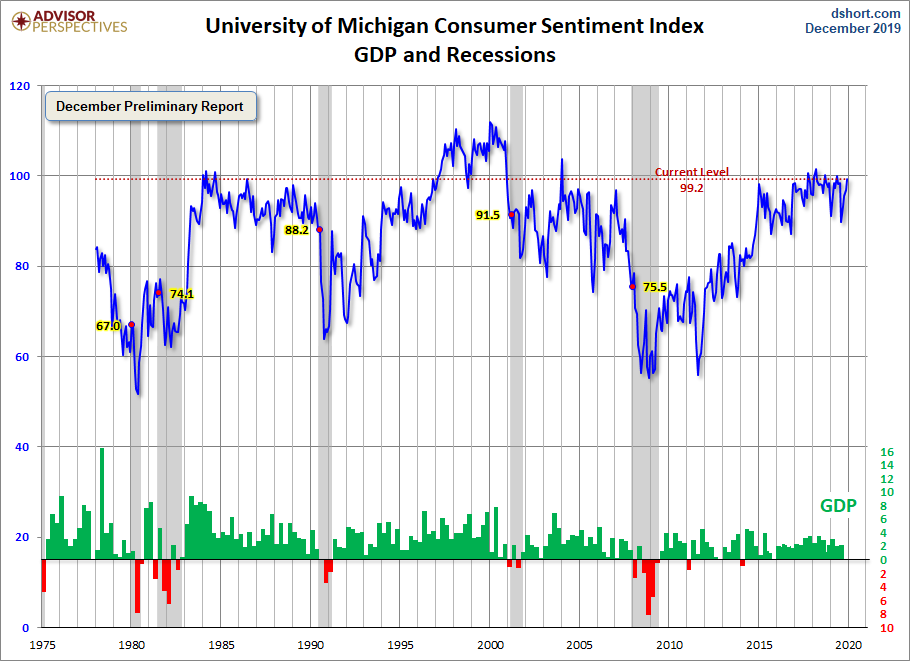

The December Preliminary came in at 99.2, up 2.4 from the November Final reading. Investing.com had forecast 97.0.

Surveys of Consumers chief economist, Richard Curtin, makes the following comments:

Consumer sentiment rose to the upper end of the favorable range it has traveled since the start of 2017. The Sentiment Index has averaged 97.0 in the past three years, the highest sustained level since the all-time record in the Clinton administration. Nearly all of the early December gain was among upper income households, who also reported near record gains in household wealth, largely due to increased stock prices. Indeed, among households with incomes in the top third of the distribution, their overall assessment of their current finances was the third highest in the past twenty years. These gains were aided by declining inflation expectations, with long term inflation expectations returning to an all-time low.

While impeachment has dominated the media, virtually no consumer spontaneously mentioned impeachment in response to any question in early December--just 1%. Nonetheless, the data indicate the strong impact of partisanship on economic expectations, which has widened in the past few months. Moreover, the gap has grown considerably in the past decade. The average gap between Democrats and Republicans was 18.7 points in the Obama administration and 41.6 points since Trump took office. Importantly, the views of Independents closely track the overall Sentiment Index, with a mean of 96.6 versus 97.0 for all consumers (see the chart). While the implications of the economic expectations of Democrats and Republicans are clearly exaggerated, the Independents, who represent the largest group and are less susceptible to maintaining partisan views, hold very favorable expectations, indicating the continuation of the expansion based on consumer spending. [More...]

See the chart below for a long-term perspective on this widely watched indicator. Recessions and real GDP are included to help us evaluate the correlation between the Michigan Consumer Sentiment Index and the broader economy.

To put this report into the larger historical context since its beginning in 1978, consumer sentiment is 14.9 percent above the average reading (arithmetic mean) and 16.3 percent above the geometric mean. The current index level is at the 89th percentile of the 504 monthly data points in this series.

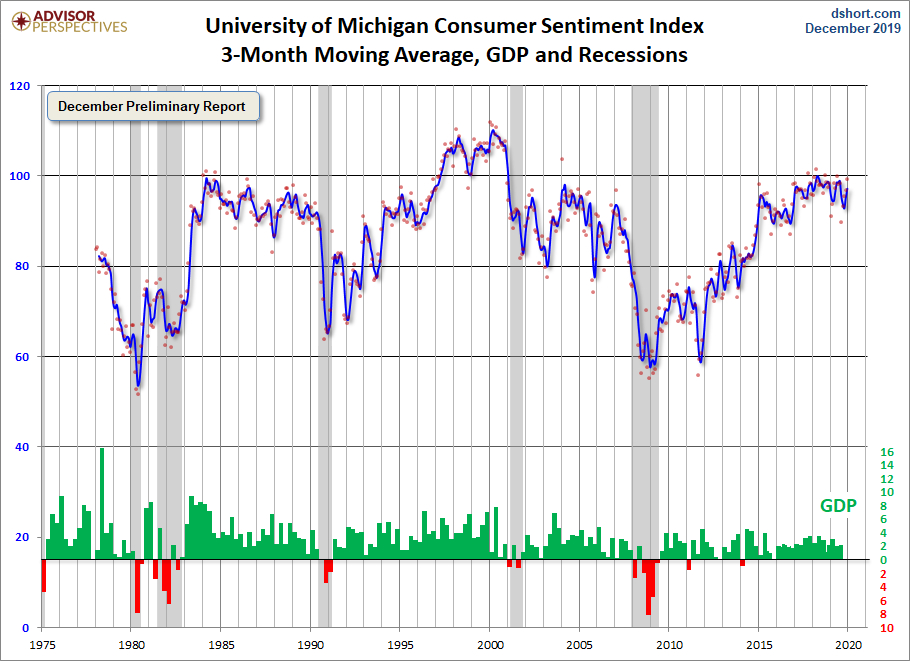

Note that this indicator is somewhat volatile, with a 3.0 point absolute average monthly change. The latest data point saw a 2.4 point increase from the previous month. For a visual sense of the volatility, here is a chart with the monthly data and a three-month moving average.

For the sake of comparison, here is a chart of the Conference Board's Consumer Confidence Index (monthly update here). The Conference Board Index is the more volatile of the two, but the broad pattern and general trends have been remarkably similar to the Michigan Index.

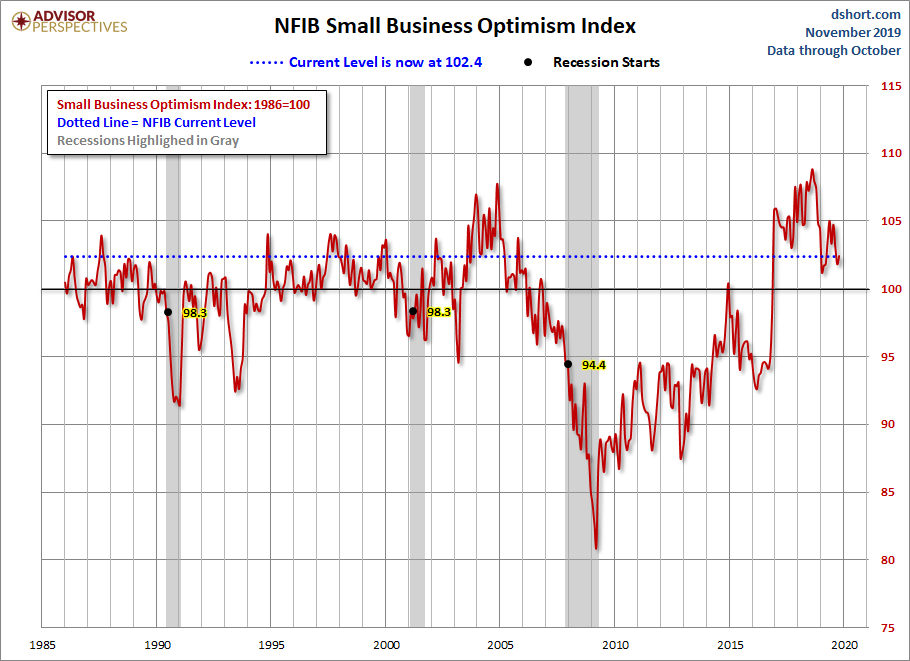

And finally, the prevailing mood of the Michigan survey is also similar to the mood of small business owners, as captured by the NFIB Business Optimism Index (monthly update here).

The general trend in the Michigan Sentiment Index since the Financial Crisis lows was one of slow improvement. The survey findings have neared the pre-recession peak.

The next update to this report will be for the December final data and will be published on December 20.

Comments

Log in or sign up to join the conversation.