Imagine a happy Sysiphus, pushing the rock up the hill, almost to the end, then gravity returns the stone back down day after day. Investors climb the wall of worry in a similar fashion but the mood is determined by where the rock is relative to the hill. Now imagine US/China trade talks as they appear almost finished, according to the FT, but tariff removal and enforcement issues push us back to reality. Imagine Brexit deals where cross-party talks open the chance for a softer plan and a long extension with the EU but rip the Tory Party into a deeper civil war and open new election risks. Imagine growth globally recovering with China March PMI bouncing but the forces of the credit bubble pop driving PBOC reactions to stem speculation, driving bonds lower and growth outlooks back down. Imagine the RBA willing to cut but for the new budget and a surprise bounce back in retail sales. There are lessons from the myths of Greece and perhaps today is the day we relearn them. Too much debt means longer-term problems. The ability for central bankers to cut and stabilize markets may not be enough in the next downturn. The policy pivot from the FOMC and others drove markets in 1Q and remain the key to 2Q. There are tidbits for change afoot – from the sharp selling of China bonds to the sharp rally in equities to the stalled FX emerging market currencies where ARS and TRY remain the fear trades.

- Australian Government budget sees A$7.1bn surplus for FY2020 and cuts GDP forecast to 2.75% from 3% - unlikely to be a budget to change RBA rate cut risks.

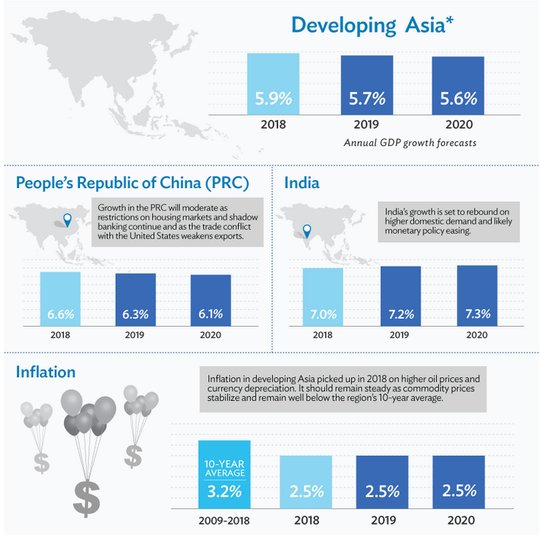

- Asia Development Bank sees growth softening in region to 5.6% in 2020 from 5.9% in 2018.

- Turkey CPI rose just 1.03% m/m, 19.71% y/y– more than the 19.5% expected – but down from the 25% highs in 4Q.

What this all means for today rests on how the momentum factors for equities and commodities play against the reality of economics. The bounces in PMI were not sufficient for Europe. Bunds are flashing yellow even as the DAX rallies. The EUR is nowhere and the GBP is ignoring the clear costs of Brexit as shown by its shrinking services PMI. The barometer of choice today is in EM markets with the MXN the right mixture of politics, economics, and liquidity – watching 19.15 as the pivot for 18.80 retest and more risk-on carry plays with less border closing fear.

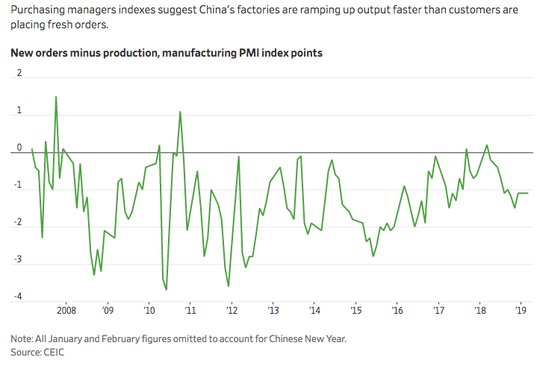

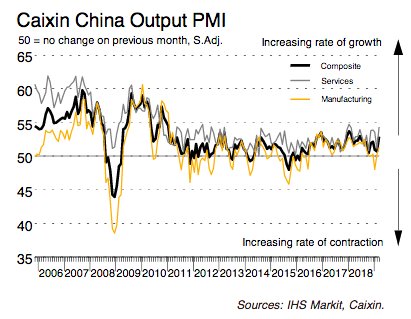

Question for the Day: Is the China PMI bounce a seasonal blip? The risk of the present market is that PMI reports don’t reflect the underlying economy. New orders may not match production as the inventory cycle returns to matter in China and elsewhere. The noise of the Vale dam collapse and its effect on steel manufacturing is another factor – one that the WSJ highlights today. The real key will be in the data ahead and that uncertainty matters as markets drive up risk assets before their release. The gap between expectations that all is fine with global growth versus the noise of restocking maybe the risk that caps oil prices, returns yield curves to inversion and drives down the equity markets from their torrid pace of gains.

Adding to the doubt about China and the regional bounces in PMI is the Asia Development Bank forecast cuts with growth moving from 5.9% in 2018 to 5.7% in 2019 and 5.6% in 2020. Specific to China, the ADB notes: “… structural changes in the economy away from industry and towards services and financial tightening as the government seeks to control financial risks will likely see economic growth moderate to 6.3% in 2019 and 6.1% in 2020 from 6.6% in 2018. Slower growth is to be expected as the PRC economy matures.”

What Happened?

- Australia March AIG services PMI gains to 44.8 from 44.5 – weaker than 45 expected. This was the first year since Aug 2010 that every sector contracted. By category, retail trade trend fell 1.8 to 37.6, hospitality fell 2.7 to 42.5, health/education fell 1.7 to 44.7, recreation fell 5 to 42.1, property fell 0.4 to 49.4, wholesale trade fell 0.3 to 44.7, finance fell 0.5 to 49.6 and transport fell 1.4 to 44.3.

- Australia March final CBA services PMI 49.3 from 48.7 – weaker than 49.8 flash expected. This puts the composite PMI at 49.5 from 49.1 – also weaker than 49.8 expected. Employment was basically flat, and subindex is the lowest since survey started in May 2016. Business confidence remains upbeat with business expansions higher, sales projections better.

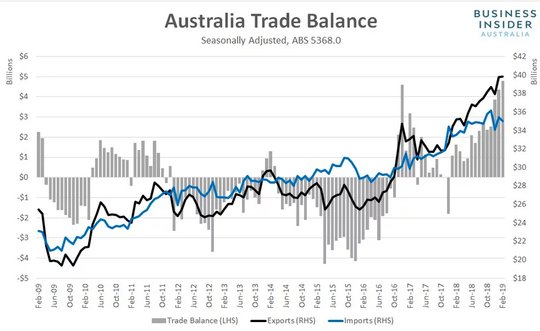

- Australia February trade surplus A$4.801bn after A$4.351bn – more than A$3.8bn expected, - new record. The exports rose 1% m/m to A$39.833bn after a 4.8% gain – less than the 2% expected – but imports fell 1% m/m to A$35.032bn after a 3.9% gain and less than the 1% expected. In February, exports of metal ores and minerals, predominantly iron ore, surged by $958 million, helping to offset a steep $760 million drop in the value of coal exports. The surge in iron ore largely reflects higher prices following supply disruptions in Brazil stemming from a mining disaster in late January. The equally large drop in coal exports may reflect reports of delays in Australian shipments being processed at Chinese ports during the month.

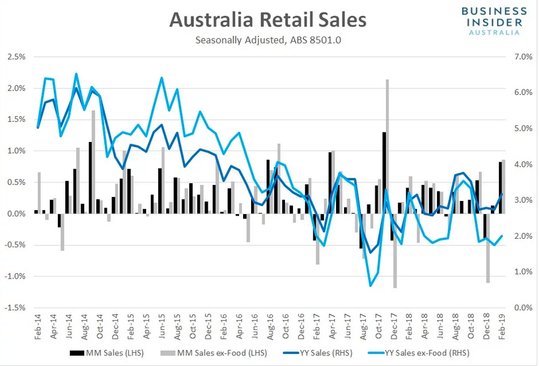

- Australia February retail sales jump 0.8% m/m after 0.1% m/m – better than 0.2% m/m expected. Ex-food sales rose 0.9% after 0% m/m. The ABS economic survey director, Ben Faulkner said: "There were improved results across most industries with rises in food retailing (0.8 per cent), department stores (3.5 per cent), household goods retailing (1.1 per cent) and clothing, footwear and personal accessory retailing (1.6 per cent). Other retailing (0.0 per cent) and cafes, restaurant and takeaway services (0.0 per cent) were relatively unchanged. The rise this month follows subdued results in December 2018 (-0.4 per cent) and January 2019 (0.1 per cent)."

- Japan March services PMI 52 from 52.3 – weaker than 52.1 expected – but best quarter since 2Q 2017. Nevertheless, business confidence sinks to 18-month lows and the Composite PMI fell to 30-month lows at 50.4 from 50.7.

- China March Caixin services PMI 54.4 from 51.1 – better than 52.3 expected – best since Jan 2018. This puts the composite PMI at 52.9 from 50.7 – better than the 50 expected – best since June 2018. New orders for services were the best in 14 months. New export sales rose to the second best rate since Dec 2017. Employment rose fractionally – similar to February. Overall confidence rose slightly, with Services at 3-month highs and Manufacturing at 10-month highs, but both remain below the long-run average.

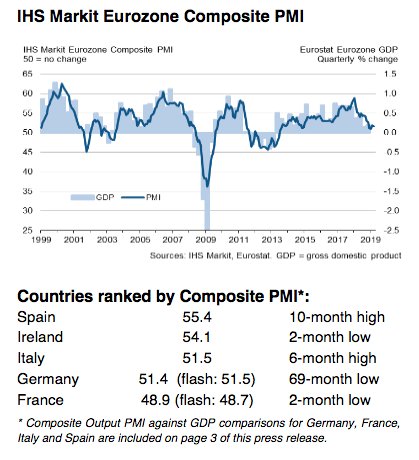

- Eurozone March final services PMI up to 53.3from 52.8 – better than 52.7 flash – best since November. However, the composite PMI fell to 51.6 from 51.9 – better than the 51.3 flash. Services bounced more than manufacturing sagged. New service orders rose to 4-month highs led by Spain and Germany. IHS sees 1Q GDP for Eurozone at 0.2% q/q.

- Spain services PMI 56.8from 54.5 – better than 55 expected – best since Feb 2018.

- Italy services PMI 53.1from 50.4 – better than 50.8 expected – best since Sep 2018.

- France final services PMI 49.1from 50.2 – better than 48.7 flash - but the composite PMI 48.9 from 50.4 – weaker than 49 expected.

- German final services PMI 55.4from 55.3 – better than 54.9 flash and 6M highs– but the composite PMI 51.4 from 52.8 – weaker than 51.5 flash.

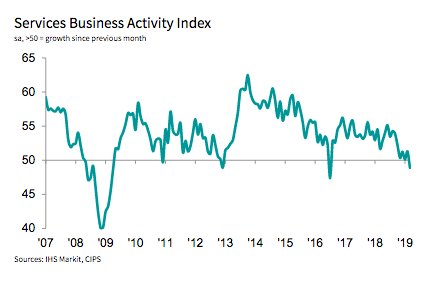

- UK March services PMI 48.9 from 51.3 – weaker than 50.9 expected – worst since July 2016. The composite PMI fell to 50 from 51.4 – making this the worst quarter since 4Q 2012. IHS sees 2019 GDP for UK now at 0.8% well below the 1.3% y/y consensus. The jump in manufacturing was unable to offset the weakness in services. Service new orders fell for the 3rdmonth as Brexit uncertainty dominates.

- Eurozone February retail sales up 0.4% m/m, 2.8% y/y after revised 0.9% m/m, 2.2% y/y – better than 0.2% m/m, 2% y/y expected– but January revised lower from 1.3% m/m. The non-food sales rose 0.9% m/m, while food/drink rose 0.1% m/m and auto fuel fell 0.7% m/m. Sales were highest in Belgium up 1.6% while Portugal fell 1% m/m.

Market Recap:

Equities: The S&P500 futures up 0.5% after a flat result yesterday. The Stoxx Europe 600 is up 0.6% with 4thday of gains while Asia rips higher with MSCI Asia Pacific up 1.1%.

- Japan Nikkei up 0.97% to 21,713.21

- Korea Kospi up 1.20% to 2,203.27

- Hong Kong Hang Seng up 1.22% to 29,986.39

- China Shanghai Composite up 1.24% to 3,216.30

- Australia ASX up 0.65% to 6,368.70

- India NSE50 off 0.59% to 11,643.95

- UK FTSE so far flat at 7,392

- German DAX so far up 1.15% to 11,889

- French CAC40 so far up 0.55% to 5,454

- Italian FTSE so far up 1% to 21,740

Fixed Income: Risk-on extends and better global services PMI drive but EU bonds are mixed – German 10-year Bund yields off 2bps to -0.05%, France up 2bps to 0.40%, UK Gilts up 3bps to 1.08% while periphery is bid – Italy off 1bps to 2.51%, Spain off 1bps to 1.14%, Portugal off 1bps to 1.27% and Greece off 5bps to 3.65%.

- US Bonds are offered in bear steepening with risk-on equities, waiting for ADP– 2Y flat at 2.33%, 5Y up 1bps to 2.32%, 10Y up 2bps to 2.51%, 30Y up 2bps to 2.91%.

- Japan JGBs offered in quiet market- BOJ kept buying unchanged despite chatter. Focus shifts to 30Y sale tomorrow. 2Y flat at -0.15%, 5Y flat at -0.17%, 10Y up 1bps to -0.05%, 30Y flat at 0.52%.

- Korea BOK sold KRW3trn in 2Y stabilization bonds at 1.74% down from 1.85%.

- Australian bonds sold on retail sales, curve steeper again– 3Y up 1bps to 1.44%, 10Y up 6bps to 1.88%, NZD 10Y up 7bps to 1.94%.

- China PBOC skips open market operations for 11th day. Fitch has negative outlook for China bank debt, sees profit growth in single digits medium term. China bonds sold with steepening trade– 2Y up 1bps to 2.64%, 5Y up 6bps to 3.03%, 10Y up 11bps to 3.24%.

Foreign Exchange: The US dollar index is off 0.2% to 97.03. The emerging markets are mixed with ASIA: INR up 0.5% to 68.58, KRW flat at 1133; EMEA: RUB flat at 65.199, ZAR flat at 14.14 and TRY off 2.4% to 5.617

- EUR: 1.1250 up 0.4%. Range 1.1200-1.1255– focus is on bounce in German services, rates and US data ahead.

- JPY: 111.50 up 0.15%.Range 111.21-111.58 with EUR/JPY 125.40 up 0.55% - all about equities and risk-mood with 112 back in play

- GBP: 1.3165 up 0.25%.Range 1.3121-1.3196with EUR/GBP .8540 up 0.1% - all about 1.30-1.33 holding and Brexit deals

- AUD: .7115 up 0.65%.Range .7054-.7127 with retail sales and trade pushing rate rethink – watching .7220 after .7050 holds. NZD .6795 up 0.55% - lags to A$ with .6740 base.

- CAD: 1.3305 off 0.25%.Range 1.3296-1.3353 with focus on crosses, 1.3250 test in play with oil and politics drivers.

- CHF: .9965 off 0.15%.Range .9967-.9988 with EUR/CHF 1.1210 up 0.3%. Less fear and .9880 holding opens 1.00 and 1.1250 tests.

- CNY: 6.7075 off 0.2%. Range 6.7050-6.7220 with focus on trade talk hopes. PBOC fixed at 6.7194 from 6.7161.

Commodities: Oil up 0.4%, Gold up 0.2%, Copper up 0.5% to $2.9315

- Oil: $62.67 up 0.15%.Range $62.46-$62.99 with Brent up 0.45% to $69.69 watching $70 for breakout.

- Gold: $1298 up 0.2%.Range $1294.50-$1298.80 with $1301 and $1305 next watching USD wobble against risk on mood. Silver up 0.5% to $15.14, Platinum up 1.9% to $868.80 and Palladium off 0.3% to $1396.20.

Economic Calendar:

- 0815 am US Mar ADP employment change 183k p 165k e

- 0830 am Atlanta Fed Bostic speech

- 0945 am US Mar final services PMI 56p 54.8e / composite 55.5p 54.3e

- 1000 am US Mar services ISM 59.7p 58.7e

- 1030 am US weekly EIA oil inventory 2.8mb p 3mb e / gasoline -2.883mb p -2.77mb e

- 0500 pm Minn Fed Kashkari speech

Comments

Log in or sign up to join the conversation.