OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ15 +0.03%) are down -0.08% and European stocks are down -0.61% at a 1-week low on disappointment in company Q3 earnings results. Intel is down nearly 3% in pre-market trading after saying a slowdown in demand may curb sales at its server-chip division, and JPMorgan Chase is down over 1% in pre-market trading after Q3 earnings came in below expectations. Losses were limited on a possible increase in M&A activity as SanDisk jumped nearly 10% in pre-market trading after it was said to hire a bank to explore a potential sale of the company. Asian stocks settled lower: Japan -1.89%, Hong Kong -0.71%, China -0.93%, Taiwan -0.53%, Australia -0.11%, Singapore -0.03%, South Korea -0.45%, India-0.25%. China's Shanghai Composite closed lower for the first time in six sessions and Japan's Nikkei Stock Index fell to a 1-week low on deflation concerns in China after China Sep producer prices fell -5.9% y/y, the fastest pace of decline in 6-years and the 43rd consecutive month that producer prices have been negative.

The dollar index (DXY00 -0.21%) is down -0.26% at a 3-week low on speculation the slowdown in China may prompt the Fed to keep interest rates lower for longer. EUR/USD (^EURUSD) is up +0.29% at a 3-week high. USD/JPY (^USDJPY) is down -0.23% at a 1-week low.

Dec T-note prices (ZNZ15 +0.11%) are up +4.5 ticks.

China Sep CPI rose +1.6% y/y, less than expectations of +1.8% y/y. Sep PPI fell -5.9% y/y, right on expectations and matched Aug's drop as the steepest pace of decline in 6 years.

U.S. STOCK PREVIEW

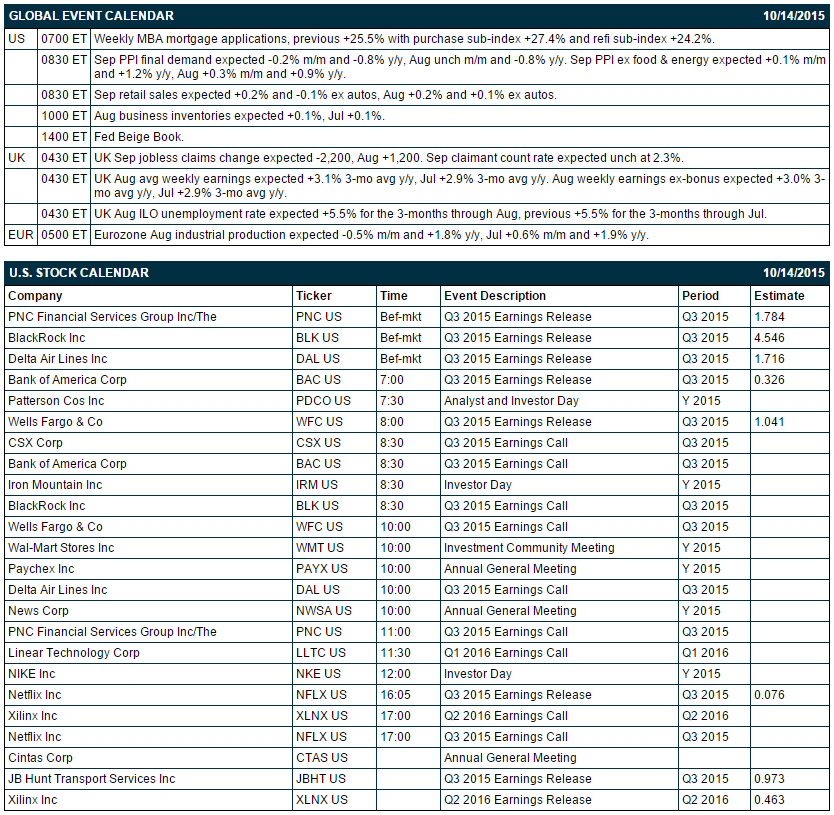

Key U.S. news today includes: (1) weekly MBA mortgage applications (previous +25.5% with purchase sub-index +27.4% and refi sub-index +24.2%), (2) Sep final-demand PPI (expected -0.2% m/m and -0.8% y/y, Aug unch m/m and -0.8% y/y) and Sep PPI ex food & energy (expected +0.1% m/m and +1.2% y/y, Aug +0.3% m/m and +0.9% y/y), (3) Sep retail sales (expected +0.2% and -0.1% ex autos, Aug +0.2% and +0.1% ex autos), (4) Aug business inventories (expected +0.1%, Jul +0.1%), and (5) the Fed's Beige Book.

There are 8 of the S&P 500 companies report earnings today: Bank of America (consensus $0.33), Blackrock (4.55), PNC (1.78), Wells Fargo (1.04), Netflix (0.08), JB Hunt (0.97), Delta Air Lines (1.72), Xilinx (0.46).

U.S. IPO's scheduled to price today: First Data (FDC), Albertsons (ABS).

Equity conferences during the remainder of this week include: Energy Storage North America Conference on Thu, and Moody's UK Water Sector Conference on Thu.

OVERNIGHT U.S. STOCK MOVERS

JPMorgan Chase (JPM -0.28%) fell over 1% in pre-market trading after it reported Q3 adjusted EPS of $1.29, below consensus of $1.38.

Intel (INTC -0.53%) slid nearly 3% in pre-market trading after it reported Q3 EPS of 64 cents, better than consensus of 59 cents, but then projected a slowdown in corporate server demand as businesses scale back capital spending plans.

BlackRock (BLK -0.17%) reported Q3 EPS of $5.00, above consensus of $4.53.

Bank of America (BAC unch) reported Q3 EPS of 35 cents, higher than consensus of 33 cents.

PNC Financial Services Group (PN -0.71%)C reported Q3 EPS of $1.72, weaker than consensus of $1.78.

Delta Air Lines (DAL -1.59%) reported Q3 EPS of $1.74, better than consensus of $1.72.

GoPro (GPRO -1.72%) fell nearly 2% and Under Armour (UA -1.98%) dropped over 1% in after-hours trading after Piper Jaffray downgraded both stocks to 'Neutral' from 'Overweight.'

CSX Corp. (CSX -2.33%) climbed nearly 2% in after-hours trading after it reported Q3 EPS of 52 cents, higher than consensus of 50 cents.

SanDisk (SNDK -1.72%) jumped almost 10% in after-hours trading and Micron (MU +0.83%) rose nearly 3% after Bloomberg reported that SanDisk hired a bank to explore a possible sale and received interest from Micron.

Cepheid (CPHD -8.61%) sank 11% in after-hours trading after it reported a Q3 EPS loss of -13 cents, more than double consensus of a -6 cent loss, and then cut guidance on fiscal 2015 revenue to $537 million to $541 million from a July estimate of $544 million to $553 million, below consensus of $549.8 million.

Linear Technology (LLTC -0.19%) gained over 3% in after-hours trading after it reported Q1 EPS of 46 cents, right on consensus, but said Q2 revenue would be $341.9 million to $352.2 million, above consensus of $339.2 million.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ15 +0.03%) this morning are down -1.50 points (-0.08%). Tuesday's closes: S&P 500 -0.68%, Dow Jones -0.29%, Nasdaq-0.68%. The S&P 500 on Tuesday retreated from a 1-1/2 month high and closed lower on global growth concerns after China Sep imports dropped-20.4% y/y, a bigger decline than expectations of -16.0% y/y and the largest decline in 7 months. There was also carryover weakness from a slide in European stocks after the German ZEW survey expectations of economic growth fell -10.2 to a 1-year low of 1.9. On the positive side, there was increased M&A activity after Anheuser-Busch InBev NV bought SABMiller Plc for $106 billion.

Dec 10-year T-notes (ZNZ15 +0.11%) this morning are up +4.5 ticks. Tuesday's closes: TYZ5 +3.00, FVZ5 +2.75. Dec T-notes on Tuesday closed higher on hopes for a delayed Fed rate hike after China Sep imports fell by the most in 7 months. In addition, the 10-year T-note breakeven inflation expectations rate fell to a 1-week low.

The dollar index (DXY00 -0.21%) this morning is down-0.243 (-0.26%) at a 3-week low. EUR/USD (^EURUSD) is up +0.0033 (+0.29%) at a 3-week high. USD/JPY (^USDJPY) is down -0.27 (-0.23%) at a 1-week low. Tuesday's closes: Dollar Index -0.082 (-0.09%), EUR/USD +0.0021 (+0.18%), USD/JPY -0.29 (-0.24%). The dollar index on Tuesday fell to a 3-week low and closed lower on reduced Fed rate hike concerns after the -20.4% y/y plunge in China Sep imports, the most in 7 months, and the decline in the 10-year T-note breakeven inflation expectations rate to a 1-week low.

Nov crude oil this morning is down -10 cents (-0.21%) at a 1-week low and Nov gasoline is down -0.0035 (-0.27% at a 1-month low. Tuesday's closes: CLX5 -0.44 (-0.93%), RBX5 -0.0288 (-2.15%). Nov crude oil and gasoline prices on Tuesday closed lower with Nov gasoline at a 1-week low. Energy prices were undercut by the sell-off in stocks and expectations for weekly EIA crude inventories to climb +2.6 million bbl. A supportive factor for crude was signs of strong Chinese demand for crude with China Jan-Sep crude imports of 249 MMT. up +8.8% y/y and the most in 5 years.

Comments

Log in or sign up to join the conversation.