End of the Summer and there are no do-overs as Europe gets back to work and starts to think about the lessons learned and apply them for an Autumnal risk-rally. The problem remains one around politics and emerging markets.

This week will focus still on Trump trade policy and how it plays out in Canada and Europe. Overnight stability in the CNY helped bring a bit of relief that China isn’t taking the bait and playing tit-for-tat with the US even as $200bn more in tariffs loom large. However, FX markets continued to show volatility, G10 focus was on GBP weakness. UK Brexit concerns dominated GBP today with UK PM May under further political pressure, her Telegraph editorial suggested no second referendum and no compromise to the Chequers plan which EU Barnier strongly opposed over the weekend. The AUD fell to 20-month lows with weaker retail sales. The EUR stuck in weaker part of range with Italy PMI at 2-year lows. But, Fitch affirmed Italy’s BBB rating Friday, while downgrading the outlook to negative, and Salvini offered that Italy’s budget with “touch” the 3% EU budget deficit limit but won’t break it. BTPs are bid and pressure on EU shares reversed. TRY stabilized after the CBRT vowed to take necessary actions to support price stability and said policy will be adjusted in the September meeting. This followed the 17.9% y/y inflation for August – showing TRY weakness driving prices.

Argentina is waiting for a new fiscal plan today and hopes for more flexibility from IMF. The world seems a dangerous place and one where the economic data today reveals the cracks in optimism despite solid growth as both Asia and European PMI reports sag a bit and outlooks dive. The focus today is on the GBP which is the big mover while the shift tomorrow maybe back to the commodity currencies with the RBA and BOC decisions looming this week.

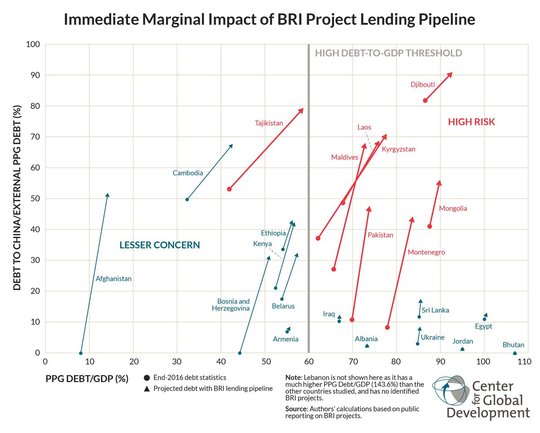

Question for the Day: What is the risk for debt from China’s Belt and Road push? Chinese President Xi opened the China-Africa forum today. There were a few key takeaways from his address all of which seems pointed at US trade policy disputes. 1) China insists on “win-win” relations with nations in the fight against protectionism and unilateralism. 2) China promises to further open-up to the rest of the world, as isolations means “no future” for any country. 3) China aims to develop relationship with global partners on a path of fairness and mutual respect. The key push was to deepen cooperation with African nations in the One Belt and Road Initiative.

Whether China succeeds to change the world order and rise to super power status equal to the US rests on whether this OBRI plan succeeds in driving real growth outside of China.The chart from Center for Global Development and its blog on the subject are worth reading today as the key issue for September remains what happens to EM as investors balance value and buying this dip against further fears of debt deleveraging and catching the falling knife of asset sales and FX turmoil.

What Happened?

- New Zealand 2Q Terms of Trade rose 0.6% q/q after -2% q/q - less than +1.0% q/q expected. Total export prices rose 2.4% due to rise in dairy, meat and wool prices. Dairy prices rose 3.2% due to a 5.2% rise in volumes and a 7.6% rise in values. Meat prices rose 3.6% due mainly to 5.4% rise in lamb prices. Meat volumes rose

4.7% and values rose 3.7%. Wool prices rose 4.0% as a 1.2% rise in values offset the 2.1% decline in volumes. Total import prices rose 1.7% due mainly to rise in petroleum and petroleum product prices. Crude oil prices rose 14% but volumes fell 35% and values fell 26%. The services terms of trade fell 5.8%, after around 6.0% rise in Q1. Export prices for services fell 1.9% and import prices rose 4.2%. - Australia July retail sales 0% m/m after 0.4% m/m – weaker than 0.2% m/m expected. In trend terms, all categories of retail sales were up in July except household goods retailing which was flat both in July and June. The latest outcome was due to slowing in all categories of retail sales, except other retailing which rose 1.7% in July versus a 0.2% rise in June. Household goods retailing fell 1.2%, marking the biggest fall since the 2.8% drop in December last year. Department stores continued their weak trend, down 1.9% in July and has declined for five out of the last seven months this year. Food categories slowed in July, with food retailing up 0.3% versus a 0.4%

rise in June, and food services up 0.6% after a 0.8% rise. - Australia August AIG Manufacturing PMI rises to 56.7 from 52 – better than 52.1 expected. All 7 activity indices expanded. Sales rose 15.2 to 60.7 – though some of this maybe weather related due to destocking of some agricultural products. New Orders rose 8.5 to 59.6. Exports rebounded up 8.5 to 58.4. Prices rose sharply – input prices up 9.3 to 77.4 – most since Mar 2011, while selling prices rose 5.1 to 58.1 most since April 2017. The drought caused some of the price pressures particularly food and beverages. The weaker A$ helped export orders. Wages rose 4.1 to 64.7

- Australia 2Q business inventories up 0.6% q/q after 08% q/q - more than 0.3% q/q expected. 1Q revised higher from 0.7% q/q. This helps 2Q GDP as inventories are unlikely to subtract from growth. Corporate profits rose 2% q/q after 6.5% q/q – better than 1.3% q/q expected.1Q revised from 5.9% rise. Mining profits rose 4.4% q/q in Q2 compared with a 12.2% rise in Q2. Retail profits rose 1.5% after a 6.0% rise. Construction profits unexpectedly declined in Q2, down 5.3%, but this followed a strong 11.8% jump in Q1. Wages and salaries rose 1.2% q/q from 0.9% revised in 1Q.

- Japan 2Q Capital Spending jumps 12.8% y/y from 1Q 3.4% y/y – more than 6.6% y/y expected – best in a decade.The seasonally adjusted ex-software spending was 6.9% q/q, 14% y/y after 0.8% q/q, 2.1% y/y. Manufacturing was 19.8% from 2.8% y/y. Investment in equipment was backed by solid global and domestic demand as well as the need to cope with labor shortages in April-June, when the U.S.-China trade dispute had little direct impact on Japanese exports or production Services 9.2% from 3.6% y/y – most since 2Q 2017. This overall report will lead to 2Q GDP revisions.

- Japan August final Manufacturing PMI 52.5 from 52.3 – same as flash.Production rose with faster new order growth but export orders drop. Sentiment hit on geopolitical fears – with the outlook at 21-month lows.

- Korea August Manufacturing PMI 49.9 from 48.3 – slightly worse than 50.2 bounce expected. Conditions failed to improve for the 6th month in a row, but new orders and employment rose while output inflation eased. Outlook for production improved.

- China August Caixin Manufacturing PMI 50.6 from 50.8 – as expected – 14-month lows. Production increased at the best rate since January even while demand eased. New business rose at the slowest rate in 15-months with weaker foreign demand notable. Export sales fell for the 5th month.

- Swiss July retail sales -1.0% m/m, -0.3% y/y after +0.3% y/y – weaker than 0.0% expected.

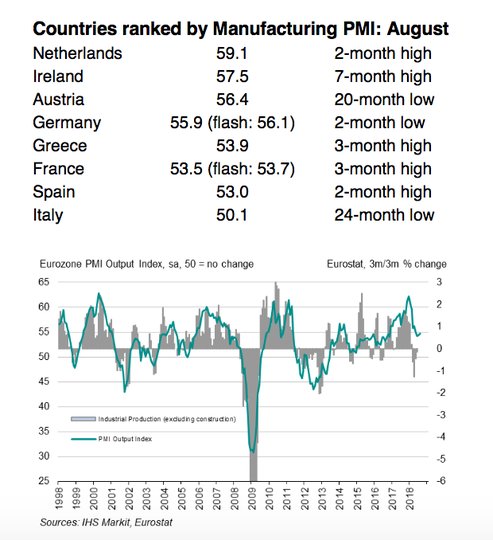

Eurozone August final Manufacturing PMI 54.6 from 55.1 – same as flash. Output growth was better, but new orders slow to 2-year lows as tariffs and global trade fears hit confidence. Markit noted, “prospects dimmed further as growth of new orders hit a two-year low and worries about the outlook deepened... One positive was a cooling of price pressures, which fed through to the smallest rise in factory selling prices for a year and could help bring consumer inflation down in coming months.”

- Italy Manufacturing PMI 50.1 from 51.5 – weaker than 51.1 expected

- French final Manufacturing PMI 53.5 from 53.3 – weaker than 53.7 flash

- German final Manufacturing PMI 55.9 from 56.9 – weaker than 56.1 flash

- Spanish Manufacturing PMI 53.0 from 52.9 – better than 52.5 expected

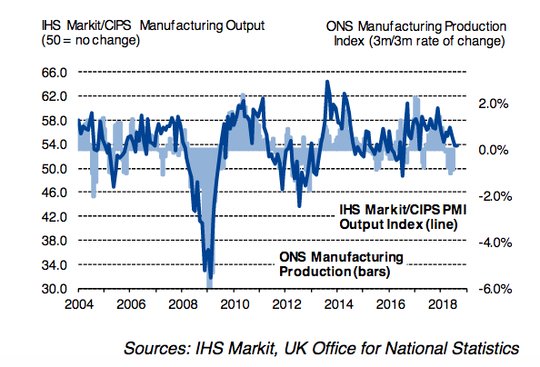

- UK August CIPS Manufacturing PMI 52.8 from 53.8 – weaker than 53.8 expected – 25-month lows.Job creation near stagnation while business optimism slips to 22-month lows. New export orders contract – first time since April 2016.

Market Recap:

Equities: The US S&P500 futures are up 0.25% after 0.01% gains Friday – with markets closed today. Stoxx Europe 600 is up 0.1% with trade focus – energy shares lead offset by autos and construction. The MSCI Asia Pacific fell 0.5% while the MSCI EM is off 0.2% and the MSCI World index is off 0.2% to 1-week lows.

- Japan Nikkei off 0.69% to 22,707.38

- Korea Kospi up 0.85% to 2,307.03

- Hong Kong Hang Seng off 0.63% to 27,712.54

- China Shanghai Composite off 0.17% to 2,720.74

- Australia ASX off 0.18% to 6,416.50

- India NSE50 off 0.84% to 11,582.35

- UK FTSE so far up 0.85% to 7,497

- German DAX so far off 0.2% to 12,337

- French CAC40 so far off 0.05% to 5,405

- Italian FTSE so far up 0.15% to 20,297

Fixed Income: Core EU bonds are offered with turnabout in risk mood in morning despite weaker Italy data as hope for budget rises and spreads in periphery snap back down. German 10-year Bund yields up 1.5bps to 0.34%, France up 1.2bps to 0.69% while UK Gilts are flat at 1.425%.The periphery is bid – Italy off 6.5bps to 3.16%, Spain off 1.5bps to 1.45%, Portugal off 1.5bps to 1.895% and Greece the exception up 3bps to 4.36%.

- The Netherlands sold E1.69bn of new 6M Feb 2019 DTC at -0.62% with 1.45 cover.

- US Bonds are closed for Labor Day

- Japan JGBs sold after BOJ plan changes, ignoring Kuroda. 5Y up 1bps to -0.076%, 10Y yields up 1.5bps to 0.122%, 30Y up 0.7bps to 0.845%.

- Australian bonds see modest profit taking despite retail sales, focus shifts to RBA, C/A, more growth data – 3Y off 1bps to 1.965%, 10Y flat at 2.515%.

- China PBOC skips open market operations for 9th day, leaves liquidity neutral, but money market rates are higher with O/N up 2.5bps to 2.28% and 7-day up 1.5bps to 2.616%. 10-year bond yields rose 1bps to 3.595%.

Foreign Exchange: The US dollar index is flat at to 95.11 after trading 95.22 highs in Asia and back to 95 lows in Europe with focus on 94.95 and 95.52 consolidation. In Emerging Market FX, USD mostly bid - EMEA is USD bid: ZAR off 0.95% to 14.83, TRY off 1.2% to 6.6150 – touched 6.7325 on inflation – RUB off 0.75% to 67.99. ASIA is USD mixed: INR off 0.1% to 71.06, KRW up 0.25% to 1110.50 from 1117.80 highs, TWD flat at 30.712.

- EUR: 1.1615 up 0.1%. Range 1.1588-1.1626 with PMIs slightly weaker but Italy less scary and same with TRY and ARS driving – focus is on 1.1550-1.1725 consolidation

- JPY: 111.10 up 0.1%. Range 110.85-111.19 with early $ selling reversed with CNY stability and with equities in Europe. EUR/JPY 129.00 up 0.1% watching 128-130 consolidation.

- GBP: 1.2885 off 0.55%. Range 1.2864-1.2967 with Brexit headlines driving 1.29 break opens 1.2750 restest and 1.30 resistance. EUR/GBP .9010 up 0.6% with .8950-.9050 keys.

- AUD: .7210 up 0.3%. Range .7166-.7218 with A$ sold on retail sales, China trade fears rebounds into RBA and tracks CNY and other crosses. NZD off 0.15% to .6610 with .6540 key.

- CAD: 1.3050 up 0.1%. Range 1.3045-1.3079 with Trump weekend comments on Canada opening fears of no deal but 1.30-1.32 holding with oil, rates and crosses key.

- CHF: .9695 up 0.1%. Range .9685-.9707 with less Italy fears, cross relief – EUR/CHF 1.1260 up 0.15% with 1.12-1.14 key.

- CNY: 6.8347 fixed 0.15% weaker from 6.8246, but trades up 0.2% to 6.8165 at the close from Friday. The EUR/CNY holds below 8 at 7.9240. CNH focus is on 6.8275-6.8400 consolidation. The CFETS RMB index rose 0.33% to 93.08 after 2 weeks of losses, but its still down 1.87% from start of year at 94.85

Commodities: Oil up, Gold down, Copper up 0.1% to $2.7155.

- Oil: $69.90 up 0.15%. Range $63.53-$70.00. WTI watching $68 as the pivot for $71.05 July 10 highs or $63.89 Aug 16 low. Brent $78.03 up 0.5% - watching $74.71 – 55-day m.a. against $78.65 trend resistance. Weekend news showed Iraq and Russia crude exports up in August.

- Gold: $1201.50 off 0.2%. Range $1200-$1204. Stronger USD, but more trade doubts and political fears. Silver $14.52 off 0.15% - watching $13.984 Aug 26 lows against $14.87 20-day m.a. Platinum flat at $788.05, Palladium up 0.2% to $984.75.

Conclusions: What is the best game plan? US and Canada Labor Day Holidays are usually a time to sit back and think through a game plan for the month. The view that August with its surprise uptick for US and Asia shares continues seems to be winning the consensus. Expect today’s price action and list of worries to remain the guiding lights with focus on Italy budget, UK Brexit, Argentina fiscal plan and IMF, Turkey inflation and CBRT, China/US trade deals, US talks with Canada and Europe on trade, US politics into the mid-term November vote – all these are going to drive positioning as money managers steer between the risk and the rewards of each.Carry and value are competing with growth and momentum. The biggest problem for September maybe in the no-do over rules for returns as any mistake in active management loses out to a grinding passive return strategy – as many have seen over the summer.

Comments

Log in or sign up to join the conversation.