OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ16 +0.17%) are little changed, up +0.02%, as they rebound from a fresh 3-3/4 month low as political uncertainty ahead of next Tuesday's U.S. Presidential election undercuts stocks. Dec E-mini S&PS posted a fresh 3-3/4 month low in overnight trade after Fox News reported that the FBI investigation into presidential candidate Clinton's emails has taken on a "very high priority." U.S. stock indexes recovered and European stocks rebounded from a 3-week low and are up +0.24% after the UK government lost a Brexit lawsuit over the Article 50 Brexit vote. GBP/USD jumped +1.15% to a 3-week high after the British High Court ruled that the government does not have the power to trigger Article 50 of Brexit without Parliamentary approval. Asian stocks settled mostly lower: Japan closed for holiday, Hong Kong -0.56%, China +0.84%, Taiwan -0.79%, Australia -0.07%, Singapore -0.18%, South Korea +0.03%, India -0.35%. China's Shanghai Composite bucked the negative trend and posted a 9-1/2 month high as industrial stocks rallied on speculation government policy will remain supportive of fiscal spending and infrastructure projects to support growth.

The dollar index (DXY00 -0.04%) is down -0.17% at a 3-week low. EUR/USD (^EURUSD) is down -0.20%. USD/JPY (^USDJPY) is down -0.11% at a 4-week low as U.S. political uncertainty undercuts stocks and fuels safe-haven demand for the yen.

Dec 10-year T-note prices (ZNZ16 +0.01%) are unchanged.

The Eurozone Sep unemployment rate was unch at 10.0%, right on expectations and remained at a 5-1/3 year low.

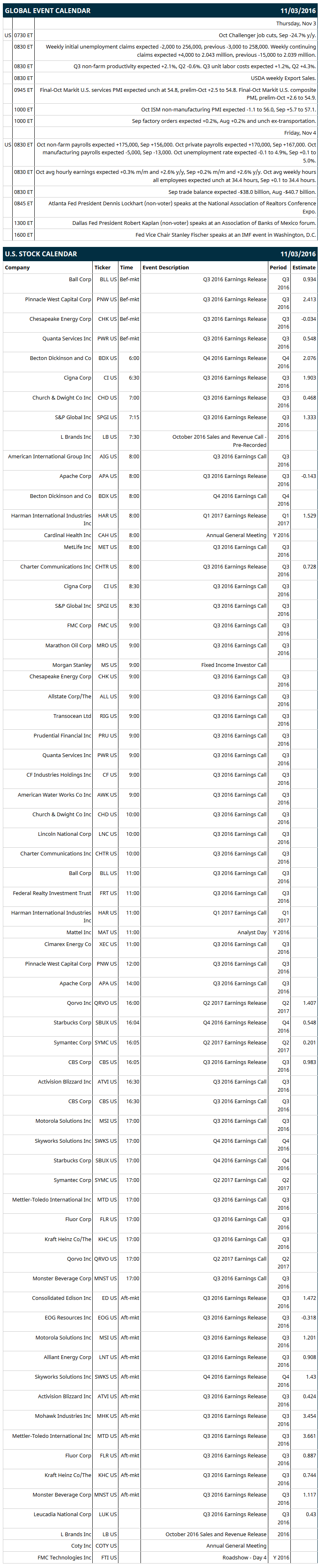

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) Oct Challenger job cuts (Sep -24.7% y/y), (2) weekly initial unemployment claims (expected -2,000 to 256,000, previous -3,000 to 258,000) and continuing claims (expected +4,000 to 2.043 million, previous -15,000 to 2.039 million), (3) Q3 non-farm productivity (expected +2.1%, Q2 -0.6%) and Q3 unit labor costs (expected +1.2%, Q2 +4.3%), (4) final-Oct Markit U.S. services PMI (expected unch at 54.8, prelim-Oct +2.5 to 54.8), (5) Oct ISM non-manufacturing PMI (expected -1.1 to 56.0, Sep +5.7 to 57.1), (6) Sep factory orders (expected +0.2%, Aug +0.2% and unch ex-transportation), (7) USDA weekly Export Sales.

Notable S&P 500 earnings reports today include: Starbucks (0.55), Church & Dwight ((0.47), S&P Global (1.33), Apache (-0.14), Charter Communications (0.73), Symantec (0.20), CBS (0.98), Consolidated Edison (1.47), Motorola Solutions (1.20), Alliant Energy (0.91), Fluor (0.89), Kraft Heinz (0.74), Monster Beverage (1.12), among others.

U.S. IPO's scheduled to price today: Smart Sand (SND).

Equity conferences during the remainder of this week include: Needham Next-Gen Storage Networking Conference on Wed, Goldman Sachs Industrials Conference on Wed-Thu, BancAnalysts Association of Boston Conference on Thu-Fri.

OVERNIGHT U.S. STOCK MOVERS

Newmont Mining (NEM -2.03%) was upgraded to 'Overweight' from 'Neutral' at JPMorgan Chase with a price target of $43.

NXP Semiconductors (NXPI -0.52%) was downgraded to 'Neutral' from 'Buy' at Mizuho Securities with a 12-month target price of $110.

Facebook (FB -1.80%) dropped 6% in after-hours trading after CFO Wehner said that ad sales growth will "come down meaningfully starting mid-2017."

Zumiez (ZUMZ +1.79%) climbed over 9% in after-hours trading after it reported October comparable sales rose +10.2%, higher than consensus of +2.6%, and said it seesQ3 adjusted EPS of 35 cents-36 cents, better than consensus of 29 cents-30 cents.

Fitbit (FIT -1.91%) sank nearly 30% in after-hours trading after it said it sees Q4 adjusted EPS of 14 cents-18 cents, well below consensus of 75 cents.

Take-Two Interactive Software (TTWO +1.98%) rallied 5% in after-hours trading after it reported Q2 adjusted revenue of $479.4 million, higher than consensus of $402.5 million, and then raised its fiscal 2017 bookings estimate to $1.6 billion-$1.7 billion from an August 4 estimate of $1.5 billion-$1.6 billion.

Wynn Resorts Ltd. (WYNN -1.74%) fell 5% in after-hours trading after it reported Q3 Macau adjusted property Ebitda of $151 million, below consensus of $205.7 million

Transocean Ltd. (RIG -3.13%) climbed nearly 2% in after-hours trading after it reported Q3 adjusted EPS of 25 cents, higher than consensus of 14 cents.

Marathon Oil (MRO -3.69%) gained over 1% in after-hours trading after it reported a Q3 adjusted loss of -11 cents a share, a smaller loss than expectations of -19 cents.

Flotek Industries (FTK -2.92%) slid nearly 3% in after-hours trading after it reported Q3 revenue of $73.7 million, less than consensus of $76.9 million.

Hologic (HOLX -0.81%) rose 3% in after-hours trading after it reported Q4 adjusted EPS of 52 cents, above consensus of 50 cents, and then said it sees fiscal 2017 revenue of $2.94 billion-$2.98 billion, higher than consensus of $2.94 billion.

Diplomat Pharmacy (DPLO -0.89%) plunged over 25% in after-hours trading after it reported Q3 adjusted EPS of 21 cents, below consensus of 24 cents, and then cut its 2016 adjusted EPS estimate to 83 cents-87 cents from an August 9 view of 90 cents-95 cents.

Inteliquent (IQNT -0.12%) surged over 30% in after-hours trading after GTCR agreed to buy the company for $800 million or $23 a share.

Zynga (ZNGA -2.14%) fell 3% in after-hours trading after it reported a Q3 GAAP loss of -4 cents a share, a bigger loss than expectations of -3 cents, and then said it sees Q4 revenue of $180 million0$190 million, weaker than consensus of $204.3 million.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ16 +0.17%) this morning are little changed, up +0.50 of a point (+0.02%). Wednesday's closes: S&P 500 -0.65%, Dow Jones -0.43%, Nasdaq -0.84%. The S&P 500 on Wednesday fell to a 3-3/4 month low and closed lower on concerns about next week's U.S. election and on weakness in energy-producer stocks after the price of crude oil tumbled -2.85% to a 5-week low. Stocks were also undercut by the post-FOMC statement that said the pace of price gains "has increased somewhat since earlier this year," which bolsters the case for a Fed rate hike next month.

Dec 10-year T-notes (ZNZ16 +0.01%) this morning are unchanged. Wednesday's closes: TYZ6 +7.50, FVZ6 +4.00. Dec 10-year T-notes on Wednesday closed higher on increased safe-haven demand with the sell-off in stocks and the uncertainty about next week's U.S. election. T-notes were undercut by the FOMC's slightly more hawkish language in its post-meeting statement that increased the odds of a December rate hike.

The dollar index (DXY00 -0.04%) this morning is down -0.161 (-0.17%) at fresh 3-week low. EUR/USD (^EURUSD) is down -0.0022 (-0.20%). USD/JPY (^USDJPY) is down -0.11 (-0.11%). Wednesday's closes: Dollar index -0.301 (-0.31%), EUR/USD +0.0043 (+0.39%), USD/JPY -0.85 (-0.82%). The dollar index on Wednesday fell to a 3-week low and closed lower on uncertainty about next week's U.S. election and on the FOMC's decision not to raise interest rates at Wednesday's FOMC meeting. There was also strength in EUR/USD which climbed to a 3-week high after Eurozone Oct Markit manufacturing PMI was revised upward to a 2-3/4 year high, which reduced the chances for additional ECB stimulus.

Dec crude oil prices (CLZ16 +0.90%) are up +34 cents (+0.75%) and Dec gasoline (RBZ16 +0.59%) is up +0.0102 (+0.70%). Wednesday's closes: Dec crude -1.33 (-2.85%), Dec gasoline +0.0440 (+3.10%). Dec crude oil and gasoline on Wednesday closed lower with Dec crude at a 5-week low. Crude oil prices were undercut by the +14.42 million bbl surge in EIA crude inventories (versus expectations of +2.0 million bbl) and by the +3.9% y/y increase in Russia Oct crude production to a post-Soviet record of 11.2 million bpd. Crude oil was also undercut by the +170,00 bpd increase in OPEC Oct crude production to a record 34.02 million bpd.

(Click on image to enlarge)

Comments

Log in or sign up to join the conversation.