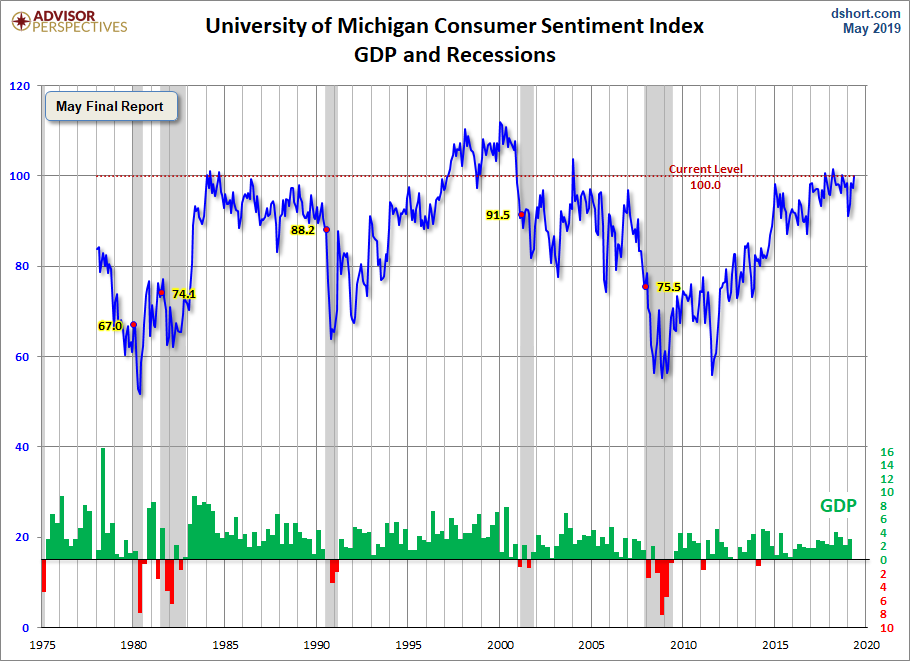

The May Final came in at 100.0, up 2.8 from the April Final reading. Investing.com had forecast 102.0.

Surveys of Consumers chief economist, Richard Curtin, makes the following comments:

Although consumer sentiment remained at very favorable levels, confidence significantly eroded in the last two weeks of May. The late-month decline was due to unfavorable references to tariffs, spontaneously mentioned by 35% of all consumers in the last two weeks of May, up from 16% in the first half of May and 15% in April and equal to the peak recorded last July in response to the initial imposition of tariffs. The year-ahead inflation expectations jumped to 2.9% in May up from last month’s 2.5%. Year-ahead inflation expectations among those who unfavorably mentioned tariffs was 0.5 percentage points higher than those who made no references to tariffs. Importantly, the gain in inflation expectations was recorded prior to the actual increases in consumer prices due to the most recent hike in tariffs. While higher inflation expectations modestly reduced real income expectations, the largest impact was on buying conditions for appliances and other large household durables, which fell to their lowest level in four years. The combination of higher inflation and a slower pace of spending provide conflicting signals for monetary policy. The divergence will further widen if, as is likely, the trade war escalates. Will the Fed risk higher inflation by lowering interest rates, or risk higher unemployment by raising interest rates? This delimma comes at a time when consumers have expressed the highest level of confidence since 2002 in the government’s ability to keep both inflation and unemployment at reasonably low levels (see the chart). Consumers now judge economic security more important than a faster pace of growth in their personal incomes or household wealth. [More...]

See the chart below for a long-term perspective on this widely watched indicator. Recessions and real GDP are included to help us evaluate the correlation between the Michigan Consumer Sentiment Index and the broader economy.

To put Friday's report into the larger historical context since its beginning in 1978, consumer sentiment is 16.0 percent above the average reading (arithmetic mean) and 17.4 percent above the geometric mean. The current index level is at the 90th percentile of the 497 monthly data points in this series.

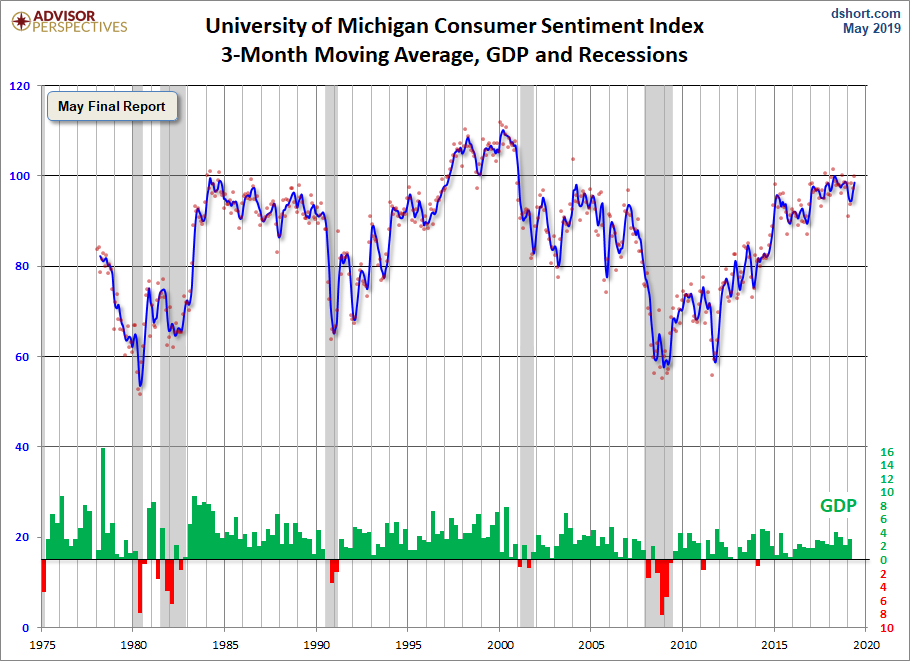

Note that this indicator is somewhat volatile, with a 3.0 point absolute average monthly change. The latest data point saw a 2.8 point increase from the previous month. For a visual sense of the volatility, here is a chart with the monthly data and a three-month moving average.

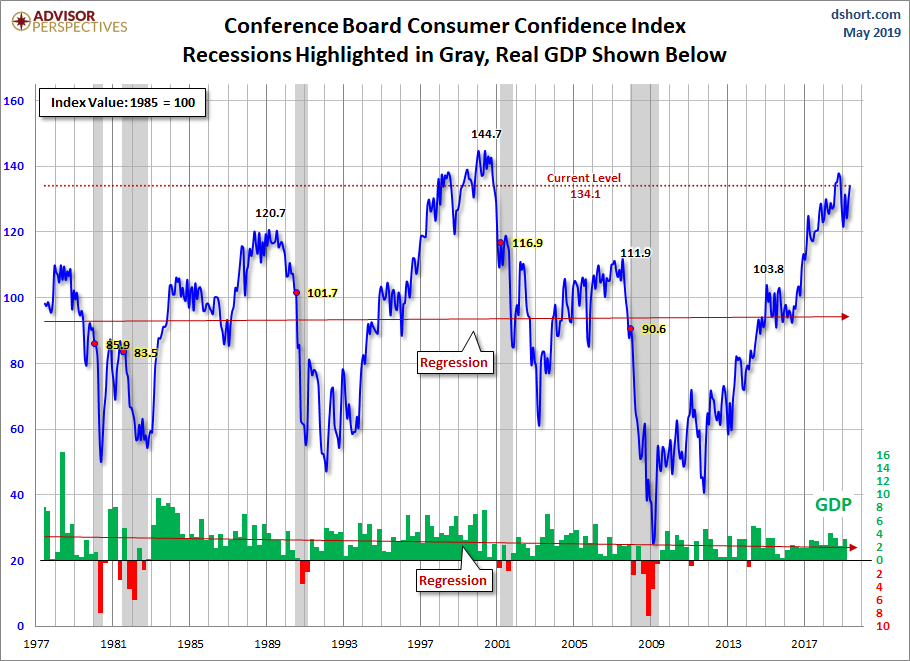

For the sake of comparison, here is a chart of the Conference Board's Consumer Confidence Index (monthly update here). The Conference Board Index is the more volatile of the two, but the broad pattern and general trends have been remarkably similar to the Michigan Index.

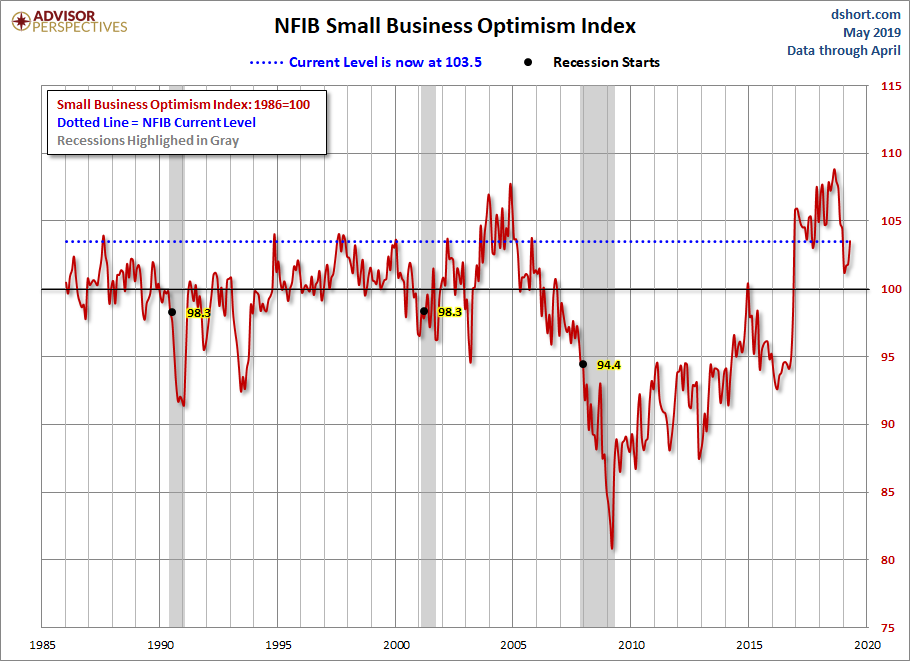

And finally, the prevailing mood of the Michigan survey is also similar to the mood of small business owners, as captured by the NFIB Business Optimism Index (monthly update here).

The general trend in the Michigan Sentiment Index since the Financial Crisis lows was one of slow improvement. The survey findings saw a jump in late 2016 with improvements that have recently begun to decline.

The next update to this report will be for the June preliminary data and will be published June 14th.

Comments

Log in or sign up to join the conversation.