Thesis:

A smart value investor was an aggressive buyer of undervalued stocks in 2008 and 2009. Since Mr. Buffett was not aggressively buying stocks during the financial crisis, he laid the foundation for his subsequent mediocre investment returns.

His insistence of holding Billions of dollars of cash while the market was down substantially was a perplexing mistake for a seasoned value investor. His inability to seize values resulted in a lost decade for shareholders. The BNSF acquisition is examined and it's costly dilution to shareholders.

"Cash combined with courage in a time of crisis is priceless." - Warren Buffett

Patience, Discipline and Panic:

The hard part of being a value investor is avoiding overpriced stocks when everyone else is buying. It requires discipline. The huge reward for the patient investor is when prices are attractive, or in this case, extremely attractive, you have cash to take advantage of incredible opportunities.

Unfortunately, Mr. Buffett did not really take advantage of these incredible opportunities. In fact, the Burlington Northern purchase required selling other investments as well as diluting shares near decade low valuations. Not using cash on hand to purchase stocks or buyback Berkshire stock was a missed opportunity for shareholders.

Be greedy when others are fearful and fearful when others are greedy. Warren Buffett

Berkshire a net seller of stocks in 2009:

We made some sales early in 2009 to raise cash for our Dow and Swiss Re purchases and late in the year made other sales in anticipation of our BNSF purchase - Warren Buffett Berkshire Annual Letter

I can't explain why Mr. Buffett wasn't greedy for the great opportunities in the stock market during this period. Perhaps he felt that BNSF, Goldman, Sachs and General Electric would perform better over time. I believe it was a huge mistake, especially for an investor whose businesses generate Billions of dollars that need to be invested.

SPY 10 Year Price Returns (Daily) data by YCharts

The benefit of being a value investor is that you can profit handsomely from other investors who purchased overpriced shares at the top and then are panicking at the bottom.

"Whatever money you may need for the next five years, please take it out of the stock market right now, this week. I do not believe that you should risk those assets in the stock market right now."

Jim Cramer, CNBC October 8, 2008

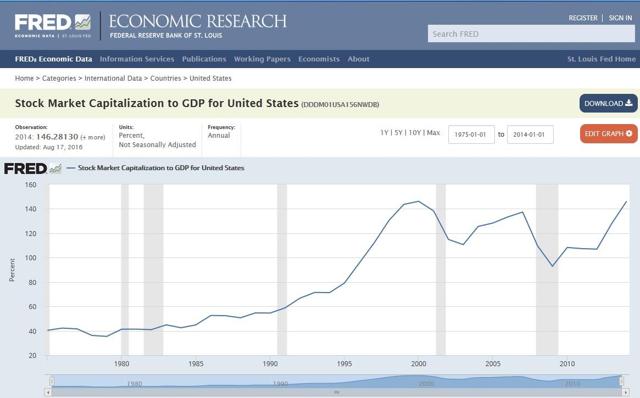

Today's market:

Berkshire Hathaway: So Much Cash, Such An Expensive Market (BRK-A)

Over the last decade, Mr. Buffett has complained that he has had trouble putting cash to work and cited high valuations as the problem. As we see, valuations are much more expensive. It is a legitimate question as to why he wasn't able to purchase more when prices were lower and more attractive.

"Wait for a fat pitch and then swing for the fences." -Warren Buffett

Value:

In 2009, Berkshire threw off $8-$10B in cash and even more in the years to come.

- Why not invest it.

- Why not issue bonds in anticipation of future cash flows, to purchase shares at attractive prices?

- Why not buyback Berkshire stock instead of diluting it?

We have- we have eight or $10 billion to invest every year. -Warren Buffett, 2009

Liquidity: I see no logical reason based on cashflow, interest expense, or liquidity that would have prevented Buffett from investing much more during the downturn in either undervalued companies or in a Berkshire buyback.

Returns: In my opinion, returns for Berkshire Hathaway (BRK-B) shareholders could have been much higher with less risk over the past decade. As we will see, the large Burlington (BNSF) acquisition proved costly in many ways.

Liquidity:

We entered 2008 with $44.3 billion of cash-equivalents, and we have since retained operating earnings of $17 billion. Nevertheless, at year end 2009, our cash was down to $30.6 billion (with $8 billion earmarked for the BNSF acquisition).Berkshire Hathaway Annual Report, 2009

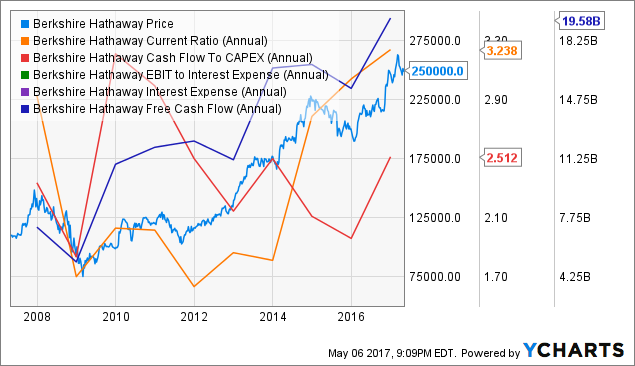

Buyback:

As we see, Berkshire stock declined substantially during the financial crisis. The book value was cut in half. One of the best investments I made during the 2008 Crisis was buying Berkshire Stock. Why wasn't Warren Buffett doing the same?

Today, we see companies offering bonds and doing buybacks with prices near all-time highs. It's a shame that Mr. Buffett held to his large cash position and wasn't able to deploy that capital in ways that would enhance future returns.

"Cash combined with courage in a time of crisis is priceless." - Warren Buffett

Access to Cash:

If one can have the patience to buy stocks during a panic like 2008, then one doesn't need to be an exceptional stock picker to receive incredible returns for years to come.

Mr. Buffett had the most valuable commodity during the crash: he had cash and access to much more to invest in undervalued stocks or companies. Or a stock buyback.

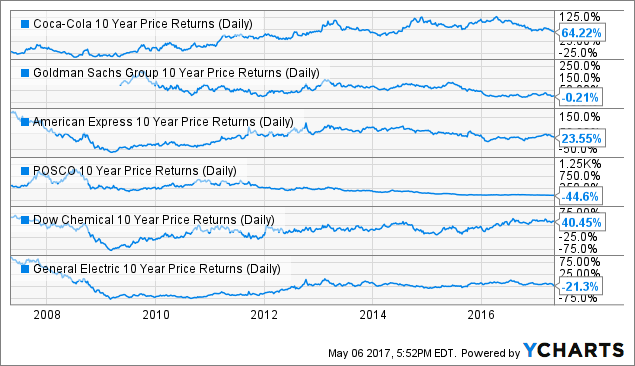

Buffett's Favorite Stocks/ Average returns:

Were any of the investments from 2008-2009 exceptional? General Electric (GE) and Goldman, Sachs (GS) have underperformed the overall market by a large margin. Even accounting for his preferred dividends, the returns on these investments are hardly impressive.

Risk: In fact, he took enormous risks investing in these distressed companies. Goldman, Sachs had a 22:1 Leverage ratio at the time of his investment.

KO 10 Year Price Returns (Daily) data by YCharts

Apple:

Apple had a p/e of 12-13 back in 2009. So, if Mr. Buffett had invested, the returns for shareholders would have been exceptional. His recent Apple (AAPL) investment was at a p/e of 16, with Tim Cook as the CEO, when he could have purchased Apple shares at a p/e of 11-13 with Steve Jobs as the CEO in 2009. The risk/ reward seemed much more attractive in 2009.

Hindsight: Yes, hindsight is 20/20. But, the point is that there were hundreds or thousands of great opportunities in 2008-2009. And if Mr. Buffett thinks Apple is undervalued today, then it seems fair to ask why wasn't he a buyer when it was much more attractively priced.

AAPL 10 Year Total Returns (Daily) data by YCharts

AAPL 10 Year Total Returns (Daily) data by YCharts

Under-performance:

Mr. Buffett still has a terrific tracks record. However, his job is to allocate capital. Since stocks were so attractively priced after the financial crisis, one can wonder why he wasn't able to better capitalize on these opportunities.

In a first, Buffett gets beat by the S&P 500 over five years.

these results capped a five-year period, year-end 2008 to year-end 2013, in which the S&P 500 beat Berkshire's gain in book value per share -- the first such period in Berkshire's history. For the five years, the S&P index jumped 128%. Berkshire's book value per share rose by only 91%.

Mr. Buffett was not able to invest more during the financial crisis due to his large purchase of BNSF. So, let's examine the performance of this business and his other purchases.

BNSF Investment:

Mr. Buffett's comments seem to indicate he's not even convinced it will be a great investment.

In an interview with Charlie Rose Buffett says a "reasonable return is good enough" and acknowledges that BNSF was "not a bargain" at $26 billion.

Reasonable return is good enough, Charlie. I mean, 50 years ago, I was looking for spectacular returns, but I can't- I can't get them. We have- we have eight or $10 billion to invest every year. -Warren Buffett

You're spending a lot of money to repair track, add rolling stock, whatever it may be. So it's capital-intensive, and it is regulated, and it will continue to be regulated, and it will continue to be capital-intensive.

And unfortunately, Buffett diluted shareholders near the market bottom in 2009 to pay for this acquisition.

BUFFETT: I don't like to use stock, but on this one, because of the size and because they wanted a tax-free option for shareholders, we're doing it 40 percent stock and 60 percent cash.

As we see, an unfortunate time to dilute shareholders.

Radical Shift in Berkshire:

What the Berkshire shareholder wants is a business that throws off cash (like the insurance business) that allows Mr. Buffett to invest the float at a high rate of return.

BNSF's contribution to Berkshire's earnings has fluctuated between 18 percent to 29 percent since it was brought into the fold.

Capital Intensive Business:

"At BNSF we will spend a lot of money to have the best railroad possible but we're not going to be buying other businesses," Buffett, 83, said, however.

Already, the company has spent $27.2 billion on capital expenditures since the beginning of 2010. (Bloomberg)

BNSF is a capital intensive business that requires cash for capital expenses to operate.

The investor can only imagine the opportunity cost of $27B in investments that could have been made since 2009.

Returns:

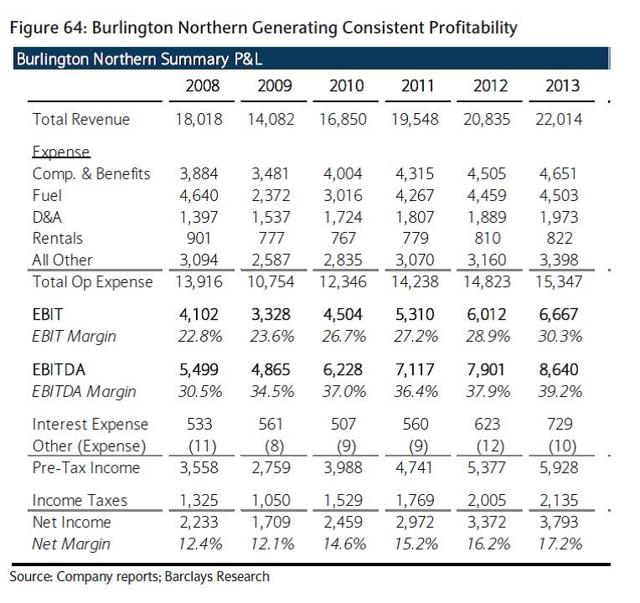

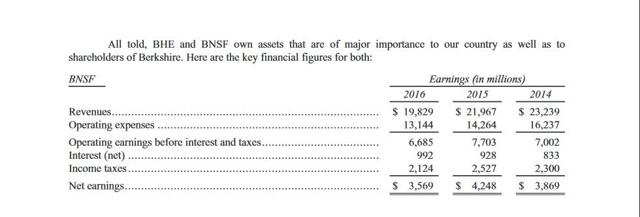

The railroad business had a nice recovery from the financial crisis. However, the intelligent investor can easily ask, what business hasn't had a nice recovery since then? Returns of all financial assets and the market averages (MDY) have done incredibly well. The reader can make their own judgment on the performance of BNSF.

(Click on image to enlarge)

(Berkshire Annual Report)

In his annual letter to shareholders, the Berkshire Hathaway CEO said that the story in 2014 for BNSF, the giant railroad company that Buffet bought in 2009, was "not good."

- "The railroad disappointed many of its customers," writes Buffett.

- Buffett called attention to BNSF's plan to spend $6 billion on improvements in 2015

BNSF: 2017: Still struggling

Declining Coal Use Hurts BNSF Railroad

- Mr. Buffett's letter notes that the BNSF railroad's earnings fell 16% in 2016 to $3.6 billion but doesn't say why.

- BNSF is one of Berkshire's biggest units, and this drop had a notable impact on the company's full-year results.

- "In 2016, we experienced declining demand, especially in our coal and crude oil categories.

- Coal had the largest decline

- BNSF's freight revenues from coal fell 27% in 2016.

- But freight revenues fell in other segments too, including consumer products and industrial products.

The financial media praised this investment in Goldman, Sachs Sachs, Buffett. Even accounting for his preferred dividends, the risk/ reward for the investment is unimpressive. Intelligent investors realize that in a severe recession or depression, Mr. Buffett's investment could have been diluted or wiped out.

Risk: In 2009, Goldman, Sachs had an incredible amount of leverage at 22:1. And in spite of its prestigious name, any company can go bankrupt with that much leverage, especially in a financial crisis. In my opinion, the risk/ reward of this investment was poor. Making money is not the only consideration for an investor.

they will submit themselves to greater regulation, including limits on the amount of debt they can take on. When it collapsed, Lehman had about a 30:1 debt-to-equity ratio, meaning it had borrowed $30 for every dollar in capital it held. Morgan Stanley currently has a debt-to-equity ratio of 30:1, while Goldman Sachs has one of about 22:1.

(MS) GS 10 Year Total Returns (Daily) data by YCharts

Conclusion:

Mr. Buffett missed incredible opportunities during the financial crisis. As a value investor with ample liquidity, Mr. Buffett had the opportunity to create exceptional returns for his shareholders. This missed opportunity still weighs on his returns. Holding excess cash was a mistake. And his inability to buy back shares in Berkshire Hathaway at a big discount was another missed opportunity. Unfortunately, his inability to seize values a decade ago has resulted in a lost decade for his shareholders.

Comments

Log in or sign up to join the conversation.