Micron's (NASDAQ:MU) main driver is memory pricing, and there's been good news just out that pricing is turning up and supply likely will not meet demand. That's a good set up for this tech cyclical that's so dependent on pricing. I wanted to run through some of the updates on 2020 supply, demand and pricing.

First Let's Discuss Pricing

Earnings drive stock prices and my model for Micron is so dependent on pricing.

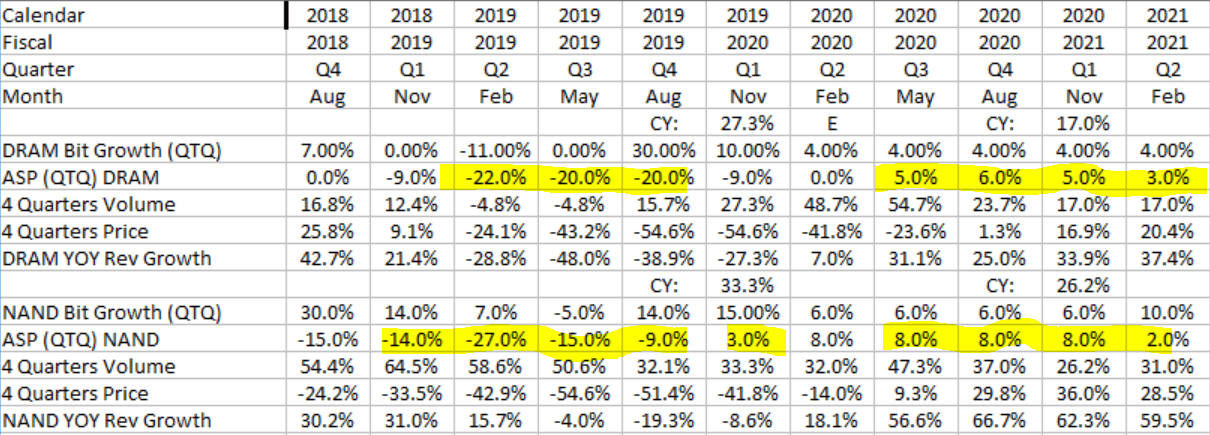

Source: Elazar Advisors reports sourced from Micron Earnings Reports

You see above the pricing has been down for DRAM and just turned up for NAND in the November quarter. (see our full model: Paywall).

Along with that earnings kept dropping.

|

Pricing falling forced EPS lower. Now EPS should start moving up with pricing moving up.

The Street expects down EPS for Micron from the November quarter to the February quarter but I think EPS should do much better than that.

This is the most important driver to the income statement because it drives revenues, margins and so earnings. Earnings drive stock prices so this lift in pricing should help Micron show big upside for earnings for the quarters.

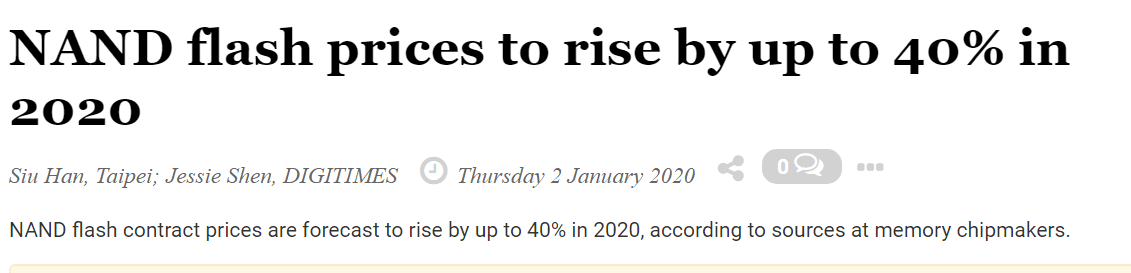

This was out today.

I incorporated the 40% rise of NAND into our Micron earnings model.

67% of Micron revenues last quarter were DRAM while 33% NAND (Page 13).

This report below on NAND was updated from expecting pricing up 10% in Q1 to now expecting pricing up 10%-15% in Q1. So estimates are on the way up.

Here's some recent news on DRAM.

Graphics DRAM is one segment of the market but memory typically moves up in unison regardless of the end market. Memory is more of a commodity so overall industry pricing moves together.

You can see based on our quarterly pricing grid way above that a turn up in DRAM would be a first after dropping for multiple quarters.

Demand and pricing are moving up likely because of cloud capex growth rates moving back up and also 5G coming. The let up in the US-China trade war probably hasn't been felt yet but also should be a driver.

Industry Supply Shortfalls: Wow

This gets a wow from me...

You have pricing already starting to move up. Demand should improve from last year with the let up in trade tensions and 5G buildouts. And combined with that you may get a big double-digit shortage in DRAM and NAND supply after manufacturers have been shaving capacity.

Conclusion

This sets up a strong year for pricing. 2019 was the setup. But 2020 looks like the actualization of a strong pricing environment which should be amazing for Micron earnings and stock price.

I started following tech and memory back in the '90s. You can't ask for more for memory stocks than higher pricing.

Comments

Log in or sign up to join the conversation.