The last-minute deal between the US/Mexico and Canada preserves NAFTA with a new name USMCA. The deal revises rules surrounding automobiles, the dairy sector and intellectual property, but does not resolve end the controversy surrounding US tariffs on steel and aluminium. Both CAD and MXN are stronger against the USD this morning.

The markets are trading with a pocketful of hope that trade negotiations and Trump tweets are noise, leaving markets to believe in global growth and stability. Economic data now matters to the path forward as the uncertainty of monetary policy rests on the central bankers’ response function to surprises, less tweets and elections.

Witness the move up in Korean rates as the PMI report rises and the labor component at 5 ½ year highs sets up speculation for BOK rate hike. The Japan Tankan drop in sentiment was offset by the rise in Capex leaving the BOJ time to do nothing, with focus on the longer-end buying games into tomorrow’s 10-year JGB sale.For Europe, the PMI reports aren’t weak enough to offset the ECB plans on QE end and so the EUR holds but rates are higher. On the other hand, politics remain front and center in Europe though their effect on FX and bonds seems more limited. 1) Italy. 2Y BTPs sold off moving from 1.05% to 1.11% on a report in La Republica suggesting that the EU Commission will reject Italy's budget proposal in November has further fueled uncertainty over the budget. 2) UK. Tories continue to split over Brexit while UK PM May continues to push her negotiations. Her speech Oct 3 maybe a key market event.

Gilts open lower, GBP holds with better PMI.This leaves today to the US political mood and the US economic data with a balancing act in between. The mood for risk is high and so few expect much to derail the rush to new highs for equities in the US. There is a pesky risk barometer out there to consider – the rise of oil to $83 in Brent opens questions of whether this is a tax on global consumer demand. Throw in the weather shift and risks to NatGas prices in Europe thanks to US/EU sanctions on Russia and you have the makings for trouble in energy prices driving up inflation and leaving less room for growth. We have seen this story before and it doesn’t end well. The energy producers are usually winners when oil is higher – and this shows up in CAD, NOK and RUB particularly. But taking out the NAFTA noise it’s interesting to chart the RUB today and think through whether the oil gains are reaching a tipping point for trouble. Watching 66 for such a signal but expecting momentum on oil and risk to lead us to 61.50.

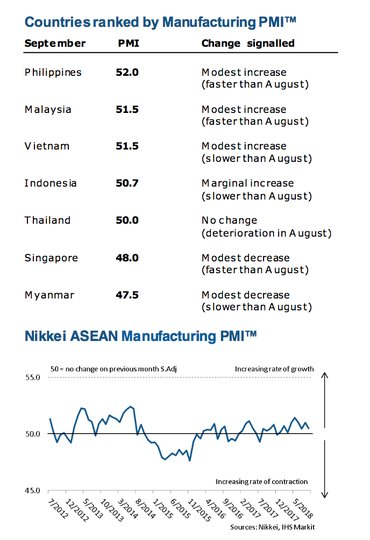

Question for the Day: Is Asia slowing? Short answer yes – but how much matters. The focus on US/China trade tariffs and their spill over into Asia won’t go away. The hope trade rests on the Canada deal overnight leading to more for Europe and Japan. The reality is that the China/US talks are sidelined and that neither side thinks they will lose if they wait it out. The biggest loser is the ASEAN Manufacturing area as they reflect the overall global trade relationship between the two. The headline ASEA Manufacturing September PMI fell to 50.5 from 51 – this puts 3Q PMI average at 50.6 down from 51.2 in 2Q. In September both output and new orders slowed with exports declining even further. The role of FX declines in helping offset economic woes and rebalance maybe something to focus on as the Philippines topped the rankings in September while Indonesia drops down to 4th place.

What Happened?

- Australian September AIG Manufacturing PMI 59 from 56.7 – better than 56.4 expected. The input prices touch the highest since March 2011. New orders rise 3 to 62.6 – best since March.

- Japan September final Manufacturing PMI 52.5 from 52.5 – weaker than 52.9 flash. The 3Q average at 52.4 was below 1Q and 2Q. Further increases in sales and new orders helped to offset export weakness. Overall confidence 12M forward rose but at the slowest pace since November 2016.

- Japan 3Q Tankan Large Manufacturing 19 from 21 – weaker than 22 expected. The outlook for December 22. The large non-Manufacturing (Services) index 22 from 24 – as expected. The small manufacturing 14 from 14 – slightly better than 13 expected – while the small non-manufacturing 10 from 8 – also better than 6 expected. JPY expectations were 107.4 from 107.26 – well below the 114 trading today. The Capex plans for Large Firms 13.4% from 13.6% - less than 14.2% expected – while small firm plans -8.4% from -5.4%, but for all firms Capex 8.5% from 7.9%.

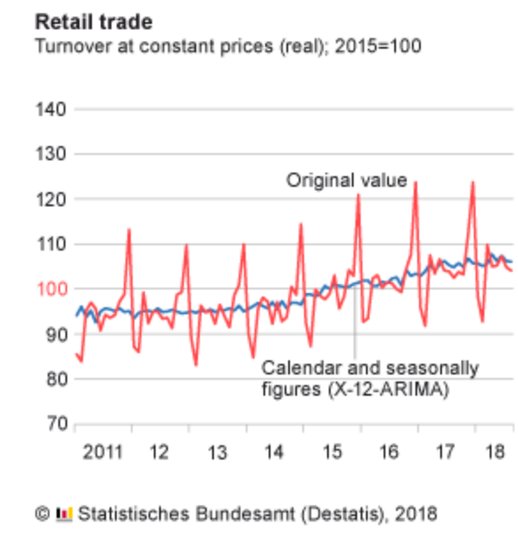

- German August retail sales -0.1% m/m, +1.6% y/y after revised -1.1% m/m (was -0.4%) – weaker than +0.4% m/m bounce expected.The 3Q retail sales now up 0.1% q/q after 0.9% in 2Q. The 3M moving average 0% after -0.5% in July.

- Swiss August retail sales +0.3% m/m, 0.4% y/y after -0.3% y/y – as weaker than 1.7% y/y expected. This follows the September decline which was the first in 4 months.

- Spanish August retail sales +0.3% y/y after -0.4% y/y – better than -0.9% y/y expected.

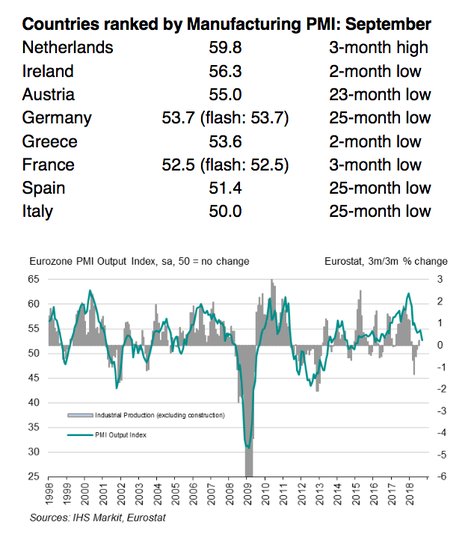

Eurozone September final Manufacturing PMI 53.2 from 54.6 – weaker than 53.3 flash. This is the lowest growth in nearly 2-years with jobs and production slowing. Global trade concerns push confidence down to 3-year lows. Exports rise only slightly slowing overall orders and production.

- Spanish Manufacturing PMI 51.4 from 53 – weaker than 52.6 expected

- Italy Manufacturing PMI 50 from 50.1 – weaker than 50.5 expected

- French final Manufacturing PMI 52.5 from 53.5 – same as flash

- German final Manufacturing PMI 53.7 from 55.9 – same as flash

- UK September Manufacturing PMI 53.8 from revised 53 – as expected. August revised from 52.8. Modest recovery with domestic demand stronger and increased orders from North America and Europe. Input and output cost also increase. However, IHS notes this level of PMI suggests only modest output and exports of intermediate goods had their worst quarter in 3-years, suggesting UK is becoming less of a component supplier.

- UK August mortgage approvals rise to 66,440 from 65l,156 – more than 64,500 expected – highest in 7-months. The UK Consumer Credit rose to GBP1.118bn from GBP838mn – near expectations – but still below the 6-month GBP1.3bn average as “other loans” remains sluggish. Net mortgage lending slowed to GBP2.904bn from GBP2.97bn. The BOE M4-ex financials was up 0.3%m/m and 0.9% 3M y/y.

- Eurozone August unemployment rate 8.1% from 8.2% - better than 8.2% expected – best since November 2008. The youth unemployment rate also dipped to 16.6% from 16.7%. There were 13.22mn unemployed in the Eurozone and 16.657mn in the EU28. Czech led with 2.5% unemployment followed by Germany and Poland both at 3.4%.

Market Recap:

Equities: The S&P500 futures are up 0.6% - best in a week – after a 0% outcome Friday. The Stoxx Europe 600 is up 0.4% with Italy leading, while the MSCI Asia Pacific was up 0.2% but Japan saw its Nikkei 225 at 27-year highs. The MSCI EM and World indices are both up 0.1%.

- Japan Nikkei up 0.52% to 24,245.76

- Korea Kospi off 0.18% to 2,338.88

- Hong Kong Hang Seng closed for holiday

- China Shanghai Composite closed for holiday

- Australia ASX off 0.52% to 6,292.70

- India NSE50 up 0.71% to 11,008.30

- UK FTSE so far up 0.1% to 7,517

- German DAX so far up 0.6% to 12,318

- French CAC40 so far up 0.25% to 5,508

- Italian FTSE so far up 1.45% to 21,011

Fixed Income: US bonds go into steepener mode after NAFTA deal, JGBs stuck in dull range with eye on longer end and BOJ noise, Bunds sell off and curve steepen along with French OATs. BTPs bounce with headlines on budget and reactions driving.UK 10-year Gilts up 2bps to 1.59%, German Bunds up 2.5bps to 0.495%, French OATs up 3 to 0.83%. The perhiphery – Italy up 2.5bps to 3.16%, Spain up 1.5bps to 1.51%,Portual up 1bps to 1.875%, Greece up 1.5bps to 4.135%.

- US Bonds see selling and curve steeper after NAFTA deal, equity bounce – 2Y up 1.2bps to 2.831%, 5Y up 2bps to 2.973%, 10Y up 2.5bp to 3.085%, and 30Y up 3bps to 3.235%

- Japan JGBs hold ranges into 10Y sale, with weaker Tankan, long-end focus – 2Y -0.125% up 0.4bps, 5Y up 0.3bps to -0.075%, 10Y up 0.7bps to 0.124%, 30Y up 2.2bps to 0.92%.

- Australian bonds have quiet start with NSW holiday and NAFTA/China PMI focus – 3Y flat 2.046%, 10Y flat at 2.665% - RBA next key

Foreign Exchange: The US dollar index is flat at 95.11 with a 95.05-95.32 range – focus is on CAD and MXN post NAFTA. In Emerging Markets – EMEA mostly USD offered: ZAR up 0.4% to 14.083, TRY up 2.2% to 5.92 and RUB off 0.1% to 65.60; ASIA mostly USD bid: TWD flat at 30.52, KRW off 0.2% to 1111.50 and INR off 0.5% to 72.86

- EUR: 1.1610 up 0.05%. Range 1.1574-1.1628 with focus on Italy, rates, 1.1550 holding for 1.1680 resistance.

- JPY: 114.00 up 0.25%. Range 113.59-114.05 with 114 barrier gone 115 next. EUR/JPY 132.30 up 0.25% - watching 133.50 next.

- GBP: 1.3040 up 0.1%. Range 1.3019-1.3061 with EUR/GBP .8900 flat. Market watching Tory conference and data divergence with EU. 1.29-1.32 keys.

- AUD: .7220 off 0.1%. Range .7207-.7232 with RBA key and .7250-80 resistance. NZD .6605 off 0.2% - waiting with A$ reflects weaker China outlook

- CAD: 1.2790 off 0.9%. Range 1.2787-1.2887 with NAFTA deal triggering stops at 1.2880 with 1.2550 next big target 1.2750 minor. Oil/BOC vs. rates/crosses.

- CHF: .9825 up 0.1%. Range .9847-.9792 with EUR/CHF 1.1405 with Italy neutralized and weaker data driving marginal cross with 1.1450 key.

Commodities: Oil up, Gold down, Copper down 1% to $2.7985

- Oil: $73.42 up 0.25%. Range $73.25-$73.65. Brent up 0.3% to $82.99. Focus is on Iran/Venezuela supply hits and some doubts post Baker Hughes on US production. WTI watching $79 for technical target against $70 base. Brent watching $87 target against $80 support.

- Gold: $1186.25 off 0.4%. Range $1185.50-$1193. Gold stuck in bearish consolidation with 55-day now $1204.50 and support at Aug 16 lows $1160.40 with $1182 pivot. Silver $14.56 off 0.65% - watching $14.801 the 55-day against $14.50 pivot and $14.18 Sep 27 lows. Platinum off 0.5% to $812 and Palladium off 1.65% to $1057.25.

Conclusions: Does the middle class matter?Interesting to read the World Data lab report last week that Brookings and the FT picked up on. The global middle class is now about 3.6bn people or nearly half the world’s population. The World Data Lab defines middle class as someone earning between $11 and $110 per day, on a 2011 purchasing power parity basis, a benchmark used by many organizations and governments, including India and Mexico. It concluded earlier this month that 3.59bn people make up the global middle class, and forecast that the group would grow to 5.3bn by 2030. This has some far-reaching implications. The politics behind the middle class are complicated. First rule for leaders, don’t give people a taste of richness and then take it away. This is a risk in Asia where most of those new middle class joiners are found. The relationship of the US to Asia and its role with trade and finances matters and with China on holiday all week, expect less worry about the US/China trade and more about politics. One point for the US is that the rise of middle class outside the US puts the US middle class off – as it questions American exceptionalism.

Economic Calendar:

- 0900 am Atlanta Fed Bostic Speech

- 0930 am Canada September RBC Manufacturing PMI 56.8p 56.6e

- 0945 am US September final Manufacturing PMI 54.7p 55.4e

- 1000 am US September Manufacturing ISM 61.3p 60.5e / prices paid 72.1p 70.8e

- 1000 am US August Construction Spending 0.1%p 0.5%e

- 1215 am Boston Fed Rosengren Speech

Comments

Log in or sign up to join the conversation.