OVERNIGHT MARKETS AND NEWS

Dec E-mini S&Ps (ESZ17 -0.42%) this morning are down -0.45% after the U.S. Senate suspended voting on the tax bill until today after a compromise to win a majority collapsed. Also, the U.S. faces a partial government shutdown next Friday if Congress can't agree on a spending bill by then. European stocks are down -0.86% at a 2-week low led by a slump in technology stocks. Asian stocks settled mixed: Japan +0.41%, Hong Kong -0.35%, China +0.01%, Taiwan +0.38%, Australia +0.33%, Singapore +0.47%, South Korea -0.14%, India -0.95%. The Shanghai Composite closed little changed after a gauge of Chinese manufacturing activity last month slipped to a 5-month low. Japan's Nikkei Stock Index climbed to a 3-week high on signs of strength in the Japanese economy after Japan Q3 capital spending rose more than expected and after the Oct job-to-applicant ratio rose to a 43-4/4 year high.

The dollar index (DXY00 -0.02%) is down -0.05%. EUR/USD (^EURUSD) is down -0.07%. USD/JPY (^USDJPY) is down -0.10%.

Mar 10-year T-note prices (ZNH18 +0.23%) are up +10 ticks as the decline in stocks boosts safe-haven demand for T-notes.

The Eurozone Nov Markit manufacturing PMI was revised upward to a 17-1/2 year high of 60.1 from 60.0.

The UK Nov Markit manufacturing PMI rose +1.6 to a 3-3/4 year high of 58.2, stronger than expectations of +0.2 to 56.5.

The China Nov Caixin (flash) manufacturing PMI fell -0.2 to a 5-month low of 50.8, weaker than expectations of -0.1 to 50.9.

Japan Q3 capital spending rose +4.2% y/y, stronger than expectations of +3.2% y/y. Q3 capital spending ex-software rose +4.3% y/y, stronger than expectations of +3.1% y/y.

The Japan Oct jobless rate was unch at 2.8% right on expectations. The Oct job-to-applicant ratio rose +0.03 to a 43-3/4 year high of 1.55, stronger than expectations of unch at 1.52.

U.S. STOCK PREVIEW

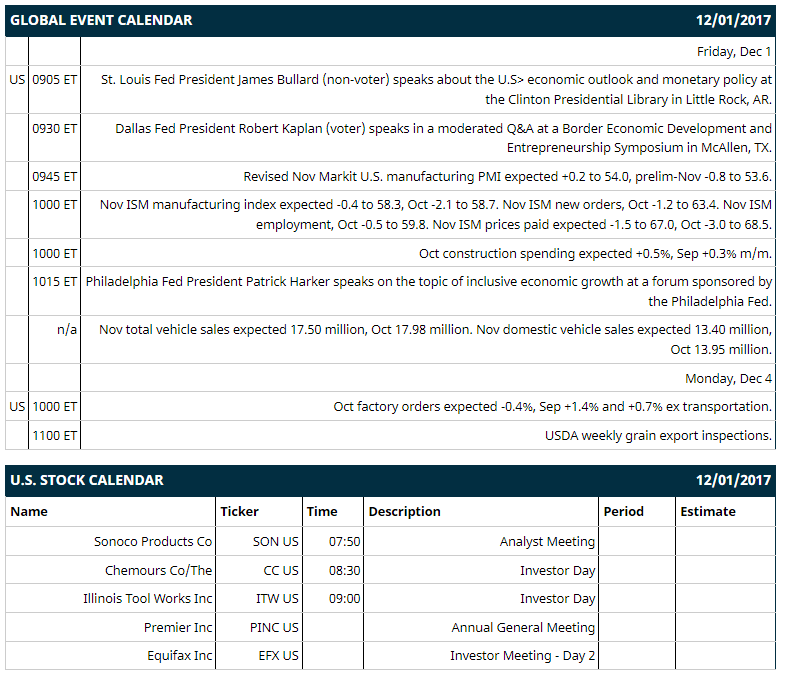

Key U.S. news today includes: (1) St. Louis Fed President James Bullard (non-voter) speaks about the U.S> economic outlook and monetary policy at the Clinton Presidential Library in Little Rock, AR, (2) Dallas Fed President Robert Kaplan (voter) speaks in a moderated Q&A at a Border Economic Development and Entrepreneurship Symposium in McAllen, TX, (3) revised Nov Markit U.S. manufacturing PMI (expected +0.2 to 54.0, prelim-Nov -0.8 to 53.6), (4) Nov ISM manufacturing index (expected -0.4 to 58.3, Oct -2.1 to 58.7), (5) Oct construction spending (expected +0.5%, Sep +0.3% m/m), (6) Philadelphia Fed President Patrick Harker speaks on the topic of inclusive economic growth at a forum sponsored by the Philadelphia Fed, (7) Nov total vehicle sales (expected 17.50 million, Oct 17.98 million).

Notable Russell 1000 earnings reports today include: none.

U.S. IPO's scheduled to price today: none.

Equity conferences this week: none.

OVERNIGHT U.S. STOCK MOVERS

Priceline Group (PCLN +0.30%) was downgraded to 'Hold' from 'Buy' at Argus Research.

Cummins (CMI +1.75%) was downgraded to 'Neutral' from 'Buy' at Goldman Sachs.

Ulta Beauty (ULTA -0.62%) dropped nearly 6% in after-hours trading after it said it sees Q4 EPS of $2.73 to $2.78, well below consensus of $2.84.

Ambarella (AMBA -0.35%) rallied 6% in after-hours trading after it reported Q3 adjusted EPS of 75 cents, higher than consensus of 67 cents, and said it sees Q4 adjusted gross margin of 62% to 63.5%, better than consensus of 61.7%.

Five Below (FIVE +0.91%) gained 2% in after-hours trading after it reported Q3 EPS of 18 cents, above consensus of 13 cents, and said it sees full-year EPS of $1.72 to $1.79, better than consensus of $1.67.

AGCO Corp. (AGCO -0.17%) was upgraded to 'Buy' from 'Neutral' at Goldman Sachs with a price target of $90.

VMware (VMW +0.58%) rose 2% in after-hours trading after it reported Q3 adjusted EPS of $1.34, better than consensus of $1.27, and then raised guidance on full-year adjusted EPS to $5.13 from a prior view of $5.06, above consensus of $5.07.

E*TRADE Financial (ETFC +0.75%) was initiated with a recommendation of 'Outperform' at Credit Suisse with a 12-month target price of $56.

Charles Schwab (SCHW +0.76%) was initiated with a recommendation of 'Outperform' at Credit Suisse with a 12-month target price of $55.

Zumiez (ZUMZ +4.56%) fell 5% in after-hours trading after it reported Q3 gross margin of 33.9%, below consensus of 34.6%.

Nutanix (NTNX +0.86%) climbed over 2% in after-hours trading after it reported Q1 revenue of $275.6 million, above consensus of $266.9 million, and said it expected Q2 revenue of $280 million to $285 million, the mid-point above consensus of $282 million.

Yext (YEXT +1.92%) dropped 5% in after-hours trading after it said it sees Q4 revenue of $47.3 million to $48.3 million, weaker than consensus of $48.5 million.

MARKET COMMENTS

Dec S&P 500 E-mini stock futures (ESZ17 -0.42%) this morning are down -12.00 points (-0.45%). Thursday's closes: S&P 500 +0.82%, Dow Jones +1.39%, Nasdaq +0.86%. The S&P 500 on Thursday rose to a new record high and closed higher on increased optimism that Congress will be able to pass a U.S. tax reform plan and on the +0.4% increase in U.S. Oct personal income, stronger than expectations of +0.3%.

Mar 10-year T-note prices (ZNH18 +0.23%) this morning are up +10 ticks. Thursday's closes: TYH8 -13.50, FVH8 -9.00. Mar T-notes on Thursday fell to a 1-month low and closed lower on the rally in the S&P 500 to a new record high and on the stronger-than-expected +0.4% increase in U.S. Oct personal income, which bolsters the case for additional Fed rate hikes.

The dollar index (DXY00 -0.02%) this morning is down -0.047 (-0.05%). EUR/USD (^EURUSD) is own -0.0008 (-0.07%) and USD/JPY (^USDJPY) is down -0.11 (-0.10%). Thursday's closes: Dollar Index -0.117 (-0.13%), EUR/USD +0.0007 (+0.06%), USD/JPY +0.45 (+0.40%). The dollar index on Thursday closed lower on strength in EUR/USD after ECB Executive Board member Praet said the breadth of economic expansion in the Eurozone is "notable." There was also strength in GBP/USD which rose to a 2-month high on reduced Brexit concerns after the EU said it will offer a 2-year Brexit transition deal to the UK as soon as January.

Jan crude oil (CLF18 +0.91%) this morning is up +40 cents (+0.70%) and Jan gasoline (RBF18 +1.06%)is +0.0111 (+0.64%). Thursday's closes: Jan WTI crude +0.10 (+0.17%), Jan gasoline -0.0039 (-0.22%). Jan crude oil and gasoline on Thursday settled mixed. Crude oil prices were boosted by a weaker dollar and by the action by OPEC and Russia to extend their crude production cuts until the end of 2018. Gasoline closed lower after the crack spread fell to a 1-3/4 month low, which reduces incentive for refiners to purchase crude to refine into gasoline.

Metals prices this morning are mixed with Feb gold (GCG18 +0.16%) +2.4 (+0.19%), Mar silver (SIH18 -0.24%) -0.059 (-0.36%) and Mar copper (HGH18 +0.41%) +0.011 (+0.36%). Thursday's closes: Feb gold -9.5 (-0.74%), Mar silver -0.086 (-0.51%), Mar copper -0.0045 (-0.15%). Metals on Thursday settled mixed with Feb gold at a 1-week low and Mar silver at a 3-1/2 month low. Metals prices were undercut by the rally in the S&P 500 to a new record high, which reduces safe-haven demand for precious metals, and by the stronger-than-expected U.S. economic data on weekly jobless claims and Oct personal income, which bolsters the case for additional Fed rate hikes. Copper closed higher on reduced Chinese copper demand concerns after the China Nov manufacturing PMI unexpectedly rose +0.2 to 51.8.

(Click on image to enlarge)

Comments

Log in or sign up to join the conversation.