Netflix (NFLX) has really become a fun name to watch come earnings season. The stock doesn’t react as harshly to the usual metrics such as earnings and revenues, and you never quite know what Reed Hastings is going to do.

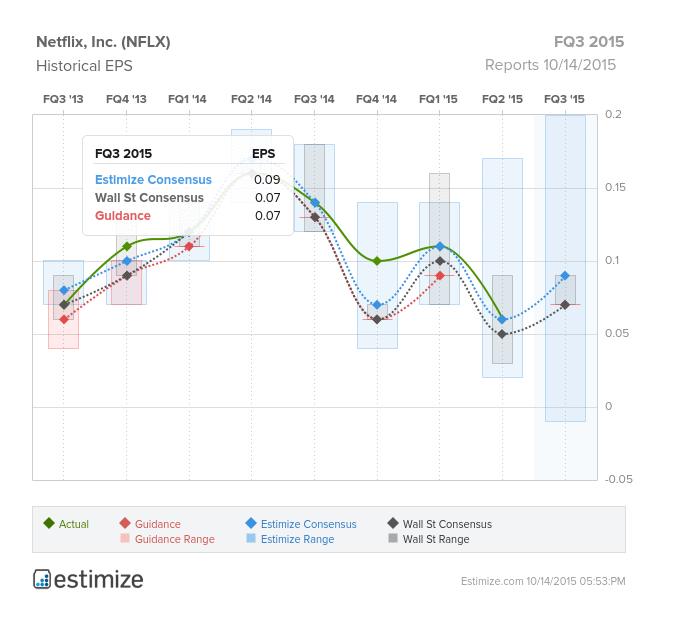

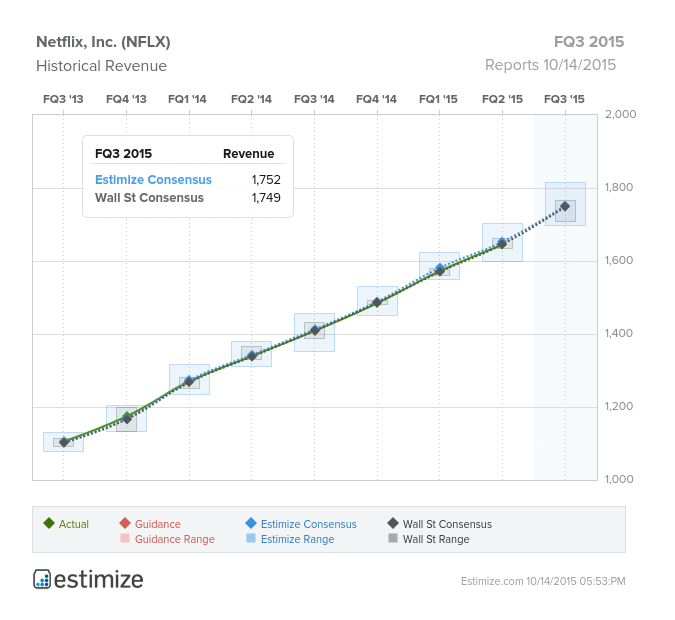

Going into the Q3 report, the Estimize consensus is calling for EPS of $0.09, two cents higher than both Wall Street and company issued guidance. Revenues of $1.75B are just about in-line. This indicates another down quarter, with YoY earnings growth of -36%, but an increase of 24% on the top-line, just about where it has been for the last 8 quarters.

Of course the metric to watch here is always subscriber numbers, consensus is calling for 1.4M net additions domestically, and 2.44M internationally, for a total of 3.84M, much higher than last quarter’s blowout results of 3.28M. There are still concerns that the domestic business is saturated at this point, and increasing competition from the likes of HBO, Comcast (CMCSA), Hulu and Amazon (AMZN) does not help. International expansion has certainly aided with user additions, while taking a bite out of the bottom-line. The company just launched in Japan last month, is getting started in Spain, Portugal and Italy this month, and is eying Hong Kong, Singapore, Taiwan and South Korea for 2016. Latin America in particular has been strong, and will only improve if rumors that Netflix may receive rights from Walt Disney to stream five “Star Wars” movies in Latin America proves true. This quarter investors will also be interested in hearing about any expansion plans in China.

Once seen as purely a content aggregator, Netflix is now a creator of it’s own wildly popular, emmy award winning, original content. However, Q3 suffers from the lack of a real hit show. The first quarter had the latest season of House of Cards, while the second quarter had Orange is the New Black. The third quarter did release Narcos which was heavily promoted, but success of the show remains to be seen. The company is relying on hits as its content obligations continues to balloon.

Due to the burdening cost of producing original content, the company announced it will be implementing a price increase. Netflix with now charge $1 more for it’s most popular “standard” subscription, bringing the price up to $9.99 a month. A similar increase in May 2014 didn’t seem to scare away customers.. the first raise since the pricing debacle of 2011 which sent customers fleeing. Raising the price to $10 puts Netflix on par with its competitors for one thing. Secondly, investors may take this as a sign that the price increase is necessary to maintain margins, especially with all of the spending that is occurring. Current customers will get grandfathered into their current subscription payment for a year, but there is always the possibility that when that expires churn will increase.

Another big question mark going forward is how the loss of Epix titles will impact the company. Netflix announced last month that they would not be renewing their deal with Epix, and as a result subscribers will no longer be able to stream franchise hits such as The Hunger Games and Transformers as well as a slew of other popular titles. Epix instead has struck a deal with Hulu, and is also available on Amazon and cable. While Netflix’s original content distinguishes the service from competitors, it still relies on popular movies and televisions shows to diversify its offerings and keep customers happy.

Overall it should be another great quarter for Netflix, but the company will have to address questions on a number of headwinds including costs, competition and churn. At this juncture investors don’t seem terribly worried, bringing the stock up 127% this year alone.

Click on image to enlarge

Comments

Log in or sign up to join the conversation.