Photo by A. C. on Unsplash

When geopolitical tensions flare up, the natural assumption is that gold should immediately surge. War breaks out, markets panic… and the metal rallies as investors rush to safety.

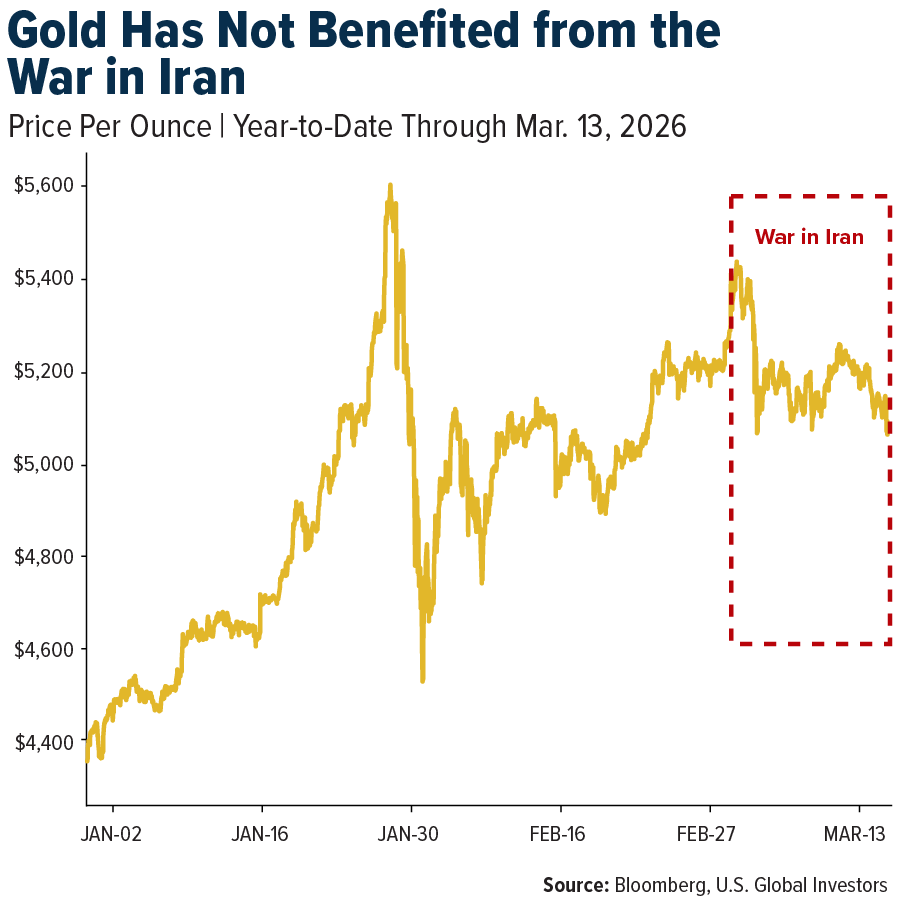

That’s historically been the case, yet over the past two weeks, the opposite has happened.

Despite hostilities raging in the Middle East, gold has struggled to gain traction and is even down modestly from recent highs. That raises the question: why isn’t the precious metal behaving like a classic safe haven right now?

The answer has to do with oil, interest rates and the U.S. dollar.

Oil Is the Real Shock Driving Markets

Last Thursday, Brent crude closed above $100 per barrel for the first time since 2022 after attacks on shipping in the Persian Gulf severely disrupted global oil flows. According to the International Energy Agency (IEA), the war has created the largest supply disruption in the history of the oil market, with exports through the Strait of Hormuz plunging to a fraction of normal levels.

This matters enormously because roughly a quarter of global seaborne oil passes through Hormuz. And when flows slow as dramatically as they are now, the entire energy system tightens almost immediately.

But as many of you know, oil shocks rarely stay confined to the energy sector. They quickly spread across inflation expectations, interest rates and currency markets. That’s exactly what we’re seeing now.

Is Diesel a Threat to Inflation?

Much of the economic impact from the conflict is tied not necessarily to gasoline but to diesel.

After all, diesel powers freight transport, agriculture, construction, mining and a whole lot more. Analysts estimate that disruptions around the Strait of Hormuz could remove roughly 3 to 4 million barrels per day of diesel supply, representing as much as 12% of global consumption.

Because diesel is so embedded throughout the economy, rising prices can push up the cost of transporting goods and producing food. The result is broad inflation pressure that spreads far beyond the energy sector, just as we saw when Russia invaded Ukraine four years ago.

Higher Oil Means Higher Interest Rates

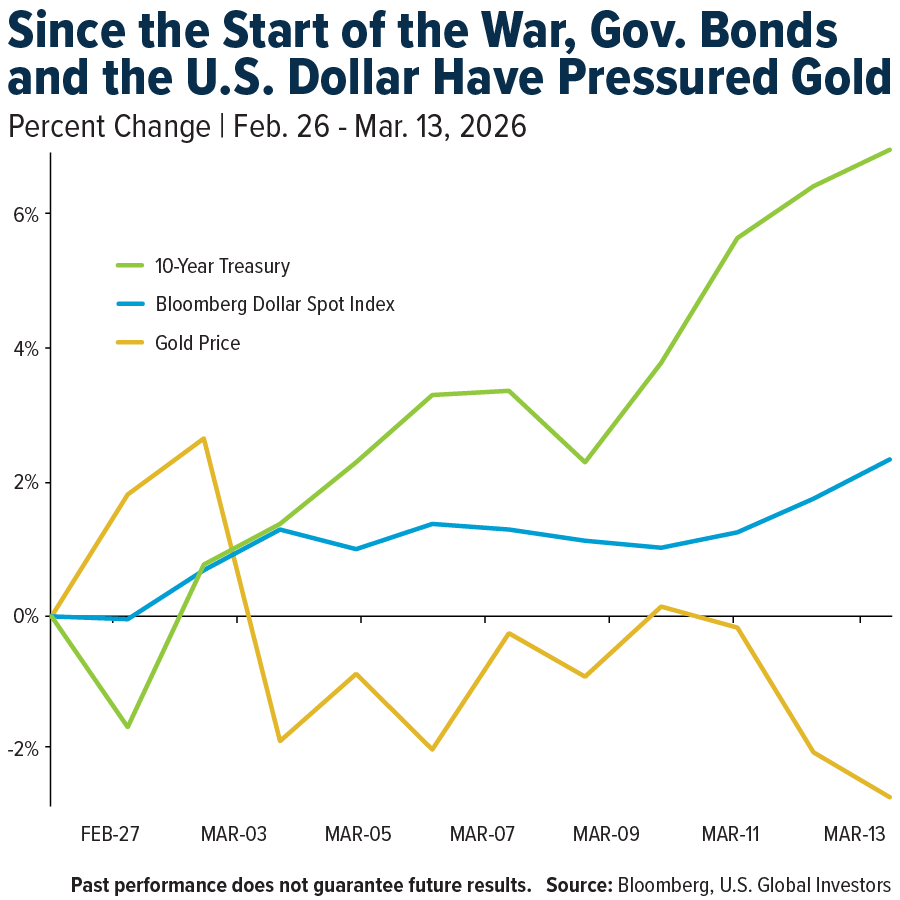

The bond market has responded accordingly. Treasury yields have moved higher as traders bet that the Federal Reserve may need to keep interest rates elevated for longer than previously expected.

Higher yields, as I’ve explained many times before, create a headwind for gold in the short term.

As you know, gold doesn’t pay interest or dividends, so when bond yields rise, investors can become temporarily less enthusiastic about holding the metal. Rising rates also tend to strengthen the U.S. dollar, which further weighs on gold prices.

This is precisely what’s happened since the war began. The U.S. dollar has rallied while gold has drifted lower, creating a divergence between two assets that are both traditionally viewed as safe havens.

The Stagflation Risk

I see the broader macro environment also shifting in ways that makes gold look even more attractive as a haven.

If energy prices remain elevated, the global economy could face a period of slower growth combined with persistent inflation… which is the classic definition of stagflation.

That’s according to a report by Oxford Economics, whose models show that if oil prices were to trade above $140 per barrel for two months, global growth could stall while inflation could spike toward 6%.

I should point out that this is a worst-case scenario, and the odds of it happening are low, according to Oxford analysts. But this type of crisis has historically created the sort of volatile conditions that have forced investors to rethink traditional portfolio strategies. I believe real assets, gold especially, look especially attractive in these environments.

The Fiscal Backdrop Looks Even More Fragile

Another important factor is the fiscal position of the U.S.

The country entered the war in Iran with national debt approaching $39 trillion, rising by more than $7 billion per day over the past year, according to Congress’s Joint Economic Committee. Meanwhile, deficits remain large and interest payments are consuming a growing share of federal revenues.

This obviously limits policymakers’ flexibility.

The war itself is incredibly expensive. Pentagon officials estimate that the first week alone cost taxpayers roughly $11 billion. If the conflict escalates or drags on, fiscal pressures would increase further.

Historically, periods of rising debt and geopolitical uncertainty have ultimately been supportive for gold.

Why I Think Gold’s Weakness May Be Temporary

I think it’s important for investors to distinguish between short-term market action and long-term fundamentals.

In the short term, rising oil prices have pushed bond yields and the dollar higher, which has created pressure on gold. But the underlying drivers that typically support gold remain very much in place.

If the conflict continues, and inflation remains elevated and fiscal pressures grow, I believe the longer-term case for gold may become even stronger.

And with the metal still trading below $5,100 per ounce, now may be an opportune time to accumulate. I’ve always recommended a 10% weighting in gold, with 5% in physical bullion and the other 5% in high-quality gold mining stocks. Remember to rebalance on a regular basis.

Comments

Log in or sign up to join the conversation.