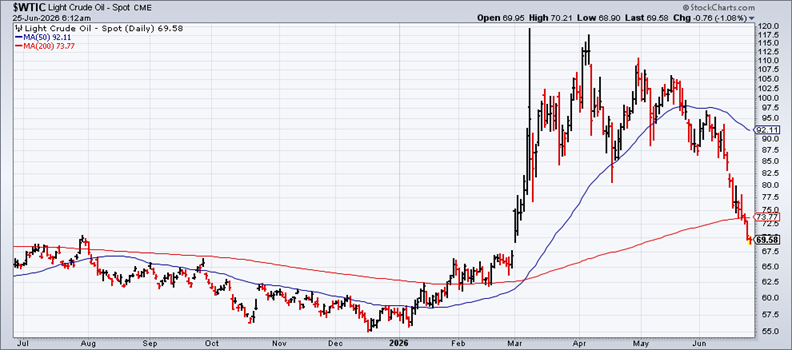

The price of the U.S. benchmark for crude oil fell below $70 a barrel on Wednesday, marking the lowest level since the war with Iran began on Feb. 28. The sharp slide will ease pressure on headline inflation measures in the coming months. The question is whether the bond market will soon follow suit, and price in lower inflation risk? Hanging in the balance is the outlook for Federal Reserve rate hikes.

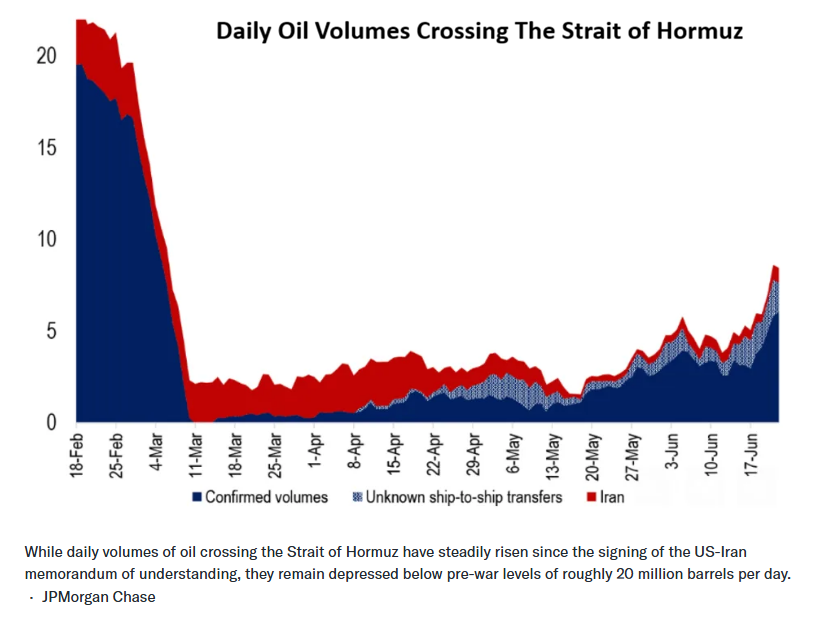

Weighing on oil prices is a preliminary deal to end the war with Iran, and shipping through the Strait of Hormuz is gradually recovering, although energy volumes remain far below pre-war levels. “What shippers are looking for is consistency over days and weeks,” says Matthew Wright, a freight analyst at Kpler, which analyzes global shipping.

The oil market is pricing in continued progress and a return to normal energy exports in the weeks and months ahead. “Traders are pricing in a return to normality,” says Francis Osborne, head of oil analysis at Argus Media, which tracks oil prices. “They are not taking into account the risks further down the road, which still remain very real.”

Despite the uncertainty that still hangs over the Middle East, Treasury yields have begun to pull back, although unevenly. The 30‑year yield, the most inflation‑sensitive maturity, fell sharply yesterday, dropping to 4.84%, the lowest level in several months. The benchmark 10‑year yield also declined, reversing the spike of the past month or so.

A notable exception is the policy‑sensitive 2‑year yield, which eased yesterday but at 4.16% remains close to its recent peak set just a few days earlier. The implication: the market isn’t fully persuaded that inflation risk has faded or that Fed rate hikes are unlikely.

Apollo Chief Economist Torsten Slok writes that lower oil prices could turn out to be inflationary, explaining:

The narrative in markets is changing from “lower oil prices mean lower inflation” to “lower oil prices mean more demand in an already overheating economy, which means higher inflation.” Driven by the strong April CPI, hot May non‑farm payrolls, and a hawkish Fed, the market narrative now suggests that the reopening of the Strait of Hormuz will further overheat the economy, forcing the Fed to raise interest rates soon.

Determining whether Slok’s outlook is accurate will take time, as uncertainty from geopolitical and macroeconomic risks cloud the outlook. In the immediate future, however, a degree of relief is expected for inflation.

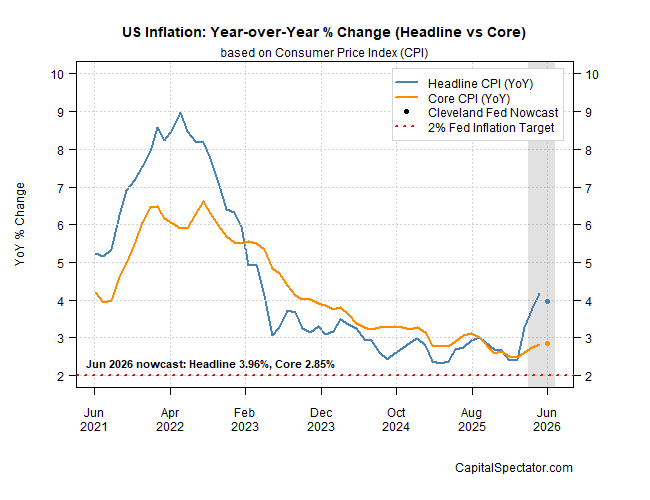

The Cleveland Fed’s nowcast for year‑over‑year CPI calls for a modest downshift after several months of hotter prints. Core CPI’s trend, which has remained relatively stable throughout the war—edging only slightly higher—is on track to rise 2.9% in this month’s update versus the year‑ago level.

Fed funds futures, however, are pricing in higher odds of rate hikes in the near term: a 34% probability of a ¼‑point hike at the next FOMC meeting on July 29, rising to 67% in favor of tightening in September.

Morningstar predicts that any lingering inflation in the near term will eventually fade. “We expect inflation to fall in the coming years. Receding energy prices will be reflected in a negative impulse to inflation in 2027. The tariff impact should also cease going forward. Moreover, wage growth has slowed considerably, which should help push services inflation back to normal. Housing inflation also continues to trend down.”

But for the moment, 2027 still feels far away. For now, markets are taking the win on cooling prices. But with the Fed’s path still unsettled, the calm may yet prove fleeting.

Comments

Log in or sign up to join the conversation.