OVERNIGHT MARKETS AND NEWS

December E-mini S&Ps (ESZ15 -0.02%) are down -0.05% and European stocks are down -0.53% ahead of the release of U.S. Oct payrolls that may provide a clue as to whether the U.S. economy is ready for an interest rate increase. Losses in European stocks accelerated after German Sep industrial production unexpectedly declined at the fastest pace in 13 months. Asian stocks settled mixed: Japan +0.78%, Hong Kong -0.80%, China +1.91%, Taiwan -1.77%, Australia +0.42%, Singapore -0.44%, South Korea -0.61%, India -0.15%. China's Shanghai Composite climbed to a 2-1/2 month high as brokerage stocks rallied on speculation China will lift a freeze on initial public offerings by year-end, which the China Securities Regulatory Commission confirmed after the market close. Japan's Nikkei Stock Index rose to a 2-1/2 month high, led by gains in exporters, on the prospects of improved earnings as the yen fell to near a 2-1/2 month low against the dollar.

The dollar index (DXY00 +0.17%) is up +0.16% at a 2-3/4 month high. EUR/USD (^EURUSD) is down -0.07%. USD/JPY (^USDJPY) is up +0.14%.

Dec T-note prices (ZNZ15 +0.06%) are up +4.5 ticks.

ECB Executive Board member Mersch said "monetary policy will remain accommodative for an extended period of time and the ECB will also ensure that inflation returns back towards our objective."

German Sep industrial production unexpectedly fell -1.1% m/m, weaker than expectations of +0.5% m/m and the largest decline in 13 months.

U.S. STOCK PREVIEW

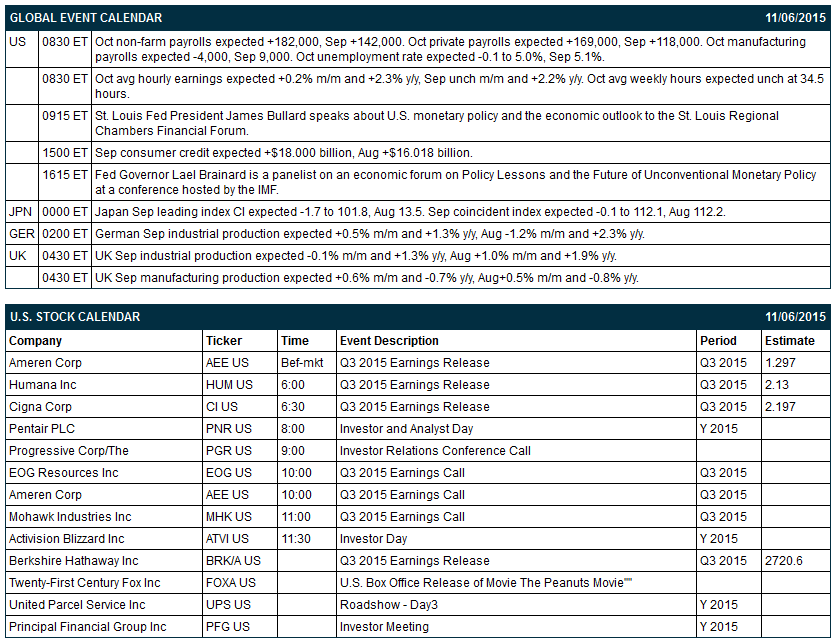

Key U.S. news today includes: (1) Oct non-farm payrolls (expected +182,000, Sep +142,000) and the Oct unemployment rate (expected -0.1 to 5.0%, Sep 5.1%), (2) St. Louis Fed President James Bullard's speech on U.S. monetary policy and the economic outlook to the St. Louis Regional Chamber’s Financial Forum, (3) Sep consumer credit (expected +$18.000 billion, Aug +$16.018 billion), and (4) Fed Governor Lael Brainard appearance as a panelist on an economic forum on “Policy Lessons and the Future of Unconventional Monetary Policy” at a conference hosted by the IMF.

There are 4 of the S&P 500 companies that report earnings today: Berkshire Hathaway (consensus $2720), Humana (2.13), Cigna (2.20), and Ameren (1.30).

U.S. IPO's scheduled to price today: none.

Equity conferences today include: Bernstein Technology Innovation Summit on Thu-Fri, BancAnalysts Association of Boston Conference on Thu-Fri.

OVERNIGHT U.S. STOCK MOVERS

Cigna (CI +1.89%) reported Q3 EPS of $2.28, better than consensus of $2.20.

Humana (HUM +1.23%) reported Q3 EPS of $2.16, higher than consensus of $2.13.

Disney (DIS -0.22%) fell 2% in after-hours trading after it reported Q4 adjusted EPS of $1.20, better than consensus of $1.14, but Q4 revenue of $13.50 billion was below consensus of $13.56 billion.

Mohawk Industries (MHK -0.36%) slipped 5% in after-hours trading after it reported Q3 adjusted EPS of $2.98, less than consensus of $2.99, and then lowered guidance on Q4 adjusted EPS to $2.66-$2.75, below consensus of $2.75.

Monster Beverage (MNST -0.44%) climbed over 8% in after-hours trading after it reported Q3 EPS of 84 cents, better than consensus of 81 cents.

Nvidia (NVDA -1.14%) jumped nearly 8% in after-hours trading after it reported Q3 adjusted EPS of 46 cents, well above consensus of 25 cents.

TripAdvisor (TRIP +0.59%) dropped over 9% in after-hours trading after it reported Q3 adjusted EPS of 53 cents, weaker than consensus of 54 cents.

Weight Watchers (WTW +2.61%) jumped over 6% in after-hours trading after it reported Q3 adjusted EPS of 39 cents, higher than consensus of 29 cents, and then raised guidance on fiscal 2015 EPS to 64 cents-74 cents from 57 cents-72 cents, above consensus of 67 cents.

Men's Wearhouse (MW -0.84%) plunged over 25% in after-hours trading after it cut its preliminary Q3 EPS view to 46 cents-51 cents, well below consensus of 87 cents, and then lowered guidance on fiscal 2015 EPS to $1.75-$2.00 from a previous estimate of $2.70-$2.90, well below consensus of $2.78.

CyberArk (CYBR -4.55%) rose 2% in after-hours trading after it reported Q3 adjusted EPS of 26 cents, double consensus of 13 cents, and then raised guidance on fiscal 2015 adjusted EPS to 80 cents-82 cents from an August estimate of 62 cents-65 cents, better than consensus of 64 cents.

Tableau Software (DATA -3.89%) surged over 15% in after-hours trading after it reported Q3 adjusted EPS of 14 cents, double consensus of 7 cents.

Skyworks Solutions (SWKS +0.12%) climbed nearly 4% in after-hours trading after it reported Q4 adjusted EPS of $1.52, right on consensus, but then raised guidance on Q1 adjusted EPS to $1.60, better than consensus of $1.56.

Kraft Heinz (KHC -0.53%) fell 1% in after-hours trading after it reported Q2 adjusted EPS of 44 cents, below consensus of 59 cents.

Shake Shack (SHAK +4.48%) rose over 6% in after-hours trading after it reported Q3 adjusted EPS of 12 cents, higher than consensus of 7 cents.

MARKET COMMENTS

Dec E-mini S&Ps (ESZ15 -0.02%) this morning are down -1.00 point (-0.05%). Thursday's closes: S&P 500 -0.11%, Dow Jones -0.02%, Nasdaq -0.31%. The S&P 500 on Thursday closed lower on the unexpected +16,000 increase in U.S. weekly initial unemployment claims to 276,000 and on weakness in health-care stocks as Valeant Pharmaceuticals fell to a 2-1/2 year low.

Dec 10-year T-notes (ZNZ15 +0.06%) this morning are up +4.5 ticks. Thursday's closes: TYZ5 -2.00, FVZ5 -1.75. Dec T-notes on Thursday fell to a new 3-month nearest-futures low and closed lower on carryover bearishness from Wednesday's comment from Fed Chair Yellen that a Dec FOMC rate hike is a "live possibility" if the U.S. economy continues to perform well. T-notes also saw long liquidation pressure ahead of Friday's U.S. Nov payrolls report.

The dollar index (DXY00 +0.17%) this morning is up +0.153 (+0.16%) at a fresh 2-3/4 month high. EUR/USD (^EURUSD) is down -0.0008 (-0.07%). USD/JPY (^USDJPY) is up +0.17 (+0.14%). Thursday's closes: Dollar Index -0.014 (-0.01%), EUR/USD +0.0018 (+0.17%), USD/JPY +0.18 (+0.15%). The dollar index on Thursday climbed to a 2-3/4 month high but fell back and closed little changed. The dollar index continued to receive a boost from Wednesday's comment from Fed Chair Yellen that an interest rate increase at the Dec FOMC meeting is a "live possibility." Meanwhile, EUR/USD fell to a new 3-1/2 month low on the unexpected declines in the Eurozone Sep retail sales and German Sep factory orders reports, which may help prompt the ECB to expand QE. The dollar fell back from its best levels on long liquidation pressure ahead of Friday's U.S. Oct payroll report.

Dec crude oil (CLZ15 +0.58%) this morning is up +34 cents (+0.75%) and Dec gasoline (RBZ15 +2.15%) is up +0.0310 (+2.28%). Thursday's closes: CLZ5 -0.93 (-2.016%), RBZ5 -0.0194 (-1.39%). Dec crude oil and gasoline on Thursday closed lower with Dec crude at a 1-week low. Crude oil prices were undercut by the rally in the dollar index to a 2-3/4 month high and by the ongoing U.S. crude supply glut with U.S. crude inventories more than 100 million bbls above the 5-year seasonal average.

(Click on image to enlarge)

Comments

Log in or sign up to join the conversation.