Summary

As AI shifts from Training to Inference, the market moves from brute force to efficiency. Custom ASICs will inevitably erode NVIDIA’s dominance in this new mass market.

Hyperscalers’ CapEx growth is set to decelerate in 2026 due to the law of large numbers. This slowdown contradicts the market’s pricing of infinite exponential growth.

With shortages ending, the sector is becoming a Buyer’s Market. Rising competition from AMD and custom silicon will pressure NVIDIA’s 70% margins and crush the high P/E.

In September 2025, I downgraded the recommendation on NVIDIA shares to “Hold,” and wrote at that time that the current stock valuation leaves increasingly less room for maneuver, considering long-term risks and changes in the market structure. At the same time, throughout my cycle of analytical materials dedicated to Marvell (MRVL) and Broadcom (AVGO), I argued the thesis that the subsequent phase, or, if you desire, iteration of artificial intelligence growth will belong by no means to universal graphics processing units (GPUs). No, it is specialized custom chips (ASICs) that will rule the show.

And now I consider that the impenetrable wall, which Jensen Huang had been painstakingly building around his CUDA ecosystem for years, has developed a serious crack. Tech giants like OpenAI, Amazon, Google, and Microsoft no longer burn with the desire to underwrite NVIDIA’s profit. They are actively introducing their own solutions or transitioning to architectures that are more effective from the point of view of price.

For investors sitting in positions, this means exactly one thing. Namely, that the Risk/Reward equation for NVIDIA shares has broken. It has shifted not in favor of the buyer. I see that the growth potential is limited by the effect of a colossal base, whereas the risks of a correction are increasing. The market continues to irrationally value the company as if it were situated in the very earliest stage of a cycle of infinite exponential growth. Whereas macroeconomic and manufacturing indicators point to the fact that we are entering a phase of inevitable plateau and commoditization — the transformation of a unique good into banal raw material.

From Windows to Android — analogy with PC

The main argument of the “bulls” usually sounds thus: “NVIDIA is the Microsoft of the AI era. And CUDA is the analogue of Windows. It is a standard which is impossible to replace, it is the base.” After all, the greater part of software for data centers is created for CUDA. And this is a strong argument, I do not dispute, but it describes a past war that has already ended. Let us conduct a deeper analysis. Yes, Windows remained the dominant system in the PC market. And not merely did it remain, it cemented itself there. Windows as an operating system totally dominates in PC.

But wherein did the main explosive growth occur in the last 15 years? More precisely, where was the money? It occurred in the mobile segment. Precisely there, where iOS and Android won. The PC market became niche and stable, while the market of mobile devices became mass, aggressive, and ubiquitous.

And it is my thought that in the future, exactly the same thing can happen with CUDA.

Training (Model Training) — is a complete analogue of the legacy PC market. Here indeed universality, maximum flexibility, and brute computational power are needed. Here NVIDIA and its H100/Blackwell chips, undoubtedly, will remain kings. But the nuance is that the market of training is finite.

Inference (Model Output/Usage) — is the analogue of the mobile market, and it is huge. When the model is already trained, it needs to be launched billions of times for end users. And right here universality is not needed. Here energy efficiency and low cost of transaction are critically needed.

To launch a simple chatbot on H100 — this turns out to be both insanely expensive, and too hot, and, what is most important, absolutely inefficient from the point of view of costs. The market inevitably shifts in the direction of specialized solutions (ASIC) and cheaper, simple GPUs. NVIDIA, however, attempts by way of inertia to vend a premium product to a market that requires utilitarian, cheap solutions. And this structural, tectonic shift is currently stubbornly ignored by the market.

Macro-risk: The Wall of CapEx and the law of large numbers

The second pillar, upon which all this inflated capitalization of NVIDIA holds, is an almost religious faith in the infinite growth of capital expenditures (CapEx) from the side of Big Tech (Microsoft, Google, Amazon, Meta).

However, we abut into the harsh reality of mathematics, or more precisely — into the inexorable law of large numbers. Let us take a glance at the dry dynamics. In 2024, the aggregate growth of CapEx of hyperscalers constituted a phenomenal +63%. In 2025, at the very peak of this “arms race,” it accelerated to +73%. But what awaits us in 2026? Analysis of consensus forecasts and cautious comments of financial directors of companies points to a sharp slowing of growth rates to 36% or even lower.

But a slowing of growth rates — is still growth in absolute dollars. Why worry? The answer lies in the effect of a high base and the requirements of the company’s current valuation. Let us calculate absolute numbers. In 2025, the aggregate CapEx of hyperscalers amounted to approximately $400 billion. Growth by 36% in 2026 implies an addition of roughly $140 billion in new capital expenditures.

For a company valued at $1 trillion, the influx of such money into the market is rocket fuel. But today the capitalization of NVIDIA constitutes $4.5 trillion, and the market values it with a P/E multiplier of about 45. In the world of “hardware,” a normal P/E for a stable, mature leader company constitutes about 25–30. The current P/E of 45 means that the market is laying in further aggressive expansion of the business — investors expect that profit and revenue will grow by another one and a half times before growth stabilizes.

Let us translate this into dollars. NVIDIA’s revenue for the last quarter amounted to $57 billion, which yields an annualized base of around $228 billion. To justify the expectations of growth laid into the P/E of 45, and to increase by one and a half times, NVIDIA needs to generate over $110 billion of additional sales per year. And now let us compare: the entire market of hyperscalers in 2026 will add to its expenses only about $140 billion (that very +36%). Even if one were to assume a fantastic scenario, wherein almost every new dollar from the CapEx growth of the entire market goes exclusively to NVIDIA chips, this will barely suffice to simply justify the current valuation. But besides chips, companies also spend on the actual construction of buildings and other equipment. The arithmetic breaks down: the absolute growth of the market no longer keeps pace with the exponential expectations laid into the share price of the huge company.

Financing in debt: In 2024, companies spent their cash reserves on Capex. In 2025, they commenced to actively borrow. Debt issuance by hyperscalers has already exceeded the mark of $100 billion. And to spend credit money at current high rates — that is, you know, a completely different financial discipline. Financial departments will begin to ruthlessly cut expenses.

The end of the chip shortage

The most dangerous moment for any cyclical company arrives when the shortage disappears. The entire year of 2023 and 2024, NVIDIA had a free ride, enjoying a unique situation: demand exceeded supply by times. Clients literally stood in queues, overpaid wild sums on the secondary market, and placed double orders, merely to snatch at least something.

But in January 2026, the situation changed:

Collapse of Lead Times: According to data from UBS and reports from supply chains (Tom’s Hardware), waiting times for H100/H200 chips collapsed from peak 52 weeks to quite comfortable 8–12 weeks. Now it is a regular commodity “from the shelf,” take it or leave it. And when the commodity is available, panic vanishes. And, naturally, the markup disappears.

A fair question: if delivery times are falling, where is the evidence in the form of immediate price reduction, growth of warehouse inventories (inventory), or fall of the order portfolio (backlog) in current reports? The answer lies in the mechanics of business cycles: prices and balance sheet inventories are lagging indicators. But I think that the dynamics of delivery times — is the purest leading indicator, measuring the very strength of the “seller’s market.”

While clients stood in line for a year, the pricing power of NVIDIA was absolute — there could be no talk of any discounts. Now, with an expectation of 8–12 weeks, NVIDIA is still located in the seller’s market, and right now prices have not yet fallen. But the fundamental strength of this market is no longer what it was a year ago. The panic has departed, and clients no longer need to make redundant orders. For a long-term investor, this is a clear signal: the peak of absolute pricing dictatorship is passed. In the following quarters, this shift in negotiating position will inevitably begin to convert into pressure on margin, and only then will it be reflected in the official backlog.

Production Tsunami: And furthermore, the problem was not in the chips themselves, but in the complex CoWoS packaging. TSMC, with the support of Samsung, aggressively, at rapid tempos expanded capacities. According to data from TrendForce, capacities of CoWoS in 2025 doubled, reaching 75,000 wafers per month. The “bottle neck” is already being eliminated.

We are gradually transitioning from a market where the seller dominated to a more balanced market. In such conditions, to hold super-high prices will be very difficult.

Theory of “Critical Mass” of AMD

Critics and skeptics often say: “AMD lags by years. No one in their right mind will rewrite code under their chips.” But I consider that this is a deep misconception, based on a situation from the past. I propose to take a glance at this through the prism of the “Theory of Critical Mass.” Earlier, the AI market was small, tiny. A theoretical share of 10% from a small market banally could not give AMD money for the development of software. Now the market constitutes hundreds of billions of dollars. And now even a modest 5% of the market, which AMD can gnaw off from NVIDIA, — is a big piece, which will already allow developing software for AMD.

What does this change in essence?

Financing of ecosystem: These monies are now more than sufficient to hire thousands of the best programmers of the world for the finishing of the ROCm platform (analogue of CUDA).

Motivation of clients: When Microsoft or Meta purchase clusters for $500 million, they inevitably supplement the ecosystem of AMD. It is a question of economy of tens of millions of dollars. Code is now written not by enthusiasts-loners in garages, but by entire departments of the largest corporations of the world.

Openness against Closedness: NVIDIA builds a closed, fenced-by-fence ecosystem (like Apple). AMD and the consortium UALink build an open system (like Android/PC). The history of IT time after time shows that open systems always win in the mass segment at the expense of wide spreading.

Also it is important to remember one nuance: AMD, like NVIDIA, is a fabless company. They do not have a rigid limitation by factories. They use the same lines of TSMC. If demand swings to the side of AMD, then they will simply buy out the freed quotas for production, and that is all. NVIDIA has no unique production advantage whatsoever.

Attack from the flanks: Custom chips (ASIC)

While NVIDIA and AMD fight over the market of universal GPUs, a real revolution is happening with ASIC chips. The largest clients of NVIDIA are becoming its direct competitors. Amazon (Trainium/Inferentia), Google (TPU), Microsoft (Maia) — all of them are working tirelessly, developing their own chips. Why do they do this?

Price: An own chip costs 2–3 times cheaper.

Energy efficiency: ASIC is sharpened strictly under one task. It does not spend energy on extra transistors, necessary for the universality of GPU. In conditions of deficit of electric power, every watt is on the account.

Independence: Not a single self-respecting tech giant wants to depend on a vendor who controls 90% of the market and dictates its conditions.

These are classic “substitute goods” in economic theory. They will not kill NVIDIA at once, no. But they methodically take away the most tasty, the most mass piece of the pie — the inference of standard models.

Trap of super-incomes

All said above leads us to the fundamental financial problem of NVIDIA — its profitability. Now the gross margin of the company is located at a cosmic level of 70%. These are figures characteristic for pure software (SaaS), and not for “hardware.” The market evaluates shares, proceeding from a false premise that this margin will be preserved forever. But this is impossible, the history of hardware provision shows that to hold such indicators in a mature market is extremely difficult.

Price pressure: AMD offers chips cheaper. To protect the share of the market, NVIDIA will have to either lower prices or give discounts. Or AMD will take away more and more share of the market.

Mix Shift: A shift of sales will happen to the side of less marginal products according to the measure of saturation of the market.

Let us conduct a basic analysis of sensitivity (Sensitivity Analysis). Let us imagine a quite realistic scenario: the strengthening of competition forces NVIDIA to lower prices, and its gross margin (Gross Margin) returns from 73% to a normalized 60%. From an estimated volume of revenue in the upcoming year in the volume of 220 billion dollars, gross profit will fall by approximately $28 billion. With the preservation of constant or growing operational expenses (OpEx), this is a direct reduction of operational profit (Operating Income). In the result we will receive a mathematical lowering of net profit per share (EPS) by approximately 20–25% even with stable revenue.

Moreover, if commoditization arrives, this will directly touch the incremental profitability of invested capital (ROIC) of the NVIDIA company. Undoubtedly, even with a lowering of margin, the business will continue to earn profit exceeding the weighted average cost of capital (WACC) — the company will remain economically healthy. However, profitability on every new invested dollar will begin to fall. From the point of view of an owner, a lowering of ROIC makes the current high premium in the evaluation of the company difficultly justified.

Finances: Trap of ideal figures

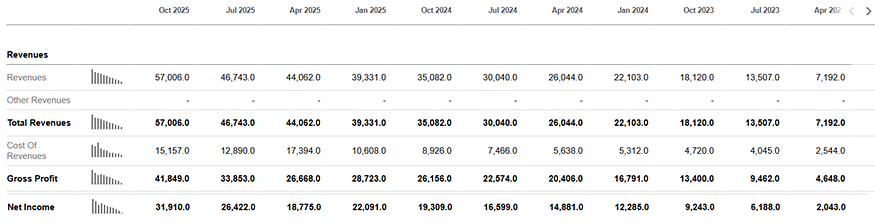

Let us take a glance at finances. Below I brought quarterly results, and, if one looks at them, then they look not simply good — they look absolutely impeccable. Only for one reporting quarter, which ended in October 2025, NVIDIA generated a colossal $57.0 billion of revenue and showed some kind of completely stunning, fantastic net profit of $31.9 billion. Simply look at this progression from April 2023. This is not a graph of revenue, this is a rocket taking off. Gross Margin (Gross Margin) for the quarter holds in the region of 73%. For a company producing a physical product, this is an unheard, anomalous indicator.

Press enter or click to view image in full size

But here is in what the fundamental problem consists. The market pays for this momentary, static snapshot a multiplier P/E of about 45. The market extrapolates this record margin into infinity, ignoring the potential cyclicality of the semiconductor branch. I, however, evaluating the business, am inclined to suppose that we are observing the peak of profitability.

Exactly at this point into the slender mathematics intervenes the factor of competition — the factor of AMD and custom ASICs. If AMD bites off even a modest 5% of the market in inference, or if Amazon transfers at least 10% of its capacities to own chips, NVIDIA will find itself in a not simple situation. It will turn out before a tough dilemma, where there is no good exit, where both decisions are worse: In variant A, they will need to aggressively protect their share of the market. And for this, Nvidia will need to lower its prices, entering into a price race. But this action will guaranteed collapse that very beautiful gross margin of 73%. In variant B, Nvidia can try to keep prices high to save margins at any price, but then it will have to sacrifice volumes of sales.

In both these scenarios, profit per share (EPS) will demonstrate negative dynamics much faster than the revenue itself because of the effect of the operating lever, which begins to work in the reverse side, against the company. The current market evaluation of the company with a capitalization of 4.5 trillion lays in an unshakable monopoly power of price formation. A power which, as I described above, is already weakening.

Conclusion: Why investors should exercise caution

In summary, I think that the situation around NVIDIA reminds of a classic completion of a cycle of hype. Technologically the company remains an unconditional leader. Its products are magnificent. But investments — this is not buying good products, this is buying future money flows at an adequate price.

The current price lays in an ideal scenario (priced for perfection). But I see here an absence of a “margin of safety” (Margin of Safety). I do not speak about a catastrophe or about the fact that the bubble will burst tomorrow. Such a company, like NVIDIA, possesses huge inertia, and the faith of the crowd does not disappear in one day. However, the potential of growth (upside) is now rigidly limited by the colossal size of the company itself and the effect of the base. At the same time, risks of lowering have strongly grown. The current valuation of the market completely ignores risks: slowing of CapEx, successes of AMD and appearance of an alternative program environment, transition of hyperscalers to own chips and physical saturation of the market.

But to hot heads I would say that to short the share is not needed? The market can remain irrational longer than you remain able to pay. To short a company, which has a huge program of reverse buyout of shares (Buyback) and is located in the center of attention of the crowd, — is mortally dangerous. Any announcement of a new chip can cause a short-term “short-squeeze.”

However, for a long-term investor, keeping shares of NVIDIA now — is an opportunity cost. The party comes to an end. In my view, shifting focus to a dry evaluation of the balance of risk and profitability clearly shows: the most reasonable decision now — is to exercise caution, take chips from the table while it is not too late, and shift capital into sectors, which only begin their cycle of growth, and not finish it at a historical limit of profitability.

This article was originally published on Medium (Investor’s Handbook)» — https://medium.com/the-investors-handbook/nvidia-times-and-conditions-for-the-company-are-deteriorating-f6bca0e2449f

Comments

Log in or sign up to join the conversation.