Buying dips has been a popular strategy since the Financial Crisis. Thus, when credit spreads blew out during the August-September 2015 market rout, many pundits and portfolio strategists suggested buying high yield debt on the dip as well. Bond Squad was opposed to this idea as weakness in the corporate credit markets was much more fundamental than it was technical or even emotional. Instead, I suggested selling risk on spikes. This was not a popular concept among Bond Squad readers as it contradicted what investors and advisors were being told by their respective firms. However, market data indicate that de-risking into spikes turned out to be a prudent tactic.

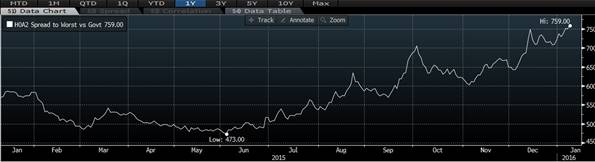

Credit spread of B-rated U.S. Corp. Bonds vs. UST Benchmarks (Source: BAML)

As you can see, following a recovery (spread narrowing) in October, high yield credit spreads trended to recent wide levels Thus, if one took advantage of, what appears to be a retail investor/wealth management-driven recovery (spread narrowing), one did oneself a favor. This is not 20/20 hindsight on my part. Since June 2014, I have warned of outright overheated conditions in the high yield credit markets. More recently, in the 10/29/15 edition of “In the Trenches” I wrote:

Slowly tightening financial conditions could help keep the economy chugging along while keeping inflation in check (not that the Fed has to worry much about inflation as currency devaluation around the world is tightening for them). However, for high risk asset (CCC-rated bonds and loans), investors could be cooked like the proverbial frog in a pot with slowly deteriorating credit conditions. In my opinion, it might be better (where suitable) to move up from the riskiest asset classes into higher-quality investments. Since the expected fed policy and global central bank policy both augur for low inflation, it is probably better to pick up yield by taking on some duration risk rather than by taking on increased credit risk. However, investor suitability should be the ultimate determining factor.

I remain very concerned with the bottom of the junk debt markets. Following a mild recovery earlier in the month, yields of CCC-rated junk debt have begun to trend higher again, even as BB-rated yields have declined. This appears to indicate a renewed rotation out of the riskiest areas of the high yield debt market. Although much of the weakness is among energy and commodities companies, continued weakness could bleed over to other sectors within the junk debt universe.

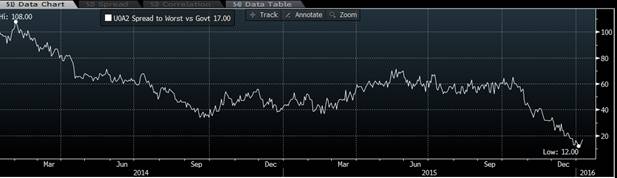

Since then, the spread widening has extended to other areas of the credit markets, including investment grade corporate bonds.

Credit spread of A-rated U.S. Corp. Bonds vs. UST Benchmarks (Source: BAML)

As you can see, A-rated corporate bond spreads have widened in recent months and during the past year. However, the widening has not been nearly as dramatic as what has occurred in the B-rated arena. The question now being asked by many investors and advisors is: Is it now a good time to enter the credit markets?

The answer is no and yes. I believe that the rout in junk debt is not quite over. Credit market participants agree that there is probably more pain to come in the high yield debt market. An article in today’s Wall Street Journal discusses the possibility that about one-third of oil producer companies could file for bankruptcy by 2017. Whether or not this comes to fruition remains to be seen, but with global demand growth for energy slowing and even higher-cost producers reluctant to cut production, a dangerous game of chicken appears underway.

Some pundits have suggested that the damage should be contained to the energy patch, but as I have stated previously, the energy boom was far-reaching with respect to the economy and to the corporate credit markets. In this evermore prepackaged world, investors tend to gain exposure to areas of the market via broad exposure (diversified portfolios). This diversification can be beneficial as a poorly-performing or troubled bond can be offset by the vast majority of holdings performing well. However, fewer investors than in the past buy and sell individual bonds on their own. Most managed portfolios (SMA, etc.) are prefabricated by the manager. Thus, one cannot simply exit the bad investment. One usually must “fire” the manager and, potentially, exit the entire portfolio. This can involve selling bonds which could be viable.

This selling can put downward price pressure on even otherwise viable high yield bonds. This results in credit spread widening and (in many cases) wider credit spreads and higher borrowing costs for high yield corporate borrowers both inside and outside a troubled sector. This is what is known as contagion.

The corporate credit markets have been pricing in weaker corporate balance sheet conditions for the past 18 months. This is especially true of junk-rated companies, many of which have seen their borrowing costs double, even as U.S. Treasury yields (interest rates) have trended lower. I believe we are witnessing a repricing of risk and a reallocation of capital along more prudent suitability lines. We are probably in the latter stages of the corporate credit storm, but like a hurricane, the back end of the storm is often the most violent part.

Sweet Child O’ Mine

We are also experiencing a repricing of risk in the municipal debt market, albeit in the opposite direction of the corporate credit markets. For nigh on seven years, the municipal credit market has been battered by pension fears, concerns about dwindling property tax revenues (in areas of the country most impacted by the housing bust), concerns about market contagion from troubled municipalities (Puerto Rico, Detroit, etc.) and (unfounded) warnings of rising interest rates. Lightening up on municipal bond holdings (and increasing high yield bond exposure) has been (and continues to be, at some firms) a core portfolio strategy. However, the data indicate that municipal credit spreads have been narrowing for more than a year.

Credit Spreads of AA-rated Municipal Bonds (Source: BAML):

What did the “port strat” folks miss?

- Investment grade municipal credit conditions have not deteriorated as feared as the economy gained traction.

- Inflation has remained tame (even outside of energy) as efficiencies and demographics contain cost increases.

- Demographic demand for reliable tax-free income has increased.

- Although municipal debt issuance has increased in recent years, it has not kept pace with the demand for reliable income (both tax-free and taxable).

- To be fair, most fixed income strategists saw this coming, but dedicated market/asset class strategists have been brushed aside at many firms.

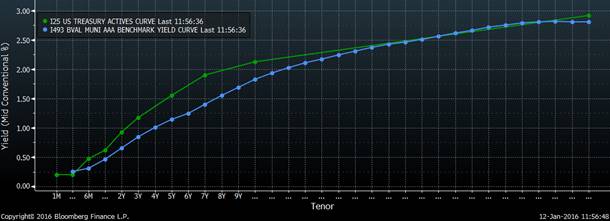

What lies ahead for municipals? On a historical basis, municipal bonds still appear attractive. After all, at one time, tax-free municipal bond yields were lower than comparable U.S. Treasury yields. This was due to their tax-free status (taxable equivalent yield). Given continuing concerns regarding municipal finance, questions over the continued tax-free status of municipal bonds, etc., it could be difficult for municipal yields to break below UST yields. However, AAA-rated Muni yields have begun to trend through UST yields.

UST yields versus AAA-rated Muni G.O. Yields (Source: Bloomberg):

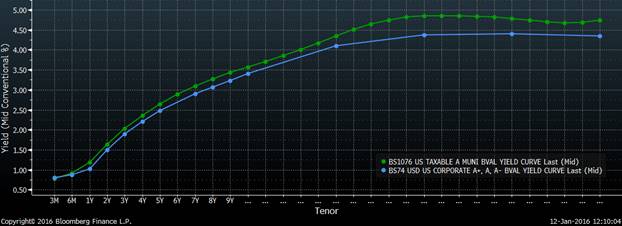

An often overlooked area of the fixed income markets are taxable munis. These are the red-headed step child of the fixed income world. As they are taxable, they are often shunned by the typical municipal bond investor/portfolio manager. Because they tend to be less liquid than corporate bonds, they are often shunned by typical (institutional) corporate bond investors and portfolio managers. The result of their mixed market parentage (taxable like a corporate bond, yet municipal obligations), taxable municipal bonds can often offer attractive opportunities for investors for whom reliable income is more important than daily liquidity. How attractive are taxable municipals? Take a look for yourself.

A-rated Taxable Muni Yields vs. A-rated U.S. Corp. Yields (Source: Bloomberg):

Even with the widening credit spreads in the corporate bond world, similarly-rated taxable municipals typically offer higher yields than their corporate counterparts, at the present time. Add to this the consensus view that, due to more stringent ratings methodology, the credit risk of A-rated taxable municipals is closer to that of AA-rated corporate bonds. In my opinion, taxable municipal bonds could be appropriate as part of buy and hold income-oriented taxable fixed income portfolios. To discuss taxable municipal bonds further, please contact me directly.

Comments

Log in or sign up to join the conversation.