It seems that the financial punditry, as well as many of their interviewees, are perplexed that the yield curve is flattening. At Bond Squad, we are not the slightest bit surprised. In the Bond Squad “2015 Outlook,” published 12/23/14, I opined:

“As the Fed raises short-term rates, the long end of the curve could begin pricing-in the effects of less accommodative Fed policy. This could result in a fairly flat yield curve at relatively low interest rates.”

This is precisely what has occurred since Fed liftoff has become more likely. Yesterday, media stories abounded that the yield curve was flattening because the Fed is expected to tighten gradually and modestly. In my opinion, this is not quite right. The curve is flattening because the Fed is poised to liftoff (which is considered anti-inflationary) at a time inflation is expected to remain fairly low. Thus, the yield curve is flattening via rising short-term rates and falling long-term rates.

That the yield curve is flattening in this way is not surprising, in itself, but I do not blame non-fixed income laypeople for being confounded. Usually, the curve flattens via short-term rates rising and long-term rates falling in the latter stages of a tightening cycle, not when the Fed lifts off. I believe the bond market is telling participants that, when it comes to the credit cycle, it might be later than you think. U.S. high yield defaults are rising and emerging market corporate defaults are at their highest level since 2009. I think we are in the early stages of the junk debt correction. When one considers that the Fed began tapering two years ago (which is a removal of stimulus, no matter how much some market participants attempt to deny it) and the expanding meltdown in the high yield credit markets, signs are there which augur for late cycle.

I believe that investors, pundits, advisors and even strategists have become too hung up on absolute numbers when they should be tracking trends. There is no law of economics which states that the neutral Fed Funds Rate must be 4.00% or that Consumer Confidence must move above, say, 110 to mark the peak of an economic cycle. Even technical strategists and analysts look for chart patterns rather than absolute numbers. Why is there a newfound affinity to relying on precise repeats/reversions of data? In my opinion because it relieves the need to be vigilant and (to some extent) responsible for portfolio management decisions.

Go tell it in the Markets

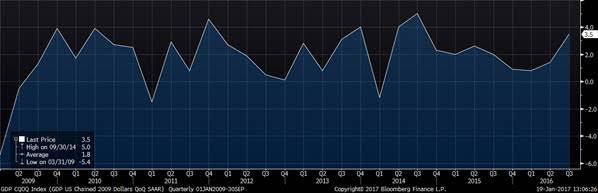

The bond market is definitely telling me something. It is telling me to expect core inflation below 2.0% and annual GDP just above 2.0% in 2016. Some equity wonks point to the apparent disagreement between the fixed income and equity markets. I do not see much disagreement. The equity market recovery has become increasingly narrowly-focused. This can be a sign that the business or market cycle is becoming long in the tooth. My 2016 Outlook, due out in two weeks, should paint a clearer picture of where I think the economy and bond market conditions are heading.

Also, don’t expect much help from commodities on the inflation front. The need for foreign economies to generate revenues as best they can should keep supplies high. That, combined with what should be a strong U.S. dollar should put somewhat of a lid on inflation pressures.

The Man with All the Toys

Puerto Rico made its debt payments, yesterday. Governor Alejandro Garcia Padilla signed an executive order to use money earmarked for servicing the debt of several public corporations to service interest due and to repay principal on $354 million in Government Development Bank bonds partially guaranteed by the commonwealth. Next up for Puerto Rico is a $357 million general-obligation interest payment on January 1st, 2016. In a November 6th filing, Puerto Rico said it might not be able to service all of its G.O. debt, even if it uses clawback provisions on other classes of Commonwealth debt. Bond Squad is not optimistic for the prospects of any holders of uninsured Puerto Rico bonds receiving par at maturity. This is not to say that receiving par is an impossibility, only that I would not count on it.

Santa’s got a Hot Rod

U.S. Auto sales for November (SAAR) printed at 18.12M. This was a repeat of the October Seasonally-Adjusted Annual Rate total. An improving job market, low financing rates, low/no money down loans, loans with longer tenors and an increased interest in vehicle leasing has driven auto sales to near record levels. SUVs, particularly crossovers, were the most popular class of vehicle. The average term of an auto loan was 67 months (which I believe is an all-time high) and about 25% of all new car sales were actually leases. The consensus opinion from industry watchers is that, although consumers are confident enough to purchase a new vehicle, keeping payments as low as possible is of great importance. Rather than purchase less vehicle, they purchase a more expensive vehicle and keep monthly payments low via longer-term loans and leasing.

This sounds a lot like the 2005-2007 housing market, doesn’t it? Although I don’t see a “bubble” in autos, it does appear that sales are above core economic and demographic trends. With the yield curve flattening, credit could become more constrained. Maybe this is partially responsible for the mediocre performance of auto manufacturer stocks? Autos looked frothy to me last year, but ever easier credit terms and more aggressive discounting has kept the party going. At some point, the party has to at least die down a bit. As such (where suitable), I favor the bonds of auto parts retailers and some replacement part suppliers over automaker bonds. At some point in the next few years, there could be many cars which are not fully-paid for needing replacement parts. Owners might be less inclined to trade them in, if credit conditions are not quite as easy as today. Also, aging demographics augurs for owning cars longer, at some point down the road.

Comments

Log in or sign up to join the conversation.