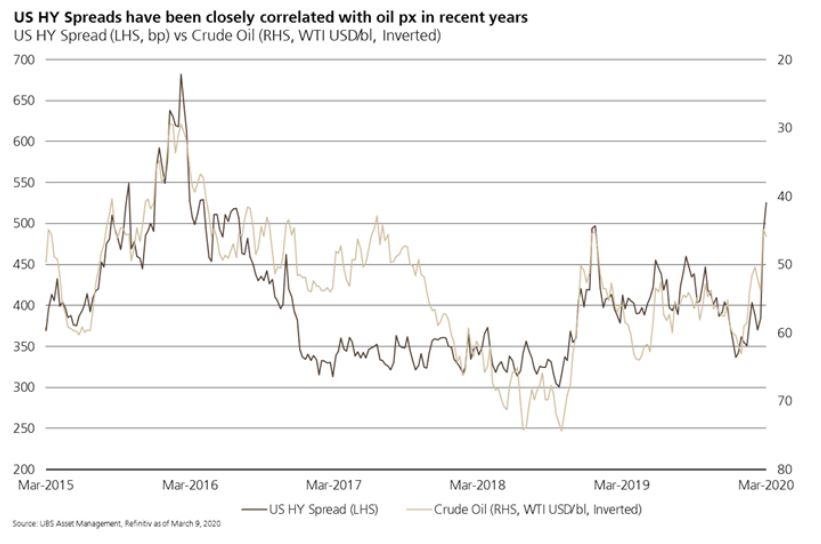

From a market perspective, the potential impact on credit is noteworthy. For highly-indebted oil producers in the US in particular, the fall in oil prices is not a question of lower shortterm earnings, but a question of solvency. In part, this is what Russia wants: to exploit the current global situation and permanently remove some of the supply coming out of the US. There are therefore knock-on effects of the oil price drop for oil equipment manufacturers and to bank lenders to the US oil industry.

US High Yield credit spreads have widened quickly and significantly to reflect this. We expect them to stay wide without any deal between the Saudi Arabia and Russia. Despite recent market movement, the energy sector still represents around 12% of US High Yield.

Importantly, we believe that these issues are unlikely to be contained within the energy sector – and raise valid concerns about the wider credit universe and about market liquidity. There is a well-documented potential mismatch between assets under management in passive high yield vehicles and dealer inventory in underlying bonds. With the coronavirus adding to liquidity concerns, these ingredients raise the prospect of exaggerated price moves if redemption flows in these high yield vehicles increase more significantly.

Outside of the specifics of the energy sector, the oil price developments represent an additional source of volatility that increases the short-term equity risk premium and is an additional weight on investor sentiment already hit by the coronavirus. Risk assets appear to have been slow to price in the risks to global growth. We therefore do not see the drawdown in global equity markets and sharp drop in US Treasury yields as a significant over-reaction to the negative newsflow of the coronavirus or energy markets over recent days.

Looking forward we expect further cuts in policy rates and an expansion of central bank balance sheets across major economies including the US, UK, Eurozone and Japan in the coming days in response to the coronavirus growth shock and risks of contagion from the falling oil price. But the effectiveness of monetary policy is diminished, at least in the short-term, by the impact of the coronavirus on economic growth.

In our view it is therefore a step change in fiscal spending from major economies that holds the key to reinvigorating growth expectations and improving investor confidence. And if policy makers are able to ward off contagion and recession, there is scope for a very sharp rebound in economic growth and in risk assets given the benefits of loose monetary policy and a low oil price.

How are we positioning portfolios?

Within Global Equity markets, the collapse in the oil price has further reinforced the 'flight to safety' we have seen in markets with cyclical stocks underperforming defensive stocks. Energy stocks are big components of Value indices and therefore Value has further underperformed growth. The riskoff environment has also put pressure on highly leveraged companies.

We are using such short term dislocation to increase holdings where shares have fallen below our estimates of long term value, while being mindful of the risk of further disruption. We are being especially sensitive to investing in companies where we believe the current uncertainty may impact their long term business models. Our experience has proven that such times present excellent potential opportunities to take advantage of over-reactions in markets.

For Fixed Income, we previously reduced credit risk and have positioned strategies to benefit from increased demand for high quality sovereign and corporate bonds. Specifically, we pared back our investment grade and high yield positions from last year and into January while maintaining a bias to long duration.

At this stage we do not anticipate making any material changes to positions. We are, however, mindful of the fact that we are in totally unchartered territory and extra caution is therefore warranted.

Comments

Log in or sign up to join the conversation.