Market Analysis

The ongoing weakness in energy prices and the building concerns about demand destruction from the current COVID-19 impact on the US economy hung over the US agriculture prices during the latter half of April. Despite OPEC voting to reduce its output at a mid-month meeting, the lack of an immediate output cut (May 1 date) and a US concern about storage availability lead to an ugly May futures expiration. This resulted in the 1st ever negative price close for US oil. A pick-up in Chinese US purchases near historic low prices provided some late month bean support.

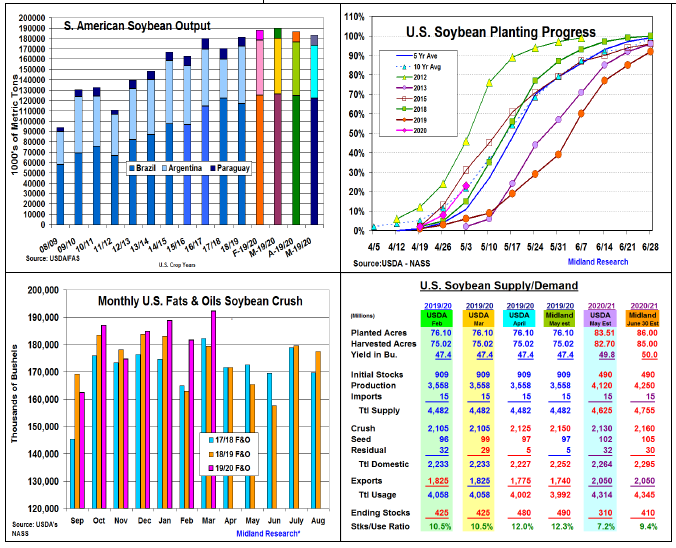

With the USDA releasing their initial 2020/21 World and US supply/demand forecasts along with making some oldcrop revisions on May 12, S America’s soybean prospects will be back in focus. Ongoing dryness in S. Brazil & parts of Argentina suggests 2.3 and 1 mmt declines in their crops to 122.2 & 51 mmt levels this month. Overall, South America’s output is still likely to remain 2 mmt higher than last year.

2020’s US soybean plantings are off to a strong start at 23% this week. This pace is above the 5 year rate, but near the 10 year average. The W Midwest is the furthest along with IA (46%), MN (35%) & NE (35%) leading the way.

The latest US soybean crush for March revealed the 3rd monthly record since October of 192.2 million bu. of beans being processed. With the US ethanol industry retrenching dramatically, US livestock feeders will have to rely on soybeans for their protein going forward because of reduced DDGs. This suggests a 25 million jump in crush to 2.15 billion bu. However, exports remain sluggish suggesting a 35 million cutback in these sales resulting in a 10 million bu rise in US stocks to 490 million.

The USDA normally uses its Ag Outlook demand & yield levels along with its spring planting level for their initial new -crop balance sheet each May. This formula will project a yearly drop in US 2020/21 stocks leaving room for more 2020 seedings as some country reports are saying.

What’s Ahead: China has appeared as a buyer on setback near soybean’s long-term $8.00 per bu price support. Hopefully, the recent tensions over the origins of this year’s coronavirus outbreak don’t derail the US/ China Phrase 1 trade deal. Given the building domestic demand for soybeans, use spot July prices in $8.75- $8.95 range to advance sales to 85% & begin Nov 2020 marketings with 15-20% at $8.85.per bu.

Comments

Log in or sign up to join the conversation.