OVERNIGHT MARKETS AND NEWS

March E-mini S&Ps (ESH16 -0.63%) are down -0.75% and European stocks are down -1.40% on global growth concerns. Crude oil (CLH16 -3.10%) is down -3.45%, which is undercutting energy producers that are leading the overall market lower with Chevron and Schlumberger down over 1% in pre-market trading. Losses in European stocks were limited after the Eurozone Dec unemployment rate unexpectedly fell to a 4-1/3 year low of 10.4%. Asian stocks settled mostly lower: Japan -0.64%, Hong Kong -0.76%, China +2.26%, Taiwan -0.32%, Australia -1.00%, Singapore -0.89%, South Korea-1.10%, India -1.15%. China's Shanghai Composite closed higher after the PBOC injected 100 billion yuan ($15 billion) into the banking system using reverse repurchase agreements to provide liquidity ahead of the Chinese lunar new year holidays next week.

The dollar index (DXY00 -0.11%) is down -0.05%. EUR/USD (^EURUSD) is up +0.30%. USD/JPY (^USDJPY) is down -0.15%.

Mar T-note prices (ZNH16 +0.21%) are up +9.5 ticks.

The PBOC said it will allow banks to cut the minimum required mortgage down payment to 20% from 25% for first-home purchases to the lowest ever in an attempt to boost China's property market. Also, the minimum down payment for second-home purchases was cut to 30% from 40%.

The Eurozone Dec unemployment rate unexpectedly fell -0.1 to 10.4%, better than expectations of no change at 10.5% and the lowest in 4-1/3 years.

Eurozone Dec PPI fell -0.8% m/m and -3.0% y/y, a faster pace of decline than expectations of -0.6% m/m and -2.8% y/y.

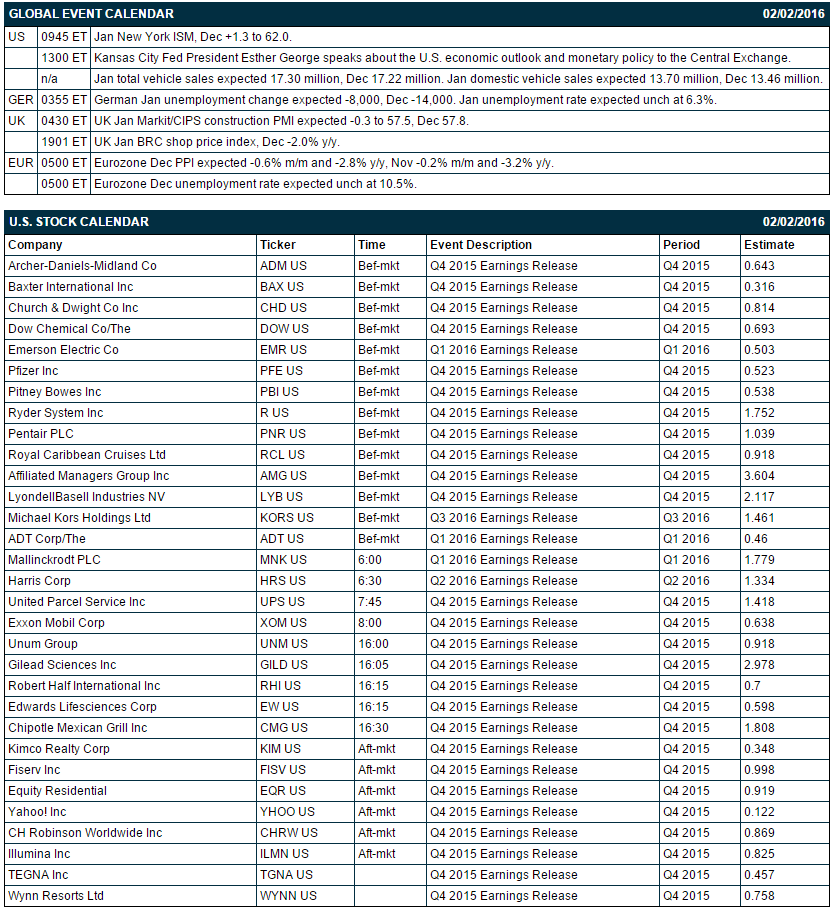

U.S. STOCK PREVIEW

Key U.S. news today includes: (1) Jan New York ISM (Dec +1.3 to 62.0), (2) Kansas City Fed President Esther George's speech about the U.S. economic outlook and monetary policy to the Central Exchange, and (3) Jan total vehicle sales (expected 17.30 million, Dec 17.22 million) and Jan domestic vehicle sales (expected 13.70 million, Dec 13.46 million).

There are 31 of the S&P 500 companies that report earnings today with notable reports including: Exxon (0.64), UPS (1.42), Pfizer (0.52), Baxter (0.32), ADM (0.64), Chipotle (1.81), Yahoo (0.12).

U.S. IPO's scheduled to price today: BeiGene (BGNE), Nordic Realty Trust (NORT), Editas Medicine (EDIT).

Equity conferences this week include: Cowen and Company Aerospace/Defense Conference & Transport Forum on Wed-Thu

OVERNIGHT U.S. STOCK MOVERS

Alphabet (GOOGL +1.24%) is up overr 3% in pre-market trading after it reported Q4 adjusted EPS of $8.67, well above consensus of $8.09, as Q4 paid clicks climbed +31% y/y, higher than consensus of +22.4% y/y.

Down Chemical (DOW +1.38%) reported Q4 EPS of 91 cents, higher than consensus of 69 cents.

UGI Corp. (UGI +0.32%) reported Q1 adjusted EPS of 64 cents, below consensus of 70 cents.

Aflac (AFL -2.50%) rose over 1% in after-hours trading after it reported Q4 operating EPS of $1.56, above consensus of $1.48.

Rent-A-Center (RCII -2.50%) slumped over 10% in after-hours trading after it reported Q3 revenue of $793.8 million, less than consensus of $874.8 million, and said it sees 2016 core U.S. revenue down -4% to -6%, weaker than consensus of +1%.

Flowserve (FLS -0.70%) lowered guidance on fiscal 2016 adjusted EPS to $2.40-$2.75, weaker than consensus of $2.95.

Mattel (MAT -3.01%) gained over 5% in after-hours trading after it reported Q4 adjusted EPS all items of 63 cents, above consensus of 61 cents.

Leggett & Platt (LEG +0.17%) slid almost 4% in after-hours trading after it said it sees 2016 sales of $2.9 billion-$4.1 billion, below consensus of $4.17 billion.

Anadarko Petroleum (APC -2.15%) climbed over 4% in after-hours trading after it reported a Q4 adjusted EPS loss of -57 cents, a smaller loss than consensus of -$1.10.

Plantronics (PLT -0.16%) was downgraded to 'Underperform' from 'Outperform' at Raymond James.

Hain Celestial (HAIN +1.73%) reported Q2 adjusted EPS of 57 cents, higher than consensus of 54 cents.

PVH Corp. (PVH -0.29%) rose over 6% in after-hours trading after it raised guidance on 2016 adjusted EPS to above $7.00 from a December estimate of $6.90-$7.00, above consensus of $6.96.

Rayonier Advanced Materials (RYAM +2.43%) fell over 7% in after-hours trading after it reported Q4 revenue of $242 million, below consensus of $245.8 million.

MARKET COMMENTS

Mar E-mini S&Ps (ESH16 -0.63%) this morning are down -14.50 points (-0.75%). Monday's closes: S&P 500 -0.04%, Dow Jones -0.10%, Nasdaq +0.17%. The S&P 500 on Monday closed slightly lower on negative carryover from the -1.78% drop in China's Shanghai Composite on growth concerns after China's Jan manufacturing PMI fell -0.3 to 49.4, weaker than expectations of -0.1 to 49.6 and the steepest pace of contraction in 3-1/3 years. Stocks were also undercut by the +0.2 point increase in the U.S. Jan ISM manufacturing index, which was weaker than expectations of +0.4 to 48.4. On the supportive side, Fed Vice Fed Chair Fischer said that market turmoil could affect the Fed's next policy move, which reduces the outlook for the Fed to raise interest rates at the next FOMC meeting in March.

Mar 10-year T-notes (ZNH16 +0.21%) this morning are up +9.5 ticks. Monday's closes: TYH6 -13.00, FVH6 -8.50. Mar T-notes on Monday retreated from a contract high and closed lower on profit-taking after the rally of more than 4 points in Mar T-notes in the past month. T-notes were also undercut by signs of strength within the weaker-than-expected Jan ISM report after the Jan new orders sub-index rose +2.7 a 5-month high of 51.5.

The dollar index (DXY00 -0.11%) this morning is down -0.048 (-0.05%). EUR/USD (^EURUSD) is up +0.0033 (+0.30%). USD/JPY (^USDJPY) is down-0.18 (-0.15%). Monday's closes: Dollar Index -0.597 (-0.60%), EUR/USD +0.0057 (+0.53%), USD/JPY -0.15 (-0.12%). The dollar index on Monday closed lower on global economic concerns that may delay additional Fed interest rate increases after China's Jan manufacturing PMI contracted for an eleventh month and the U.S. Jan ISM manufacturing index contracted for a fourth month. The dollar index was also undercut by strength in EUR/USD after German Jan Markit/BME manufacturing PMI was revised upward to 52.3 from 52.1.

Mar crude oil (CLH16 -3.10%) this morning is down -$1.09 a barrel (-3.45%) and Mar gasoline (RBH16 -4.59%) is down -0.0481 (-4.44%). Monday's closes: CLH6 -2.30 (-6.84%), RBH6 -0.0508 (-4.49%). Mar crude oil and gasoline on Monday closed sharply lower on global economic concerns after China's Jan manufacturing PMI contracted at the steepest pace in 3-1/3 years and the U.S. Jan ISM manufacturing contracted for a fourth month. Crude oil prices were also hurt by news of record OPEC crude output as Jan OPEC crude production rose +38,000 bpd to a record 33.113 million bpd.

Comments

Log in or sign up to join the conversation.