If yesterday was about bending, today is about the snap back fear. Rates up, equities down, USD up, commodities down – asset allocation and correlations will be driving investor decisions and the risk-party is looking for the punch bowl of liquidity. The best Services ISM ion record and FOMC Powell led US bond yields sharply higher to break out of their May highs and overnight continued to sell US bonds to 2011 levels over 3.20% in 10Y. Powell sees US monetary policy moving from neutral to restrictive in a gradual fashion – putting Fed Funds 3.25-3.75% range a real possibility in the 12-24 month horizon, something for the market to price. This has led to a stronger USD and hasn’t yet driven down equities, though global borrowers are on watch as higher US real growth means higher global rates. The US yield curve steepening maybe more a reflection of this reflexivity as bond yields in UK, Germany and Japan jump higher unwinding a term-premium demand for US paper. The snap back risk in rates upsetting the risk-parity party is clearly front and center but one that has notable limits from politics. The lack of China news this week stands out. The dampening effect of tariffs on confidence isn’t in play but it maybe later. Here are the key headlines that mattered in politics and policy beyond Powell overnight:

- UK proposal on Irish border “step in right direction,” according to the EU. The UK May plan to rush any deal through parliament added to view that Brexit talks part 2 are working.

- Vice President Pence tells China the US won’t be intimidated in the South China Sea. CNN reports the US Navy proposes a major show of forece to warn China.

- Italian government agrees on deficit to GDP targets of 2.4% in 2019, 21% in 2020 and 1.8% in 2021. A full budget is yet to be unveiled but will still be reviewed by the EU Commission which still can reject it. The Italian parliament will also have to approve it by the end of the year.

- ECB's Olli Rehn reiterated that ECB's role is "not to support the Italian bond market after its recent sell-off but to set policy for the whole of the Eurozone." Notably, he sees little contagion and therefore by implication little reason why the ECB monetary policy should respond., “...unless the rest of periphery starts weakening? "He added that the recent sell-off has not had any significant impact on other members, playing down fears that Italy's troubles could spread to others, like Portugal, Spain or Greece."

The game today is watching for any resistance to the US rate move and how it plays out with the data on Friday still the key turning point for the weekly picture. Expect that at 3.22% and 3.25% today. For the USD this matters as well and perhaps the tail can wag the dog. The EUR holding 1.1450 matters, same with GBP 1.29 and JPY 114.50. If USD breaks out like 10Y rates pay attention.

Question for the Day:How long can recoveries last? The market in the US is shocked by the headlines from ISM to USMCA with US jobs next. Expectations for growth are holding up and the FOMC Powell speech rings in the ears of all doubters. “There’s no reason to think this cycle can’t continue for quite some time, effectively indefinitely,” he said Wednesday in Boston. The Fed has been gradually raising its benchmark rate and doesn’t look ready to stop. Mr. Powell said policy was “a long way from neutral” meaning not restrictive which he implies is over 3%.

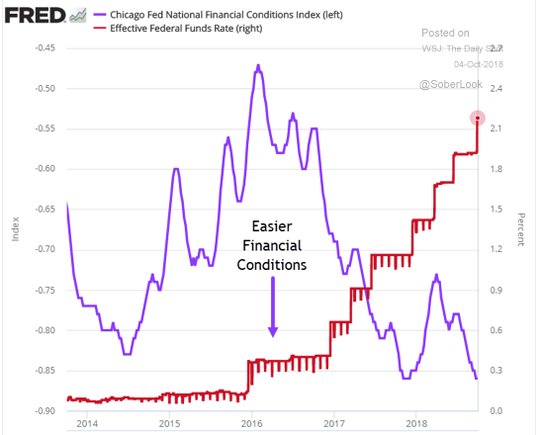

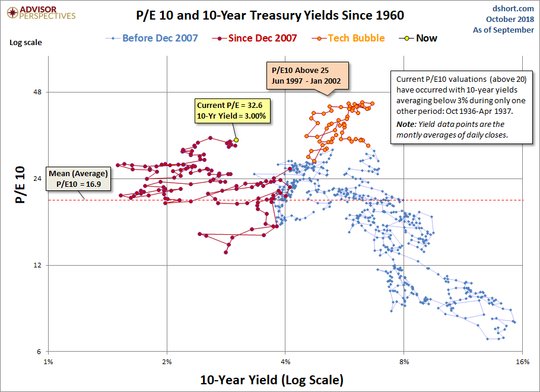

The most notable chart used by economists to explain that policy is indeed easy (if not accommodative) is this one of financial conditions against the rising Fed Funds rate. The point is that until financial conditions normalize like rates, fear of a recession is overblown. Recoveries don’t die of old age, they are murdered by policy mistakes. The risk of such is usually telegraphed by the market and the lack of P/E to US yield concern - ie valuation metrics - has been kind in 2018 due to earnings. This makes 3Q earnings reports and 4Q outlooks that much more important.

What Happened?

- Australia August trade surplus A$1.6bn after A$1.55bn – better than A$1.4bn expected. Exports rose 1% m/m to A$36.56bn mostly due to gold and rural goods partially offset by a 1% drop in ores and minerals. Iron Ore was up 9% to A$298mn (mostly a quantity, not price story) while thermal coals fell 4% to A$106mn (also due to quantity despite price rises). Imports were almost flat up A$130mn to $34.96bn after a rise in capital goods (aircraft) was offset by intermediate goods.

- German August VDMA machine orders up 7% y/y with 8% y/y rise in domestic and 6% y/y in foreign. The 3M rolling average now 8%. "This was due to demand from the euro partner countries, which stagnated in August, while 8 percent more orders were received from non-euro countries. However, the euro countries are also on a growth course this year. Their incoming orders reached a plus of 4 percent in the first eight months", explains Dr. Ralph Wiechers, Chief Economist of the VDMA.

Market Recap:

Equities: The US S&P500 futures are off 0.5% after a 0.07% gain yesterday. The Stoxx Europe 600 is off 0.7% - worst in over 2-weeks –while the MSCI Asia Pacific fell 1.2% - biggest drop in over 4-weeks. MSCI EM is off 2% worst drop in over 6 months.

- Japan Nikkei off 0.56% to 23,975.62

- Korea Kospi off 1.52% to 2,274.49

- Hong Kong Hang Seng off 1.73% to 26,623.87

- China Shanghai Composite closed for holiday

- Australia ASX up 0.46% to 6,283.90

- India NSE50 off 2.79% to 10,555.10

- UK FTSE so far off 1.1% to 7,428

- German DAX so far off 0.4% to 12,235

- French CAC40 so far off 1.1% to 5,433

- Italian FTSE so far off 0.5% to 20,635

Fixed Income: The move up in US rates drives EU bonds from the open. UK hit hardest with 10-year Gilt yields up 8bps to 1.655%, German Bunds up 5.5bps to 0.53%, French OATs up 5.5bps to 0.87%. The periphery remains key focus and does better – Italy up 4.7bps to 3.355%, Spain up 2bps to 1.55%, Portugal up 1bps to 1.895%, Greece up 12bps to 4.47%.

- UK DMO sold GBP2.5bn 5Y 1% Apr 2024 Gilts at 1.304% with 2.02 cover – previously 1.11% with 1.92 cover.

- France sold E8.862bn of bonds at higher rates and mixed demand –E4.645bn of 10Y 0.75% Nov 2028 OAT at 0.86% with 1.59 cover – previously 0.71% with 1.95 cover – E1.42bn of 15Y 1.25% May 2034 OAT at 1.23% with 1.59 cover – previously 1.11% with 1.6 cover – and E2.797 of 30Y 2% May 2048 OAT at 1.70% with 1.39 cover – previously 1.65% with 1.35 cover.

- Spain sold E4.64bn of bonds, with higher rates and good demand– E2.718bn of 3Y 0.5% Jan 2021 Bono at 0.128% with 1.78 cover, E1.043bn of 10Y 1.4% July 2028 Oblig at 1.54% with 2.38 cover – previously 1.42% with 1.5 cover – and E0.885bn of 11Y 6% Jan 2029 Oblig at 1.538% with 1.96 cover. Also Spain sold E0.41bn of 5Y 0.15% BonoEi at -0.723% with 4.85 cover – previously 2.25.

- US Bonds continue bear steepening move– 2Y up 1bps to 2.882%, 5Y up 1.7bps to 3.062%, 10Y up 2.8bps to 3.21%, 30Y up 3.8bps to 3.374%.

- Japan JGBs see curve steeper after MOF liquidity auction, tracks US moves – 2Y up 0.4bps to -0.123%, 5Y up 0.9bps to -0.067%, 10Y up 2.1bps to 0.149%, 30Y up 3.8bps to 0.945%. The MOF sold Y500bn of 15.5-39 year bonds saw a wider tail (0.9bps from 0.06bps), higher average spread (0.028% from -0.001%) and lower bid/cover (1.839 from 2.261). The focus now turns to Friday BOJ Rinban and long end size.

- Australian bonds see curve steeper in catch up to US-3Y up 3bps to 2.015%, 10Y up 7bps to 2.705%.

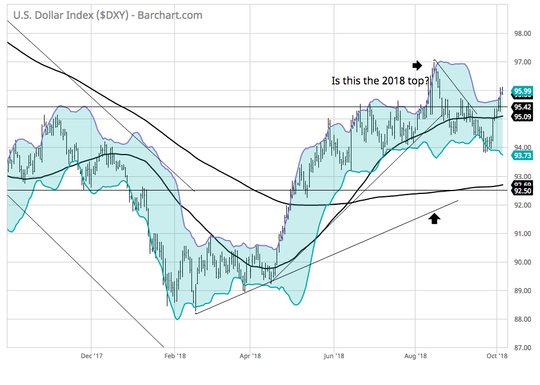

Foreign Exchange: The US dollar index is up 0.1% to 95.87 with 95.84-96.12 range – breaking out with bond yields – focus shifts to 95.70 base for 96.99 the August 15 highs. In EM, USD is bid– EMEA: ZAR off 0.25% to 14.686, TRY off 2% to 6.168, RUB off 0.6% to 66.29; ASIA: TWD off 0.4% to 30.795, KRW off 1% to 1129.80, INR off 0.5% to 79.705.

- EUR: 1.1500 up 0.15%.Range 1.1464-1.1506 with rates, Italy and technical support at 1.1450 key for 1.1550-80 bounces.

- JPY: 114.30 off 0.2%.Range 114.22-114.55 with EUR/JPY 131.40 flat – watching equities vs. rates with 115 barrier in play and 114 pivotal support for 112.80 risk again.

- GBP: 1.2980 up 0.3%.Range 1.2922-1.2995 with EUR/GBP .8860 off 0.15% - watching Brexit and rates with 1.29 key holding

- AUD: .7080 off 0.3%.Range .7066-.7112 with A$ melting on China trade worries, rates but .7050 holding. NZD .6490 off 0.35% with .64 next key.

- CAD: 1.2870 flat.Range 1.2865-1.2889 with focus on rates, data ahead, 1.2820 vs. 1.2950 consolidation.

- CHF: .9915 off 0.1%.Range .9900-.9926 with EUR/CHF 1.1400 up 0.1% - Italy, rates, focus is on EUR with 1.00 next big level in $.

Commodities: Oil lower, Gold up, Copper up 0.75% to $2.8450.

- Oil: $76.31 off 0.1%.Range $75.99-$76.47. WTI $74.30 the Oct 3 lows now a support ahead of $70 base with $77 and $79 resistance. Brent $86.15 off 0.15%with $87 target still in play with $80 support. Yemen/Saudi conflict put oil bid late yesterday but US EIA and Russia energy minister seeing prices a bit too high balance against this. Spare capacity in Libya, Saudi and Russia should make up for Iran and Venezuela output declines. Saudi is investing $20bn in spare capacity as an example.

- Gold: $1199.40 up 0.15%.Rang $1190-$1201. Gold watching $1203 55-day against $1181 support. Silver, $14.63 off 0.1%, still watching $14.755 55-day and $14.50 pivotal support. Platinum off 0.3% to $823.40 and Palladium off 0.2% to $1057.

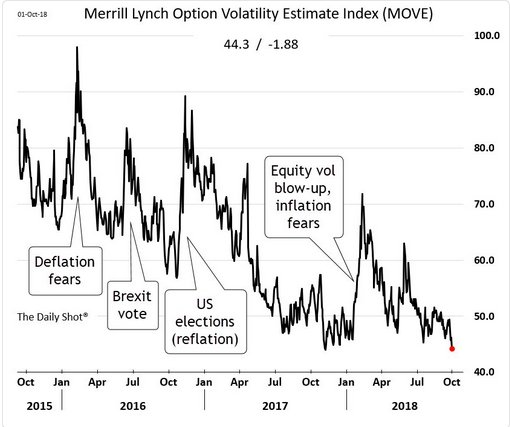

Conclusions: Is the lack of volatility in bonds and FX about to change? Short answer, that train already left the station. The chart of the MOVE index from Monday says it all. The move up in US rates has caught the market by surprise in part because of the muted reaction to the FOMC last week, which this week is clearly spelling out their dot-plot thinking and views. The risk of more rate noise is bleeding into the FX market and making that more interesting in the G10 and adding to the pain trade in the EM space.

Economic Calendar:

- 0830 am US weekly jobless claims 214k p 210k e

- 0915 am Fed VC Quarles speech

- 1000 am US Aug Factory Orders (m/m) -0.8%p +0.9%e / ex autos 0.2%p 0.4%e

- 1000 am Canada Sep Ivey PMI 61.9p 61.4e

- 0300 pm Bank of Mexico rate decision – no change from 7.75% expected.

Comments

Log in or sign up to join the conversation.