Price revulsion for risk continues following a cold weekend. Moods are wretched with the hope for central bankers to fix the financial conditions back to hot from freezing very much in doubt ahead of a long week of key economic and political events. Today was about risk-aversion extending with US/China trade relations in doubt as China calls the US ambassador to lodge a formal complaint regarding the Huawei CFO arrest. This continues with the European markets waiting for the Brexit vote tomorrow – now potentially in limbo - and the ongoing French yellow vest crisis bringing another weekend of mayhem. Politics in the US and Europe are easily priced by markets as voters make clear the direction and extent of change while in more autocratic places like China, these risks are opaque and leave open doubts. The China trade report over the weekend is an example where significant weakness in imports maybe a flashing red light for Xi and his policy approaches. Markets are grasping for anything good today, and coming up short, even in the UK where delaying the Brexit vote maybe just making for more GBP pain. The mood overall is wretched like the charts for most any risk asset.

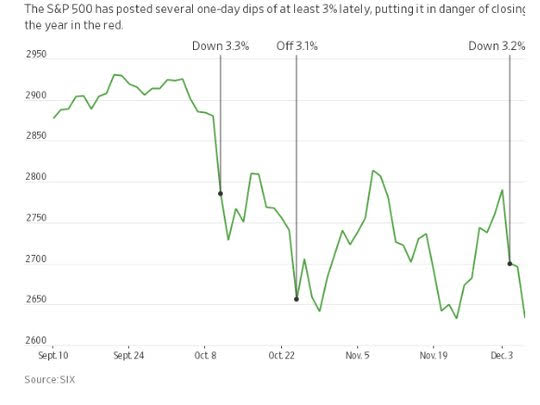

Question for the Day: Is there a Monday curse? Today is the mirror image of last week – then equities were bid and hopes for a trade truce led to double-digit gains, today the reverse is true. Markets are fickle and amoral. There is no calendar for mood-swings. The 3% curse of the last 3 months stands out in contrast to the relative calm of 2017 when the S&P500 had months of less than 1% movement. The lack of bounce in the equity markets globally distresses many investors and its historic as we need to go back to 1936 for a worse trading period. That maybe a wake-up call for the FOMC, which back then caused some of the pain with a rate hike.

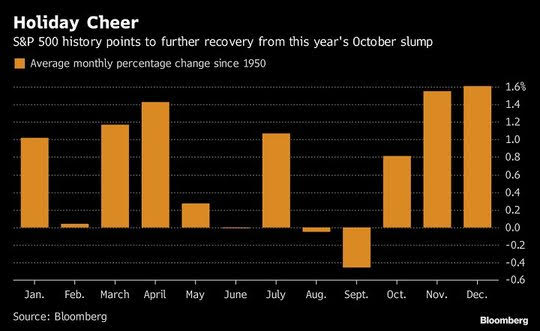

The other side of the coin that markets are watching is the usual seasonal flows that support the risk-on for December– as year-end bonuses, holiday spending and tax trades dominate the US markets. Whether the holiday cheer proves true rests on how next Monday feels, forget this one.

What Happened?

- Japan 3Q GDP revised lower to -0.6% q/q, -2.5% y/y after 0.7% q/q, 2.8% y/y – weaker than -0.5% q/q, -1.9% y/y expected. Capex revised lower to -2.8% from +2.8% worse than -1.6% expected. Private consumption revised to -0.2% q/q after 0.7% - worse than -0.1% expected. The price index unrevised at -0.3% y/y from +0.1%.

- Japan November EcoWatchers Survey 51 from 49.5 – better than 49.5 expected. The outlook also bounces to 52.2 from 50.6.

- Australian October home loans jump 2.2% m/m after -1% m/m - more than 0% m/m expected.

- German October Trade surplus E17.3bp from E17.7bn – slightly less than E17.7bn expected. Exports up 0.7% m/m after -0.4% while imports up 1.3% m/m after -0.4% m/m. The German October current account surplus narrows to E15.9bn from E21.4bn.

- Italy October industrial production up 0.1% m/m after -0.1% - better than -0.3% expected.

- UK October GDP up 0.1% m/m after 0% m/m – as expected. The 3M rolling average now 0.4% q/q after 0.6% q/q.

- UK October industrial production -0.6% m/m, -0.8% y/y after 0.1% m/m, -0.2% y/y – weaker than 0.1% m/m gain expected. Manufacturing -0.9% m/m, -1% y/y after 0.2% m/m, 0.5% y/y – weaker than 0.2% m/m, 0.5% y/y expected.

- UK October total trade deficit widens to GBP3.3bn after GBP2.23bn – worse than GBP2.9bn expected. The goods deficit GBP11.87bn after GBP10.68bn – also worse than the GBP10.5bn expected.

- Eurozone December Sentix investor confidence drops to -0.3 from 8.8 – weaker than 8.1 expected.

Market Recap:

Equities:

- Japan Nikkei off 2.12% to 21,219.50

- Korea Kospi off 1.06% to 2,053.79

- Hong Kong Hang Seng off 1.19% to 25,752.38

- China Shanghai Composite off 0.82% to 5,627.50

- Australia ASX off 2.26% to 5,627.50

- India NSE50 off 1.92% to 10,488.45

- UK FTSE so far up 0.3% to 6,797

- German DAX so far off 0.5% to 10,734

- French CAC40 so far off 0.5% to 4,788

- Italian FTSE so far off 0.55% to 18,638

Fixed Income: Running to safety now a stroll– The catch up trade in Asia, smoothes out in Europe – German Bund 10Y yields up 1bps to 0.26%, French OATs up 2bps to 0.71%, UK Gilts off 4bps to 1.23% - while periphery is mixed with Italy off 3bpst o 3.10%, Spain flat at 1.46%, Portugal flat at 1.80% and Greece flat up 1bps to 4.24%.

- US Bonds are in holding pattern ahead of supply, CPI, watching equities. 2Y up 2bps to 2.73%, 5Y up 1bps to 2.71%, 10Y up 2bps to 2.865%, 30Y

- Japan JGBs extend rally on risk-off– 10Y off 1bps to 0.042% with focus on BOJ reaction next.

- Australian bonds sold off despite equities– RBA Kent, China key – 10Y up 2bps to 2.46%.

Foreign Exchange: The US dollar index is up 0.1% to 96.63.

- EUR: 1.1415 up 0.1%.Watching 1.1380-1.1450 on the narrow and 1.13-1.15 still for the week with ECB and US rates driving.

- JPY: 112.75 flat. Watching 112-114 still with equities in charge – focus is on equities and BOJ.

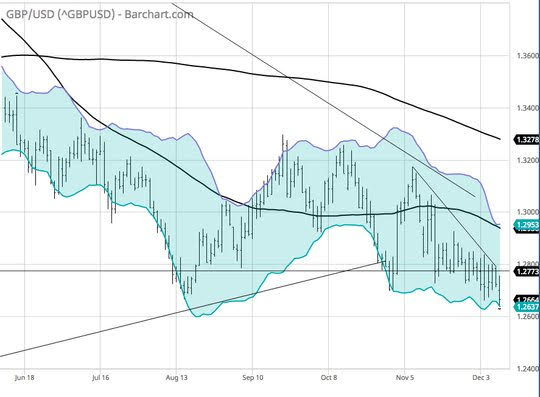

- GBP: 1.2650 off 0.5%.Watching Brexit mess still -1.2550 next then 1.24.

- AUD: .7205 up 0.1%.Even with horrible stock market and China trade hit – better than USD? NZD up 0.3% to .6885 with .6950 target.

- CAD: 1.3325 flat. Still in oil/BOC/China negatives vs. economic stability 1.3280-1.3350 keys.

- CHF: .9890 off 0.1%.Watching .98-1.00 for anything ahead of SNB decision this week.

- CNY: 6.9150 up 0.5%- pain trade showing up again with 6.96 key.

Commodities: Oil lower, Gold flat, Copper off 0.5% to $2.7770

- Oil: $51.91 off 1.3%.Range $51.56-$52.81 with Brent off 0.85% to $61.10 – watching $60 and equities first, OPEC and US supply second.

- Gold: $1246.70 flat. Range $1245.50-$1249.60 with $1250 and $1268 keys for upside watching USD and equities. Silver off 0.5% to $14.50 with $14.38-$14.75.

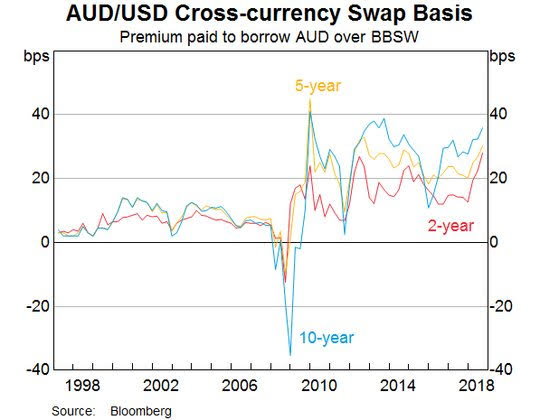

Conclusions: The year-end story for the USD maybe more about the basis swap and the role of hedging than anything else. The RBA kent speech today is a great primer for anyone that wants to get up to speed on this story – with an Australian perspective. The reason that Australian banks and the economy aren’t in a tailspin like some emerging markets even with a $500bn USD borrowing is important to consider and understand.

Economic Calendar:

- 0745 am BOC Lane speech

- 0815 am Canada Nov housing starts 206kp 196ke

- 1000 am US Oct JOLTS job openings 7.009m p 7.2m e

- 1130 am US 3M $39bn and 6M $36bn bill auction

Comments

Log in or sign up to join the conversation.