MercadoLibre (MELI) is in the right place at the right time. The company is delivering accelerating growth and record performance across the board, and management is building solid foundations for sustained growth in the years ahead. Accelerating growth and expanding margins can provide powerful fuel for the stock price.

Expectations are going to be very demanding going forward, and a high bar is always difficult to beat. However, and in spite of the potential for short-term volatility, the long-term growth story in MercadoLibre looks stronger than ever.

MercadoLibre Is Firing On All Cilynders

Being the market leader in both e-commerce and fintech in Latin America, MercadoLibre is benefitting from massive tailwinds as demand is accelerating due to the pandemic. But this is already fully acknowledged by the market, and MercadoLibre went into the third quarter earnings report with a massive return of 130% on a year to date basis. Even for a great company benefitting from favorable conditions, beating aggressive expectations is never easy.

But MercadoLibre outperformed across the board, with both earnings and sales surpassing expectations by a wide margin and the company planting the seeds for sustained expansion in the years ahead.

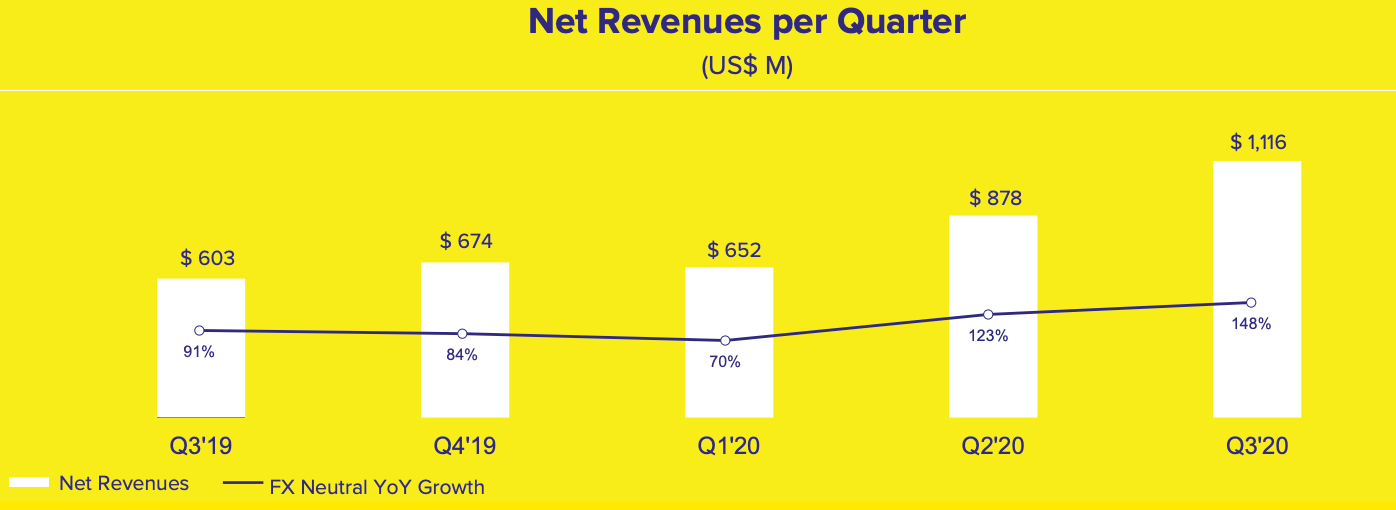

Net revenues for the third quarter were $1.1 billion, a year-over-year increase of 85.0% in USD, and 148.5% on an FX neutral basis. The number surpassed Wall Street expectations by $165.25 million.

Commerce revenues increased 109.3% year-over-year in USD, reaching $724.5 million. Fintech revenues increased by 52.3% year-over-year in USD to $391.2 million. Gross merchandise value came in at $5.9 during the quarter versus $5.3 billion expected by analysts, and total payment volume was $14.5 billion versus expectations for $13.1 billion. Mobile wallet delivered $3.2 billion in transactions, an increase of 380.5% year-over-year on an FX neutral basis.

Source: MercadoLibre

Although many countries in Latin America are still having a hard time due to the health crisis, mobility levels have been increased in the third quarter, but the company still managed to deliver accelerating performance.

It is not just that consumers are increasingly engaging with e-commerce and fintech services, but management is also making the right moves to capitalize on these opportunities and to maximize performance.

In Brazil, for example, the company increased the penetration of its managed network in commerce with initiatives such as a renewed focus on under-represented subcategories, improved rebate programs, and post-sale service enhancements for sellers and buyers.

These initiatives allowed MercadoLibre to gain market share across Brazilian e-commerce. The company also improved its Net Promoter Score by offering buyers some of the fastest delivery times in Brazil when shipping items from its fulfillment centers

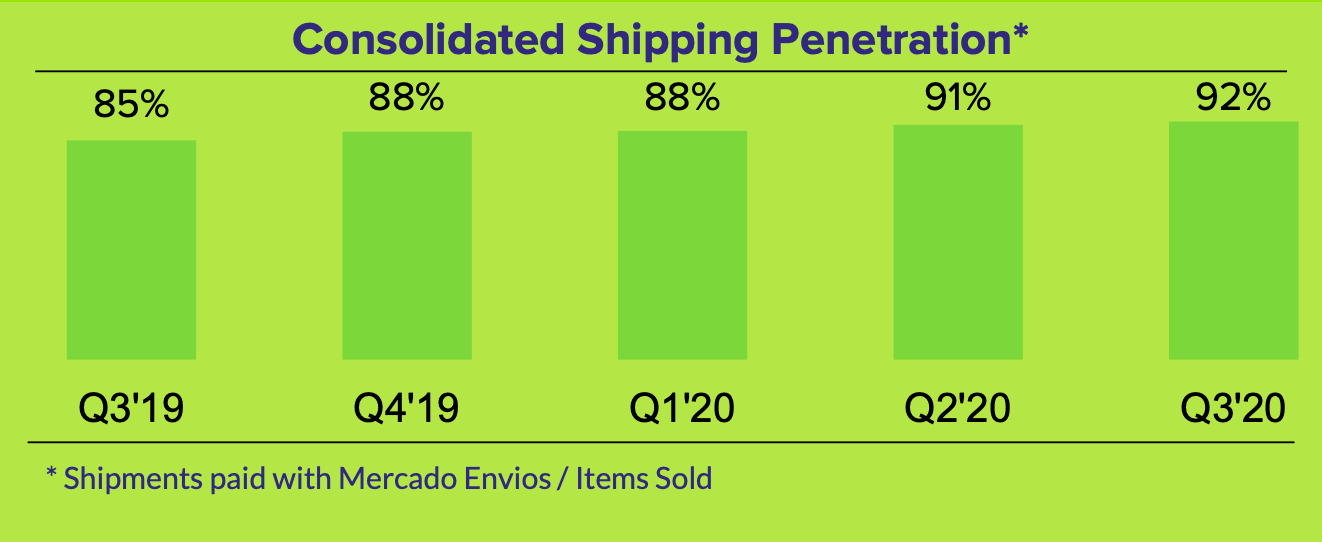

Shipping penetration has been booming lately. This has a negative impact on gross profit margins in the short term, but it also consolidates the company's strategic strength and competitive positioning over the long term.

Source: MercadoLibre

Online Payments had a strong performance during the quarter due to the shift to e-commerce consumption, accelerating sequentially to 204.3% on an FX neutral basis. The mobile wallet consumer base grew by 125.2% compared to the third quarter of 2019, reaching 13.7 million unique payers. The company's asset management product, Mercado Fondo, already has more than $540 million under management and over 13.6 million users across Latin America.

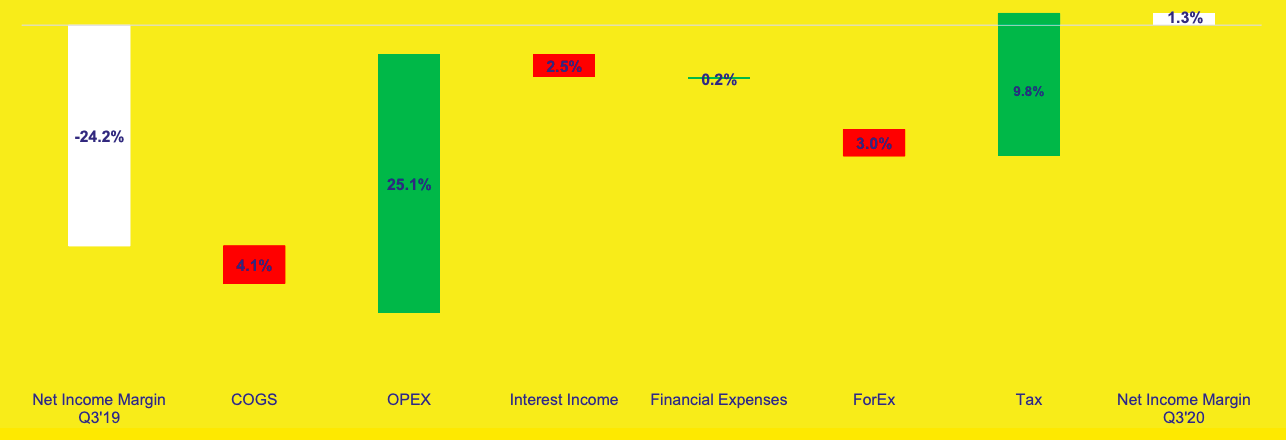

Gross profit was $480.2 million with a margin of 43.0%, a material decline versus 47.2% in the third quarter of 2019. This is due to an increase in shipping operation costs as a percentage of revenue.

On the other hand, operating expenses as a percentage of revenue declined to 35.6% versus 60.7%. This was driven by marketing expenditures efficiencies because of accelerating organic demand during the quarter.

At the bottom line level, the positive impact of the reduction in marketing expenditures had a much larger impact than the increase in shipping costs, so the net income margin is moving in the right direction. Needless to say, sustained revenue growth in combination with expanding profit margins can produce a double boost to earnings per share.

Source: MercadoLibre

Risk And Reward Going Forward

At current price levels, MercadoLibre is trading at a price to sales ratio of 18.3 times revenue estimates for 2020 and 13.6 times sales expectations for 2021. These are not cheap valuation levels by any means, but they are not unreasonable either considering the company's recent performance and future growth opportunities.

On the back of the recently released numbers, it wouldn't surprise me to see revenue estimates for this year and next year being adjusted higher in the coming days, which would mean that valuation is actually cheaper than it seems to be.

Nevertheless, expectations are going to be sky-high in the fourth quarter and next year. The holiday period and some increase in economic activity will be major tailwinds in the fourth quarter, but comparisons in 2021 are going to be much tougher. This can be a source of volatility for the stock in the near term.

That risk aside, the acceleration in demand is going to have long-term effects for MercadoLibre. The network effect is a major success driver in both e-commerce and fintech because buyers and sellers attract each other to the leading platforms in these fields, meaning that winners generally keep on winning in these industries. An expanding logistics network consolidates the company's leadership position even further.

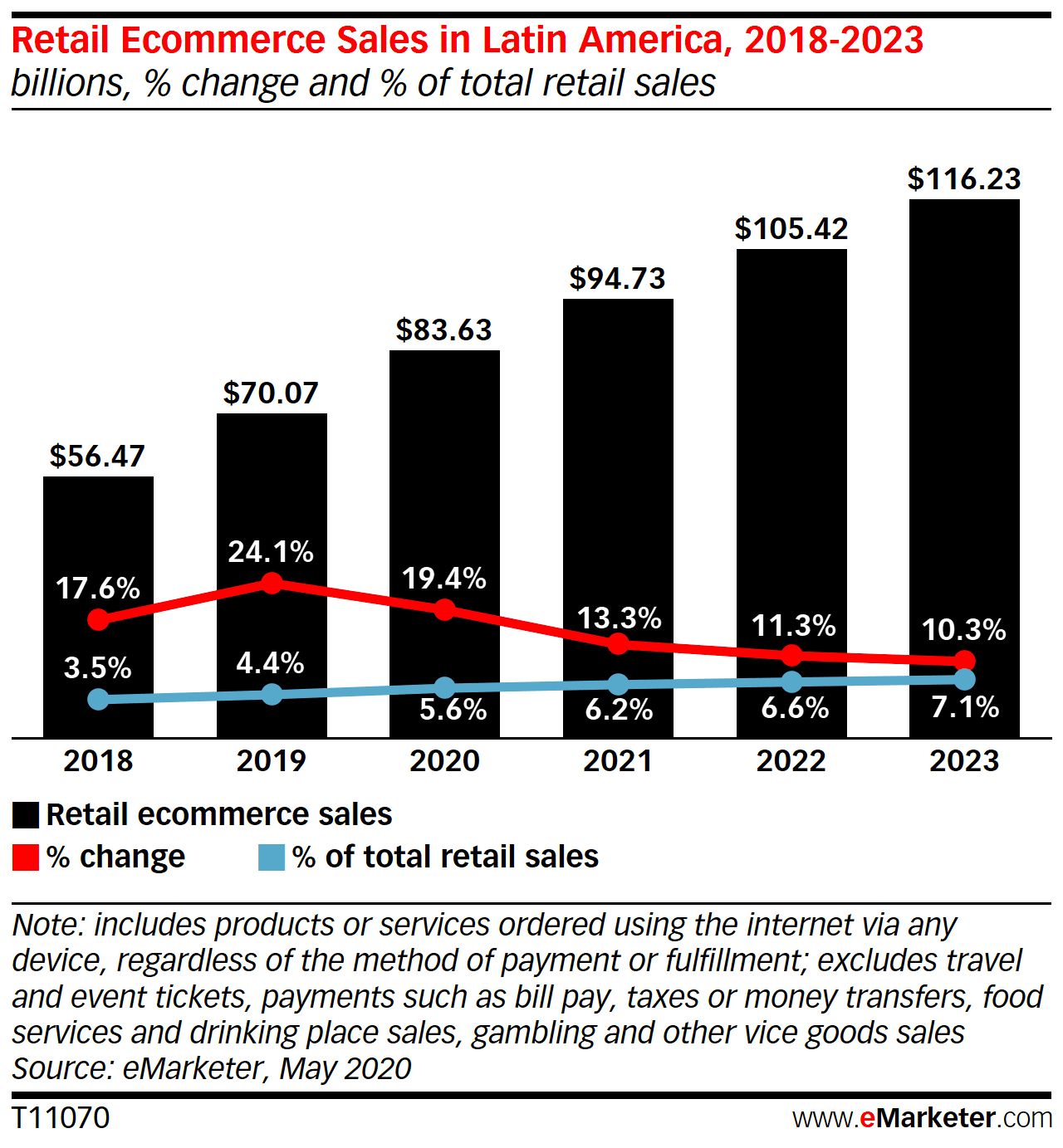

According to estimates by eMarketer, the acceleration in growth during the pandemic is going to be a game-changer for the Latin American e-commerce industry.

The implications of the pandemic are far-reaching and signal a watershed moment for e-commerce in Latin America. We estimate that 10.8 million consumers will make a digital purchase for the first time this year. This will bring the total digital buyer count to 191.7 million, or 38.4% of the region’s population ages 14 and older

Even when considering this acceleration in demand, e-commerce still represents only 5.6% of retail sales in the region, which leaves enormous room for further growth over the years ahead.

Source: eMarketer

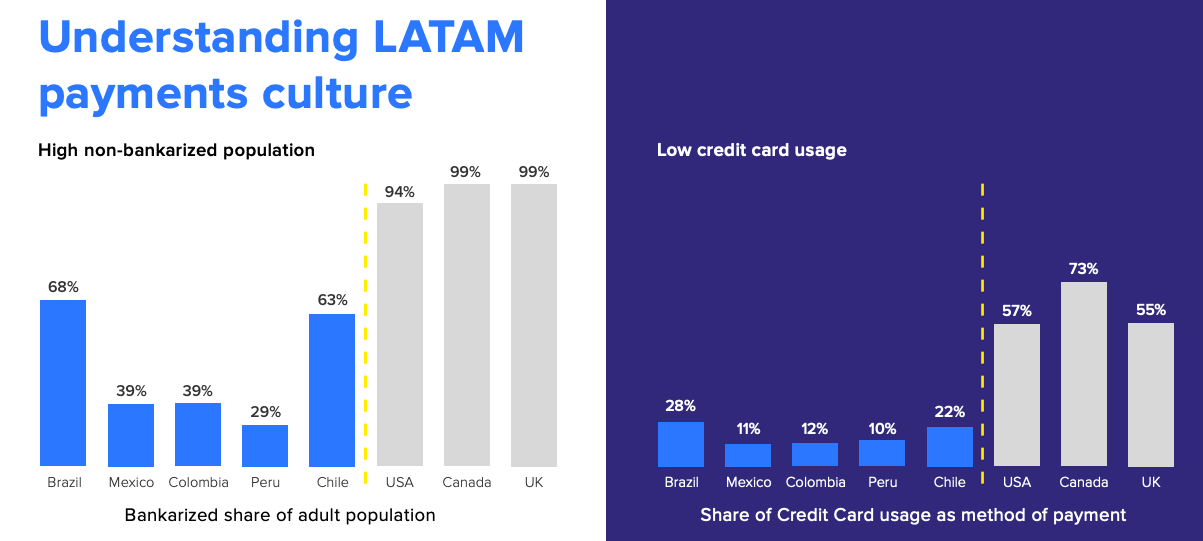

Regarding fintech, access to any kind of financial service is enormously lacking for large masses of the population in Latin America. This provides an enormous room for growth if management keeps executing well.

(Click on image to enlarge)

Source: MercadoLibre

After delivering spectacular earnings in the first three quarters of 2020 and a particularly strong report in the third quarter, the market is going to be demanding outstanding growth from MercadoLibre in the near future.

This can be a source of short-term volatility for the stock in the short term if the numbers for any specific quarter fail to meet expectations.

That notwithstanding, MercadoLibre is delivering vigorous financial performance and consolidating an undisputed leadership position in both online commerce and fintech in Latin America. Growth opportunities are enormous and management is executing well, so the stock is still offering abundant potential for appreciation in the long term.

Comments

Log in or sign up to join the conversation.