Almost a year since winning the elections, the US President Donald Trump is yet to make good on his election promises. Battling an administration that has seen a constant reshuffling of portfolios, last week saw the Trump administration invoke the tax reform proposals once again.

Once, a topic of cheer for the financial markets and one that saw a strong rally in the US equity indices and the US dollar, the markets this week brushed aside the news. Although there was some initial reaction to the proposed tax reform plans, the markets were largely muted.

This was in stark contrast to the previous such announcements when the US dollar posted a strong rally.

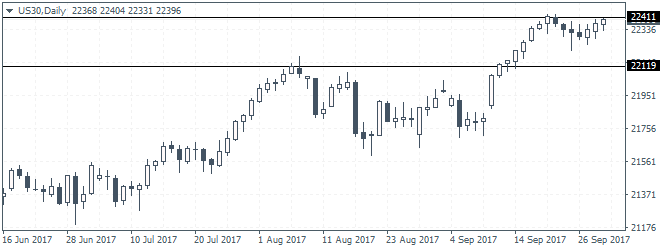

(Click on image to enlarge)

Dow 30: Range bound

Trump’s Tax Reforms: Unrealistic

President Trump's tax reforms are seen by many as being ambitious, aims to simplify, as well as lower taxes for both households and corporate sectors. The statutory tax rate for the corporate sector is expected to be reduced to 20% from the current 30%.

However, this is expected to come at the cost of rising deficit which is expected to put both the Democrats and some Republicans in direct opposition to the plans. Furthermore, Trump's proposal of signing this into law by the end of the year is also seen by many as a highly unrealistic.

The US Committee for Responsible Federal Budget estimated that Trump's proposed reforms will require about $5.8 trillion in tax cuts in a decade and would also require $3.6 trillion in setting aside provision to raise revenue. Combined, this is expected to post a net uc ot $2.2 trillion.

Investors still remember the proposed healthcare reform plans that turned out to be a debacle for the Trump administration. After the initial euphoria, the sentiment in the US dollar turned lower. This was for a number of reasons; starting with the constant controversies that hit Washington, to a downturn in the economy.

While sentiment in USD declines, ECB set to take a hawkish path

Even inflation, which at one point threatened to overshoot the Fed's 2% target rate also slowed down significantly.

Latest inflation statistics put the headline consumer prices close to 1.6%, still a far way off from the Fed's target rate. The FOMC officials have also remained on the sidelines, for the most part, this year. The latest hurricanes that hit the US in September is expected to have some kind of an impact on the short growth and inflation prospects.

September’s nonfarm payrolls are already projected to rise only 88k on account of the natural disasters.

This evidently led to the markets unwinding the long positions in the US dollar, and preference grew for the euro which has been backed by strong economic performance in the region. Despite starting the year on shaky grounds, the Eurozone's economy and the political landscape managed to stabilize.

Eurozone outlook improves

Recently concluded German elections showed that the CDU/CSU party, led by Chancellor Angela Merkel won another term as widely expected. The fact that the rise of the fringe parties in Europe has been trending is another question.

However, with most of the political headwinds now a thing of the past, the focus is likely to turn to the economic policies from the ECB. As the markets head into the final quarter of the year, the focus will evidently shift to the US political and economic landscape. Market watchers will be looking to the FOMC, the Trump administration and of course the ECB.

The week ahead will see some preliminary insights especially with the ECB’s monetary policy meeting minutes due for release this week. Investors will be scrutinizing the minutes for any clues for a decisive tapering announce that is expected in October.

Comments

Log in or sign up to join the conversation.