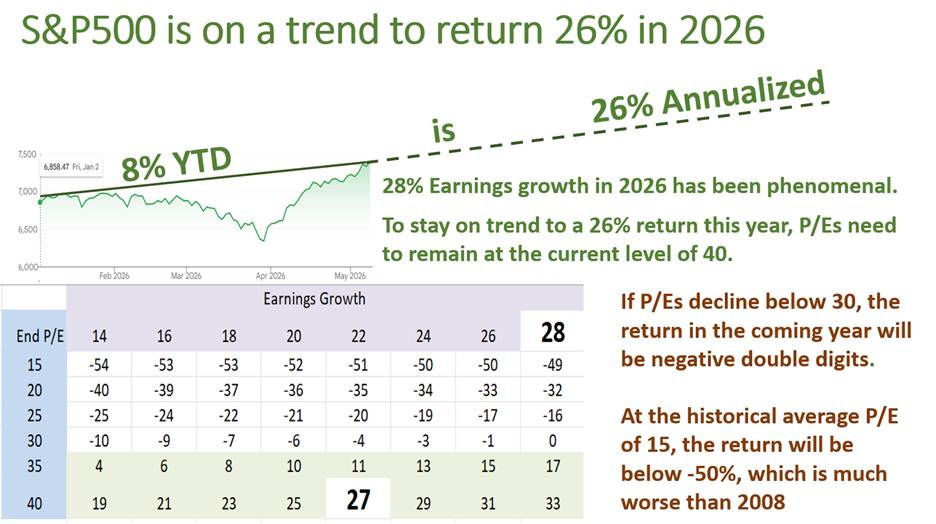

· The S&P 500’s current trajectory suggests a potential 27-33%return in 2026 IF earnings growth and P/E multiple remain elevated.

· Earnings are growing 28% currently, which should have reduced P/Es but it hasn’t. P/Es have expanded to an unprecedented level of 40, raising valuation concerns.

· If P/Es return to their historic norm of 15, stock prices will halve. If valuations bring P/E below 30, double digit losses will result.

The ranges of returns that might be earned in 2026 depend on earnings growth during the year and the Price/Earnings (P/E) ratio at the end of the year. The formula I use to construct the table is:

Return = Dividend Yield + (1 + Earnings Growth) X (1 + P/E expansion/contraction) – 1

Now a third of the 2026 return puzzle is in the books. The S&P 500 has returned 8% so far this year, so the trendline points to a 27% for the whole year 2026 – a very good return. We can use the formula above to solve for the combination of ending P/E and earnings growth that will deliver a 27% for this year. It’s a P/E that remains near the current level of 40 and earnings growth above 22%.

Here’s the trendline and the return table:

But earnings are currently growing faster than 22%. So far this year they are growing 28%. which – if it continues, AND P/Es stay at their current level of 40 – will lead to a 33% return in 2026.

So, an optimistic outlook sees today’s stock market returning 25-35% this year, which is phenomenal, especially since it follows 3 other very good years.

The other side of the performance puzzle

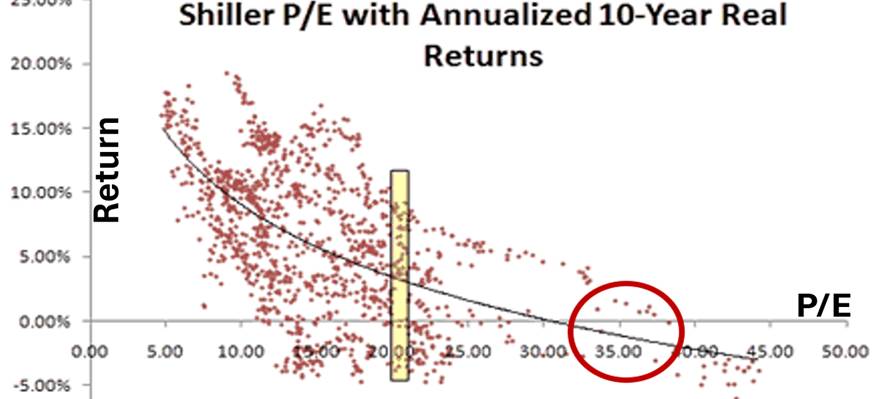

But what if P/Es regress back toward their historic average of 15? If the US stock market reaches a P/E level of 15 over the next year, it will lose more than 50%. Any decline below 30 will result in double digit losses, regardless of earning growth.

The following relationship between current P/E and subsequent return reinforces the current risk.

Conclusion

The current strong earnings growth is cause for celebration, and you’d think that it would bring down the market P/E because the “E” in that ratio is growing, but it hasn’t. P/Es continue to expand, well into the realm of “never before.” The US stock market is extremely expensive. In the past, stock markets have not remained expensive for long. Is it because of artificial intelligence? Perhaps, but a similar argument was made during the dot.com bubble.

At the current level of expensiveness, investor demand for lower stock prices will tend to drive the stock market down, reducing P/E. Increasing the “E” hasn’t done it, but decreasing the “P” will. If P/Es reach their historic norm, stocks will lose half their current value. Watch out!!

Comments

Log in or sign up to join the conversation.