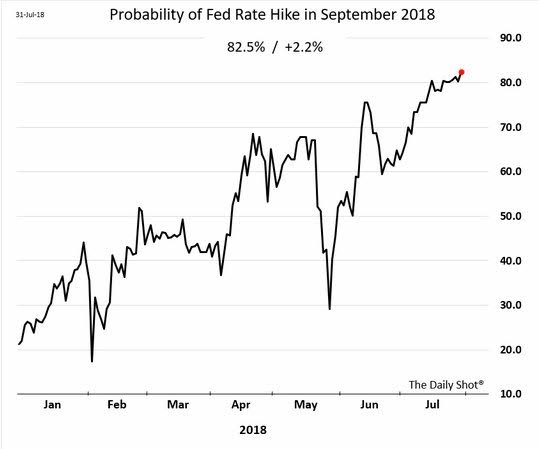

The “what will Powell do” fears seem less dramatic than “what will Trump do” as markets flip the calendar to August. The ratcheting up of trade fears counterbalances the fear of central bankers normalizing. Trade war focus returns with Trump administration proposing raising tariffs to 25% from 10% on the $200bn in Chinese imports, however, US Treasury Secretary Mnuchin and Chinese Vice Premier Liu are looking for ways to restart negotiations. This maybe the reason August gets exciting with FOMC meeting today expected to clearly lead to a September hike. But the Fed isn’t the only one ready to act.

- India RBI delivers 25bps hike as expected. The central bank kept its forecast for GDP at 7.4% for 2018-2019. "The progress of the monsoon so far and a sharper than the usual increase in MSPs of kharif crops are expected to boost rural demand by raising farmers’ income," the MPC said.

- Korea November Hike being priced. Some BOK board members stressed the need to raise rates sooner rather than later, according to minutes from the July 12 policy meeting released.

- In addition to the FOMC today, we still have Brazil COPOM, UK BOE, Czech National Bank and Mexico central on the docket for tonight and tomorrow.

The overnight focus was not on either trade or monetary policy as much as on economic data with the global Manufacturing PMI reports mostly softer and troubling to the future outlooks which are beginning to show the wear and tear of trade war talk and rate hike normalizations. This is August and it’s a hard month to trade traditionally, with the first few weeks light and the last one usually filled with those ready to get ahead of Autumn change. The risk mood today is weaker as fears are ratcheting up across all three factors – trade, rates, and economics – leaving the news from the US a key driver and the USD up trend a barometer for trouble.

Question for the Day: Is the US/China trade war just noise? Markets have moved away from the view that US/China trade tensions are elephants fighting and that the EM and EU suffer more. Whether this is true remains to be seen. The bounce back in EM shares and FX suggest investors are buying the dip, with the ongoing support being that the emerging markets are a value and carry proposition but the economics are mixed. The reality is that this could merely be a bear-market recovery for the summer.

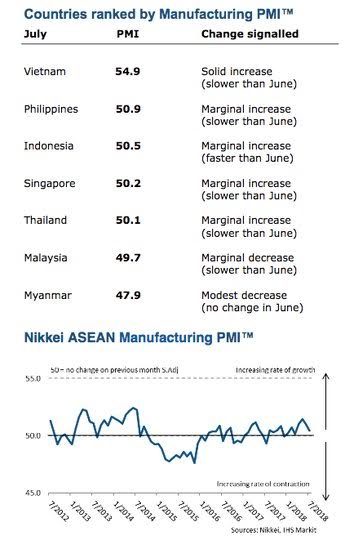

The ASEAN July Manufacturing PMI fell to 50.4 from 51 – a four-month low – with weaker gains in output and new orders but exports returned to growth highlighting the view that US trade fears are contained. However, the biggest key maybe in the optimism dropping to survey lows and future output index fell to new record lows.

What Happened?

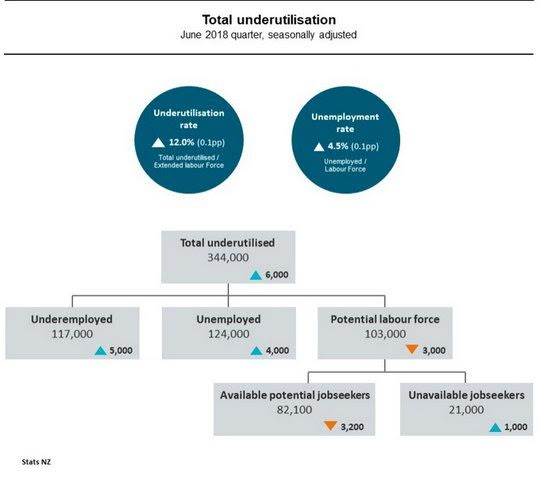

- New Zealand 2Q unemployment rose to 4.5% from 4.4% - worse than 4.4% expected. The employment change rose 0.5% q/q after 0.6% - better than 0.4% expected. The average hourly earnings rose just 0.2% - less than 1% expected, while the private labor cost index was 0.6% - as expected. The participation rate rose to 70.9% after 70.8% - also more than 70.8% expected.

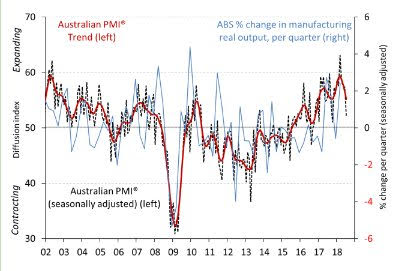

- Australia July AIG Manufacturing PMI, fell to 52 from 57.4 – weaker than 56.8 expected, while the CBA Manufacturing PMI also dropped to 52.4 from 55. The AIG PMI showed July new orders -6.5 to 51.1, exports -3 to 49.9 and employment -7.8 to 50.3.

- Japan July Nikkei Manufacturing PMI 52.3 after 53 – better than 51.6 flash. New orders rose slower – softest growth since Oct 2016 – but delivery times lengthen to 7-year highs and both input and output prices are at mult-year highs. Planned expansions into new markets and new product launches were supporting confidence but overall index on optimism fell to 4-month lows.

- China July Caixin Manufacturing PMI drops to 50.8 from 51.0 – slightly weaker than 50.9 expected – 8-month lows. The report pointed to "new export sales declining at the quickest rate in over 2 years," while there were slower increases in output and new orders.

- Caixin also noted "on the price front, the rate of input cost inflation weakened since June, but remained elevated, while output charges rose only modestly." Employment across China’s manufacturing sector continued on a downward trend in July, with some companies lowering staff due to company downsizing.

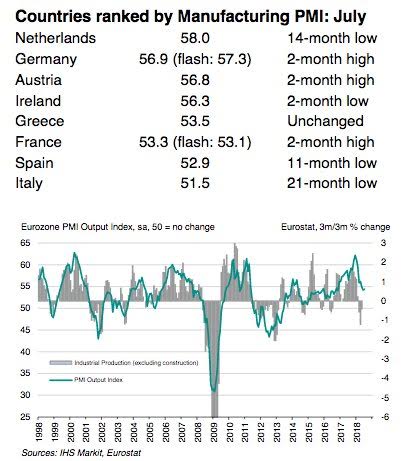

- Eurozone July Manufacturing final PMI 55.1 from 54.9 – unchanged from flash – as expected. The new export order growth is at 2-year lows with tariffs/trade war concerns noted. Employment index grew across the EU. The overall headline is still the second weakest outcome in 1½ years.

- Spanish July Manufacturing PMI 52.9 from 53.4 – weaker than 53.0 expected. Weakest rise in new orders since Aug 2017 with both employment and purchasing also slower. Input costs rose to 5-month highs.

- Italian July Manufacturing PMI 51.5 from 53.3 – weaker than 53.0 expected. IHS/Markit noted both output and new orders "broadly stagnate" while purchasing activity falls "for first time in 2-years."

- French July Manufacturing PMI 53.3 from52.5 – better than 53.1 flash. New export orders drop for the first time since Sep 2016 but business confidence rose and output along with domestic order growth quickened.

- German July Manufacturing PMI 56.9 from 55.9 – weaker than 57.3 flash. IHS/Markit noted July still signals "sharp improvement in operating conditions" and "output growth accelerating" to a 3-month high. While input price inflation was the "weakest since April but marked overall.”

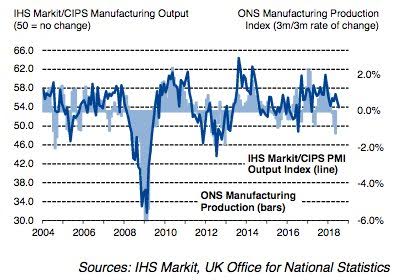

- UK July Manufacturing PMI drops to 54 from 54.4 – weaker than 54.2 expected – 3-month lows. Both output and new orders weaken and intermediate goods production "falls for first time in 2-years." IHS also noted, "Price pressures also remained elevated as a strong increase in average input costs led to the steepest rise in selling prices since February."

Market Recap:

Equities: The US S&P500 futures are off 0.09% after a 0.49% gain – and despite an Apple, earnings beat. The Stoxx Europe 600 is off 0.2% with Macron winning confidence vote and UK Brexit/May headlines driving. The MSCI Asia Pacific fell 0.2% despite Japan gaining post BOJ as US/China trade war fears rise.

- Japan Nikkei up 0.86% to 22,746.70

- Korea Kospi up 0.51% to 2,307.07

- Hong Kong Hang Seng off 0.85% to 28,340.74

- China Shanghai Composite off 1.81% to 2,824.21

- Australia ASX off 0.06% to 6,362.10

- India NSE50 off 0.09% to 11,346.20

- UK FTSE so far off 1.3% to 7,647

- German DAX so far off 0.3% to 12,769

- French CAC40 so far off 0.1% to 5,507

- Italian FTSE so far off 0.7% to 22,053

Fixed Income: Curve steepening of bonds follows Japan overnight – with BOJ widening band moving EU bonds at the open along with supply but slightly weaker global PMIs hold markets into FOMC and US data. UK 10Y Gilt yields up 4bps to 1.37%, German Bunds up 3bps to 0.47%, French OATs up 4bps to 0.77% while periphery mixed – Italy up 4bps to 2.755%, Spain up 4bps to 1.43%, Portugal up 3.5bps to 1.755%, Greece flat at 3.91%.

- Germany sold E2.373bn of 10Y 0.25% Aug 2028 Bunds at 0.47% with 1.4 cover – previously 0.36% with 1.3 cover – after Bundesbank holdings cover 1.8 from 1.6 previously.

- Greece sold E812.5mn of 26-week Feb 1 T-Bills at 0.85% with 1.52 cover – previously 0.85% with 1.38 cover.

- US Bonds are lower with bear steepening, reflecting BOJ steepening, FOMC nerves – 2Y flat at 2.67%, 5Y up 1.4bps to 2.862%, 10Y up 2bps to 2.98%, 30Y up 2.7bs to 3.109%.

- Japan JGBs drop as investors want to test BOJ new band, waiting for 10Y sale tomorrow – 10Y up 6bps to 0.12% - highest since Feb 2017 with 0.20% and speed of change key for BOJ intervention. The BOJ kept the buying unchanged in 1-3 year at Y250bn and 3-5 year at Y300bn but offer to cover ratio of the 1-3 year bucket ticked up to 3.77 from 3.35, while the 3-5 year bucket's offer to cover ratio rose to 3.01 from 1.93.

- Australian bonds track Japan lower in bear steepener after weak auction – 3Y up 2bps to 2.101%, 10Y up 4bps to 2.688% - AOFM sold A$1bn of 11Y 2.75% Nov 2029 TB154 bonds at 2.7136% with 2.88 cover – previously 2.6094% and 3.46 cover from July 4th.

- China PBOC skips open market operations, net drains CNY20bn on the day. Money market rates are lower with O/N off 4bps to 2% while 7-day off 5bps to 2.57%. 12-month swap rates are flat at 2.78 while 10-year bond yields are off 1bps to 3.48% - back to July 19 lows.

Foreign Exchange: The US dollar index is up 0.2%to 94.57. In Asia EM FX mostly flat – TWD flat at 30.616, INR flat at 68.567 after RBI hikes 25bps, KRW off 0.15% to 1121 – touched 1113 on BOK hawkish minutes. In EMEA USD is bid, RUB off 0.35% to 62.677 – tracking oil, ZAR off 0.1% to 13.247, TRY off 0.1% to 4.9240.

- EUR: 1.1685 flat. Range 1.1672-1.1691 – stuck with 1.1650-1.1720 still – hoping FOMC matter with range 1.1575-1.1780 more a prison.

- JPY: 111.85 flat. Range 111.71-111.86 with EUR/JPY 130.75 flat. BOJ still driving with 112 and 113 next big levels – equities key.

- GBP: 1.3135 up 0.15%. Range 1.3096-1.3138 with EUR/GBP .8895 off 0.15%. Bounce on Brexit hopes, BOE hike views with 1.30-1.33 key still.

- AUD: .7420 off 0.10%. Range .7401-.7429 with NZD .3805 off 0.1% - jobs in NZ and China stories/metals driving. Still stuck with .73-.75 A$ key.

- CAD: 1.3015 flat. Range 1.3006-1.3033 – with NAFTA hopes back on key but FOMC/Oil and more China fears counter 1.2980-1.3150 keys.

- CHF: .9910 up 0.1%. Range .9900-.9914 with EUR/CHF 1.1580 up 0.1% - stuck with .9880-1.0020 keys.

- CNY: 6.8293 fixed 0.19% weaker from 6.8165 yesterday. CNY fell early on Trump tariff talk to 6.8338, then recovers to 6.7878, now flat 6.8140. CNH fell 0.6% to 6.8462 – now 6.81 off 0.1%.

Commodities: Oil lower, gold lower, copper off 2.4% to $2.7780.

- Oil: $68.08 off 1%. Range $67.89-$68.52. API reported a surprise crude build puts EIA report into spotlight today with 2.3mn draw expected. WTI watching $67.50 against $68.50 resistance. Brent off 1.1% to $73.38 with $72.50 key against $74.20 resistance.

- Gold: $1223.45 off 0.05%. Range $1219-$1224. The failure to break $1225 despite US/China trade reflects FOMC fears and that is key for today. Silver off 0.3% to $15.473, Platinum off 1.25% to $828.10 and Palladium off 0.8% to $927.10 – trade fears hitting here.

Conclusions: Does the FOMC today really matter? The September hike is over 80% priced into the market. The data on growth support a hike but inflation is modest and much more than 2-3 more hikes seems to depend on the present mood continuing even as outlooks are less rosy. This is the problem for the FOMC and one that will be watched with the FOMC statement and their balance of risks.

Economic Calendar:

- 0815 am US July ADP employment change 177k p 185k e

- 0930 am Canada July RBC Manufacturing PMI 57.1p 57.5e

- 0945 am US July Manufacturing PMI 55.4p 55.5e

- 1000 am US July ISM Manufacturing 60.2p 59.5e

- 1000 am US June construction spending (m/m) 0.4%p 0.3%e

- 1030 am US weekly EIA crude oil stocks -6.147mb p -0.15mb e

- 0200 pm FOMC rate decision – no change expected / press conference

- 0330 pm US July total vehicle sales 17.47mn p 17.10mn e

- 0500 pm Brazil Central Bank Rate decision – no change from 6.5% expected.

Comments

Log in or sign up to join the conversation.