OVERNIGHT MARKETS AND NEWS

June E-mini S&Ps (ESM15 -0.23%) this morning are down -0.54% at a 1-month low and European stocks are down -1.35% at a 2-1/2 month low amid carry-over selling from Wednesday's rout after Fed Chair Yellen said equity market valuations are high. The slide in global government bond markets continued as well after Fed Chair Yellen said that long-term rates are low and could jump when the Fed begins to raise interest rates. The German 10-year bund yield climbed to a 4-3/4 month high of .777% and the U.S. 10-year T-note yield rose to a 4-3/4 month high of 2.31%. On the positive side, Greece's ASE Stock Index is up +2.39% as bank stocks rose after the ECB boosted emergency funding to Greece's central bank. The yield on the Greek 10-year bond fell -33 bp to 10.90% after the ECB raised the cap on Emergency Liquidity Assistance to the Greek central bank by 2 billion euros to 78.9 billion euros. Asian stocks closed lower: Japan -1.23%, Hong Kong -1.27%, China -2.77%, Taiwan -1.16%, Australia -0.82%, Singapore -0.78%, South Korea -0.59%, India -0.44%. China's Shanghai Composite slid to a 3-week low after Morgan Stanley downgraded Chinese stocks for the first time in 7 years to 'Equalweight' from 'Overweight,' citing the weakest corporate profits since 2009.

Commodity prices are mixed. Jun crude oil (CLM15 +0.13%) is down -0.03% and Jun gasoline (RBM15 -0.27%) is down -0.39%. Metals prices are mixed. Jun gold (GCM15 -0.42%) is down -0.60%. Jul copper (HGN15 +0.12%) is up +0.29%. Agriculture prices are mixed.

The dollar index (DXY00 +0.10%) is up +0.02%. EUR/USD (^EURUSD) is down -0.15%. USD/JPY (^USDJPY) is down -0.28%.

Jun T-note prices (ZNM15 +0.11%) are down -5.5 ticks at a 1-3/4 month low on negative carry-over from a slide in global bond markets. The yield on the 10-year Germany bund jumped to a 4-3/4 month high on .777% and has surged over 60 bp in the past week.

According to two officials who spoke on conditions of anonymity, ECB officials want progress at Monday's meeting of Eurozone finance ministers with Greece in reaching an agreement with international creditors or they will consider tightening Greek banks' access to emergency liquidity. One official said that are prepared to raise haircuts, the discounts imposed on collateral pledged by Greek banks in return for funding, to levels seen last year.

U.S. STOCK PREVIEW

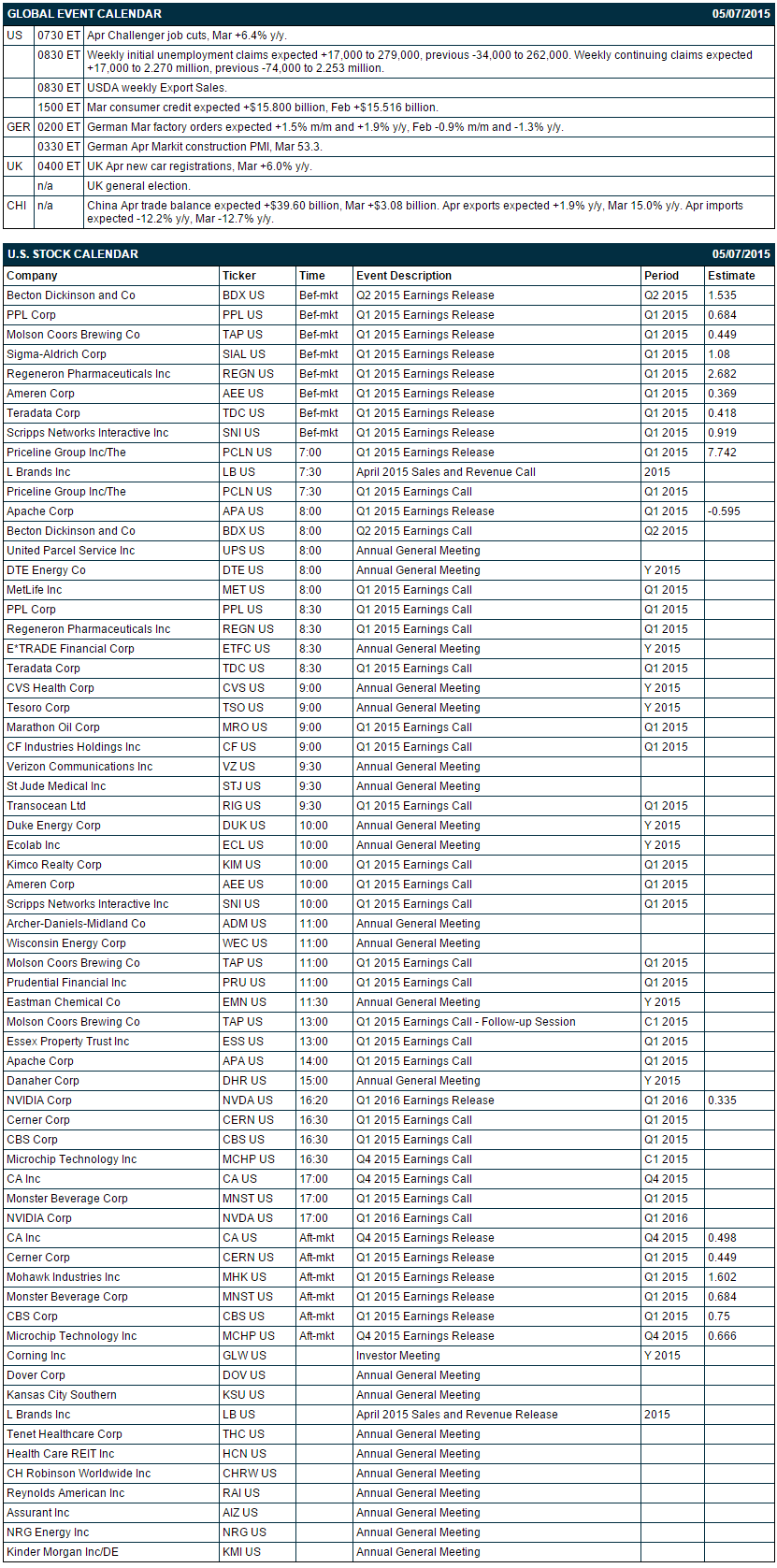

Key U.S. reports today include: (1) Apr Challenger job cuts (Mar was +6.4% y/y), (2) weekly initial unemployment claims (expected +16,000 to 278,000 after last week's -34,000 to 262,000) and continuing claims (expected +17,000 to 2.270 million after last week's -74,000 to 2.253 million), and (3) Mar consumer credit (expected +$15.800 billion after Feb's +$15.516 billion).

There are 17 of the S&P 500 companies that report earnings today with notable reports including: Priceline (consensus $7.74), NVIDIA (0.34), CA (0.50), Monster Beverage (0.68), CBS (0.75), Molson Coors Brewing (0.68).

U.S. IPO's scheduled to price today include: International Market Centers (IMC), Bojangles Inc (BOJA), Anterios (ANTE), NephroGenex (NRX), Hemishere Media Group (HMTV), Aldeyra Therapeutics (ALDX).

Equity conferences during the remainder of this week include: Baird Growth Stock Conference on Tue-Thu, Deutsche Bank Health Care Conference on Wed-Thu, ICI General Membership Meeting on Wed-Thu, Citi Car of the Future Conference on Thu, Mitsubishi UFJ Securities Oil & Gas Conference on Thu, and RBC Capital Markets Mobile & Cloud Networking Investor Day on Thu.

OVERNIGHT U.S. STOCK MOVERS

Sunoco (SXL -0.85%) reported a Q1 EPS loss with items of -10 cents, much weaker than consensus of 40 cents.

Children's Place (PLCE +7.78%) was upgraded to 'Neutral' from 'Sell' at Goldman Sachs.

Energy Transfer Equity (ETE -1.90%) reported Q1 EPS of 52 cents, well below consensus of 70 cents.

General Cable (BGC -0.92%) reported Q1 adjusted EPS of 35 cents, much better than consensus for a -13 cent loss.

Babcock & Wilcox (BWC +0.44%) reported Q1 adjusted EPS of 47 cents, higher than consensus of 43 cents.

Transocean (RIG +0.05%) reported Q1 adjusted EPS of $1.10, well above consensus of 60 cents.

Chesapeake Energy (CHK -7.19%) was downgraded to 'Neutral' from 'Buy' at SunTrust.

Pioneer Natural Resources (PXD -1.93%) was upgraded to 'Buy' from 'Neutral' at SunTrust with a price target of $190.

Tesla (TSLA -1.08%) rose nearly 2% in pre-market trading after it reported a Q1 EPS loss of -36 cents, a smaller loss than consensus of-50 cents.

Activision Blizzard (ATVI +2.16%) reported Q1 EPS of 16 cents, more than double consensus of 7 cents.

Prudential (PRU +0.36%) reported Q1 adjusted EPS of $2.79, well above consensus of $2.38.

MetLife (MET -0.63%) reported Q1 operating EPS of $1.44, above consensus of $1.41, but Q1 operating revenue of $17.03 billion was less than consensus of $17.53 billion.

Whole Foods Market (WFM +0.40%) slid 12% in after-hours trading after it reported Q2 EPS of 44 cents, higher than consensus of 43 cents, although Q2 revenue of $3.65 billion was below consensus of $3.70 billion.

21st Century Fox (FOXA -0.71%) reported Q3 EPS of 47 cents, above consensus of 39 cents.

Keurig Green Mountain (GMCR -1.75%) fell 12% in after-hours trading after it reported Q2 EPS of $1.03, below consensus of $1.05.

MARKET COMMENTS

June E-mini S&Ps (ESM15 -0.23%) this morning are down -11.25 points (-0.54%) at a new 1-month low. Wednesday's closes: S&P 500 -0.45%, Dow Jones -0.48%, Nasdaq -0.67%. The S&P 500 on Wednesday sold off to a 1-month low on the weaker than expected +169,000 increase in the ADP employment report and Fed Chair Yellen's comment that stock market valuations are "quite high" and could be a potential source of financial instability.

Jun 10-year T-notes (ZNM15 +0.11%) this morning are down -5.5 ticks to a new 1-3/4 month low. Wednesday's closes: TYM5 -10.50, FVM5 -4.50. Jun T-notes on Wednesday fell to a 1-3/4 month low on carry-over weakness from the plunge in German bund prices to a 4-month low and on Fed Chair Yellen's comment that long-term interest rates are low and could jump when they Fed begins to raise interest rates.

The dollar index (DXY00 +0.10%) this morning is up +0.019 (+0.02%). EUR/USD (^EURUSD) is down -0.0017 (-0.15%). USD/JPY (^USDJPY) is down-0.33 (-0.28%). Wednesday's closes: Dollar Index -0.989 (-1.04%), EUR/USD +0.0162 (+1.45%), USD/JPY -0.388 (-0.32%). The dollar index on Wednesday fell sharply to a 2-1/2 month low on the weaker-than-expected Apr ADP employment report, which may delay a Fed rate hike. Meanwhile, EUR/USD climbed to a 2-1/4 month high after the Eurozone Apr Markit composite PMI was revised higher by +0.4 to 53.9.

Jun WTI crude oil (CLM15 +0.13%) this morning is down -2 cents (-0.03%) and Jun gasoline (RBM15 -0.27%) is down -0.0079 (-0.39%). Wednesday's closes: CLM5 +0.53 (+0.88%), RBM5 -0.0380 (-1.84%). Jun crude oil and gasoline prices on Wednesday settled mixed with Jun crude at a 4-3/4 month high. Crude oil prices were boosted by the unexpected -3.88 million bbl decline in EIA crude inventories, the first decline in 17 weeks. In addition, U.S. crude oil production fell by -4,000 bpd, which was the third decline in the past four weeks. Gasoline closed lower after news that U.S. fuel consumption fell to an 11-month low of 18.196 million bpd.

Comments

Log in or sign up to join the conversation.