OVERNIGHT MARKETS AND NEWS

Mar E-mini S&Ps (ESH18 +0.20%) this morning are up +0.14% at a fresh record nearest-futures high and European stocks are up +1.21%. Stock markets around the world are moving higher on optimism the global economic expansion can continue. Energy stocks are gaining with Feb WTI crude oil (CLG18 +0.31%) up +0.32% at a new 2-1/2 year high on signs of tighter oil supplies after data late yesterday from API showed U.S. crude inventories fell -4.99 million bbl last week. European stocks also found support on signs of stronger economic growth after the Eurozone Dec Markit composite PMI was revised upward to a 6-3/4 year high of 58.1. Asian stocks settled mostly higher: Japan +3.26%, Hong Kong +0.57%, China +0.49%, Taiwan +0.44%, Australia +0.11%, Singapore +1.06%, South Korea -0.78%, India +0.52%. China's Shanghai Composite posted a 1-1/4 month high after JPMorgan Chase raised their China 2018 GDP forecast to 6.7% from 6.5%, citing an "upbeat external outlook." Japan's Nikkei Stock Index reopened after holiday and surged over 3% to a 26 year high on strength in technology and banking stocks.

The dollar index (DXY00 -0.28%) is down -0.30%. EUR/USD (^EURUSD) is up +0.38%. USD/JPY (^USDJPY) is up +0.09%.

Mar 10-year T-note prices (ZNH18 -0.15%) are down -5 ticks.

The China Dec Caixin services PMI rose +2.0 to 53.9, stronger than expectations of -0.1 to 51.8.

The Eurozone Dec Markit composite PMI was revised upward to a 6-3/4 year high of 58.1 from the originally reported 58.0.

The UK Dec Markit/CIPS services PMI rose +0.4 to 54.2, stronger than expectations of +0.2 to 54.0.

U.S. STOCK PREVIEW

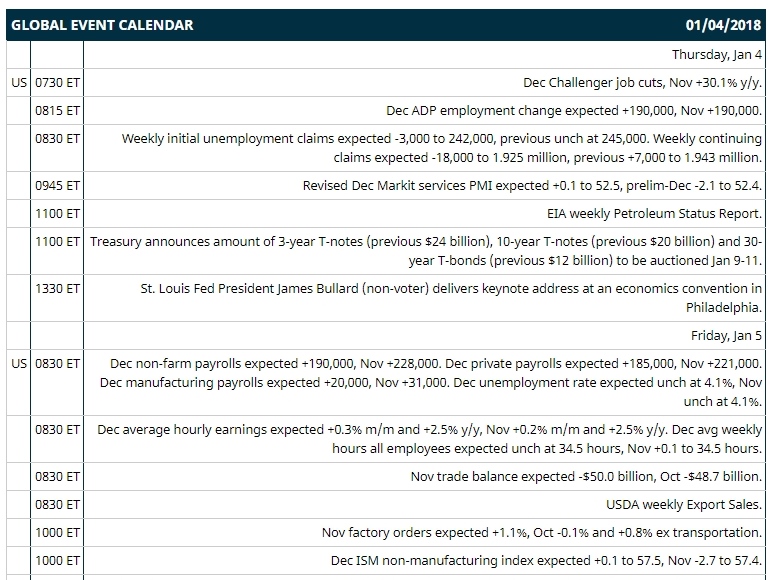

Key U.S. news today includes: (1) Dec Challenger job cuts (Nov +30.1% y/y), (2) Dec ADP employment change (expected +190,000, Nov +190,000), (3) weekly initial unemployment claims (expected -3,000 to 242,000, previous unch at 245,000) and continuing claims (expected -18,000 to 1.925 million, previous +7,000 to 1.943 million), (4) revised Dec Markit services PMI (expected +0.1 to 52.5, prelim-Dec -2.1 to 52.4), (5) EIA weekly Petroleum Status Report, (6) St. Louis Fed President James Bullard (non-voter) delivers keynote address at an economics convention in Philadelphia.

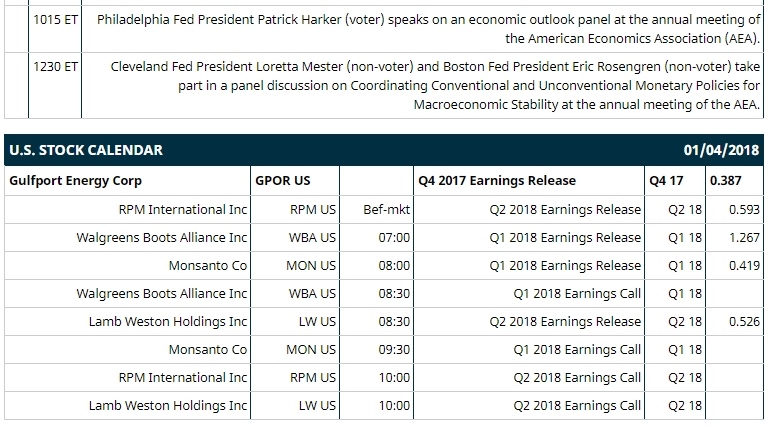

Notable Russell 1000 earnings reports today include: Monsanto (consensus $0.42), Walgreens (1.27), RPM Intl (0.59), Gulfport Energy (0.39), Lamb Weston (0.53).

U.S. IPO's scheduled to price today: none.

Equity conferences this week: Goldman Sachs Health Care Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

Mastercard (MA +1.26%) was upgraded to 'Buy' from 'Neutral' at Mizuho Securities USA with a price target of $175.

CVS Health Corp (CVS -0.44%) was upgraded to 'Strong Buy' from 'Outperform' at Raymond James with a 12-month target price of $90.

Advanced Micro Devices (AMD +5.19%) gained almost 3% in after-hours trading after it said it sees "near zero risk" to its chips related to Intel's problem.

Intel (INTC -3.39%) fell nearly 2% in after-hours trading after it said an exploit in its chips allows access to privileged information and a fix will take time to deploy.

Visteon (VC +1.69%) was rated a new 'Buy' at Guggenheim Securities with a 12-month target price of $140.

Marathon Oil (MRO +1.67%) was upgraded to 'Buy' from 'Neutral' at Bank of America/Merrill Lynch with a price target of $21.

Zumiez (ZUMZ +2.50%) rallied 13% in after-hours trading after it reported Dec comparable sales rose +7.9%, better than expectations of +4.1%, and then boosted its Q4 EPS forecast to 88 cents-90 cents, higher than consensus of 80 cents.

Tesla (TSLA -1.02%) lost nearly 2% in after-hours trading after it pushed back its goal to assemble 5,000 Model 3s cars by June, three months longer than previous expectations of 5,000 cars assembled by March.

Qiagen (QGEN +1.82%) was rated a new 'Outperform' at Evercore ISI with a 12-month target price of $35.

Alexandria Real Estate Equities (ARE -0.47%) fell 3% in after-hours trading after it announced that it had commenced an underwritten public offering of 6.0 million shares of common stock.

Momenta Pharmaceuticals (MNTA -1.39%) climbed 6% in after-hours trading after it said it will begin a trial in the first half of 2018 with Mylan for its M710 injection in patients with diabetic macular edema.

Seaspan (SSW -0.70%) rose almost 2% in after-hours trading after Fairfax Financial Holdings said it will invest $250 million is Seaspan in exchange for unsecured debentures and Class A common share purchase warrants.

Gener8 Maritime (GNRT +1.21%) fell 4% in after-hours trading after it was downgraded to 'Neutral' from 'Buy' at UBS.

Fang Holdings Ltd (SFUN -3.00%) slid nearly 4% in after-hours trading after a block of 15.5 million shares of Fang were offered at $4.90-$5.10 via Morgan Stanley.

Rite Aid (RAD -0.94%) dropped nearly 10% in after-hours trading after it reported Q3 revenue of $5.35 billion, below consensus of $7.64 billion.

MARKET COMMENTS

Mar S&P 500 E-mini stock futures (ESH18 +0.20%) this morning are up +3.75 points (+0.14%) at a fresh record nearest-futures high. Wednesday's closes: S&P 500 +0.64%, Dow Jones +0.40%, Nasdaq +0.99%. The S&P 500 on Wednesday rallied to a new record high and closed higher on signs the U.S. economic expansion will continue after the Dec ISM manufacturing index rose +1.5 to 59.7, stronger than expectations of unchanged at 58.2, as the new orders sub-index climbed +5.4 to a nearly 14-year high of 69.4. There was also strength in energy stocks as Feb WTI crude oil rose +2.09% to a new 2-1/2 year high.

Mar 10-year T-note prices (ZNH18 -0.15%) this morning are down -5 ticks. Wednesday's closes: TYH8 +3.00, FVH8 +0.25. Mar 10-year T-notes on Wednesday closed higher on positive carry-over from a rally in German bunds and on the Dec 13-14 FOMC meeting minutes that stated policy makers still expected a "gradual" approach to raising interest rates. T-notes were undercut by reduced safe-haven demand as stocks rallied to a new all-time high.

The dollar index (DXY00 -0.28%) this morning is down -0.272 (-0.30%). EUR/USD (^EURUSD) is up +0.0046 (+0.38%) and USD/JPY (^USDJPY) is up +0.10 (+0.09%). Wednesday's closes: Dollar Index +0.290 (+0.32%), EUR/USD -0.0044 (-0.36%), USD/JPY +0.22 (+0.20%). The dollar on Wednesday closed higher on the stronger-than-expected U.S. Dec ISM manufacturing index, which bolsters the case for additional Fed tightening, and on the rally in the S&P 500 to a new record high, which boosted USD/JPY on reduced safe-haven demand for the yen.

Feb crude oil (CLG18 +0.31%) this morning is up +20 cents (+0.32%) at a new 2-1/2 year high and Feb gasoline (RBG18+0.08%) is +0.0018 (+0.10%). Wednesday's closes: Feb WTI crude +1.26 (+2.09%), Feb gasoline +0.0343 (+1.95%). Feb crude oil and gasoline on Wednesday closed higher with Feb crude at a 2-1/2 year high. Crude oil prices were boosted by the rally in the S&P 500 to a new all-time high, which shows confidence in the economic outlook and is supportive for energy demand, and by expectations for Thursday's weekly EIA crude inventories to fall -5.0 million bbl to a 2-year low, the seventh consecutive weekly decline.

Metals prices this morning are mixed with Feb gold (GCG18 -0.42%) -4.1 (-0.31%), Mar silver (SIH18 -0.65%) -0.087(-0.50%) and Mar copper (HGH18 +0.89%) +0.032 (+0.98%). Wednesday's closes: Feb gold +2.4 (+0.18%), Mar silver +0.061 (+0.35%), Mar copper -0.0205 (-0.63%). Metals on Wednesday settled mixed with Feb gold at a 3-1/4 month high, Mar silver at a 1-month high and Mar copper at a 1-week low. Metals prices were boosted by the stronger-than-expected U.S. Dec ISM manufacturing index, which is positive for copper demand, and by the increased North Korean tensions which boosted safe-haven demand for gold. Metals prices were undercut by a stronger dollar and by the rally in the S&P 500 to a new record high, which reduces the safe-haven demand for precious metals.

Comments

Log in or sign up to join the conversation.