The difference between illusions and delusions may help as market embark into April, seasonally one of the better months for risk assets, but also one filled with the fundamentals doubts that make selling in May so popular. Illusions are external while delusions are internal. You can only have an illusion by distortions of the senses – for markets, this means manipulation and fixings in prices, while delusions in markets are about the psychology of mood, of greed beating fear, all based on false understandings of the fundamentals or misinterpretations of the facts. The allusion to the Lion when we are really just a Tabby Cat seems best on the day where PMI reports underscore the pain of the first quarter and the aspirations for the second – with China back growing but Japan Tankan dropping, Korea exports shrinking and Europe remaining stuck in a downturn with manufacturing at 6-year lows. The HICP from Europe suggests more disinflation despite energy costs and that alone should worry the ECB and investors, but the EUR is higher thanks to the illusions of China reflation with the PMI reports from the NBS and Caixin all showing a robust March and a return to manufacturing employment albeit it from Beijing forced demand. The focus on elections over the weekend also shouldn’t be lost as the Turkey President Erdogan sees setbacks in local elections with Ankara and potentially Istanbul losses fro the AK Party. A comedian with no political experience won the first round in Ukraine while Slovakia elects a woman as a leader and as the UK PM May struggles to hold power with today’s voting key to the Brexit saga. For the FX markets, the 1Q scoreboard was dull in developed markets and painfully predictable in EM with long RUB/short ARS the winner. The real story maybe in the CNY/EUR with CNY up 2.5% and EUR off 2.2% - leaving the US index up 0.5% in 1Q – the relationship of risk-on to growth hopes in China and the EUR remains in play and puts the EUR as the key barometer for the month of ahead. One has to wonder if this rally today is delusion or illusion.

Question for the Day: Is the China bounce lifting the region? This is the critical question but its not simple to answer. While the focus on today will be on global growth recoveries starting with the Chinese NBS and Caixin PMIs, the overall impact on Japan and Korea was modest. The Japan Tankan weakness and Korea trade export fall reflect ongoing issues for growth in Asia. However, the reports from ASEAN Manufacturing PMI reflect a more robust recovery with new orders increasing, output expanding while inflation pressures ease. This is a “Goldilocks” scenario for the region and one that will matter for 2Q should it continue. Domestic demand continues to matter. The Nikkei ASEAN March Manufacturing PMI rose to 50.3 from 49.6– with new orders rising for the first time in 2019, and export orders slowing their fall.

What Happened?

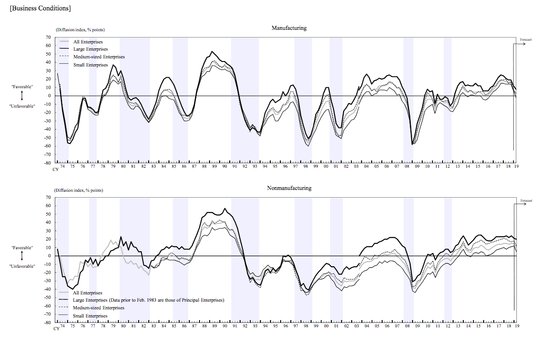

- Japan 1Q Tankan large manufacturing 12 from 19 – weaker than 13 expected with outlook 8 from 15 – also weaker than 12 expected. The medium-sized manufacturing drops to 10 from 7, while small fell to 6 from 14. The large services fell to 21 from 24 – also weaker than 22 expected with outlook unchanged at 20 – as expected. The medium sized services rose to 18 from 17 while small rose to 12 from 11. The all enterprise index fell to 12 from 16 with outlook 7 from 10. For prices output fell to 1 from 6 for large manufacturing while services fell to 7 from 8. Profits for FY2019 estimated fell to -1.3% y/y from -1.9% in manufacturing and -1.3% y/y from -0.9% in services. For all industries profits improved to -0.7% from -1.5% y/y while fixed investments fell -2.8% y/y after +10.4%.

- Japan March final manufacturing PMI 49.2 from 48.9 – better than 48.9 flash – with sluggish demand pushing output lower. Business confidence remains near record lows.

- Korea March trade surplus $5.22bn from $2.96bn – more than $4.9bn expected. Trade fell from $6.41bn in March 2018. The exports fell 8.2% to $47.11bn following -11.1% y/y – near expectations - while imports fell 6.7% to $41.89 bn after - 12.6% y/y – worse than the -4.9% drop expected. The trade surplus for 1Q narrows to $9.47bn from $12.63bn in 2018. Sales of memory chips contracted 16.6%, as global demand for smartphone slowed on low seasonal demand. Also, exports dropped for petrochemicals (-10.7%), amid increased supply from the US. In contrast, sales of ships advanced 5.4%, making it the only category to show improvement. Exports to China shrank 15.5%, the fifth straight month of fall. In addition, sales to Japan declined 12.8%, due to declining demand of semiconductors and steel, while exports to the US rose 4% up for the 6thmonth due mostly to autos and machinery.

- Korea March manufacturing PMI 48.8 from 47.2 – better than 47.7 expected. Production declines as orders continue to fall. Business confidence remains subdued.

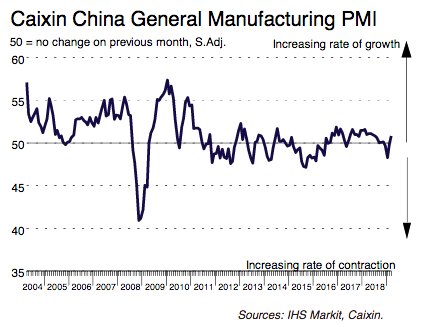

- China March Caixin manufacturing PMI 50.8 from 49.9 – better than 50.1 expected. Employment increased for the first time since Oct 2013. Output and new work increased while inventories climbed and input costs rose. Sentiment 12-month forward rises to 10-month highs. New orders rose to 4-month highs with exports moving to positive.

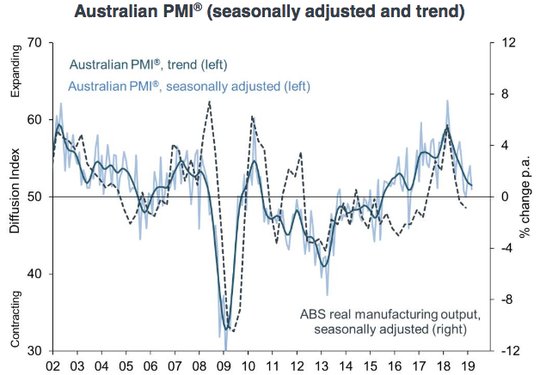

- Australia March AIG manufacturing PMI 51 from 54 – weaker than 53.5 expected. Some delayed orders linked to Federal Election and housing construction weakness. Weaker A$ noted in helping export orders. By category, Food/beverageds up 1.4 to 59, Chemicals -0.8 to 51.3, machinery off 1.7 to 46.1, building materials -2.5 to 44.7, metal products -0.9 to 46.6 while paper, TCF rose 2 to 57.7.

- Australia March final CBA manufacturing PMI 52 from 52.9 – same as flash. Growth was still the softest since July 2016. Lower employment noted while input and output prices rose and business confidence remains positive.

- Australia March NAB business confidence drops to 0 from 2 – weaker than 4 expected. This is the 6thmonth below the 6 average and the lowest since July 2013. House price drops and household spending outlooks cited. Business conditions rose to 7 from 4 – above the 6 long-term average with sales up 4 to 12, profits up 4 to 5 and employment up to 7 from 5.

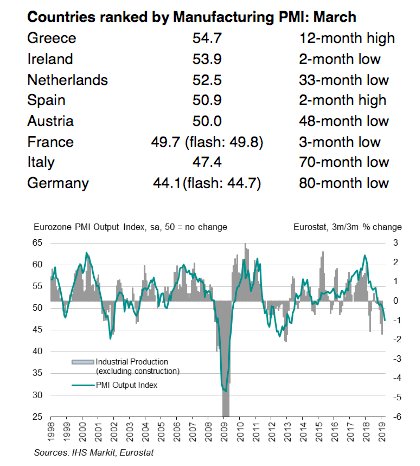

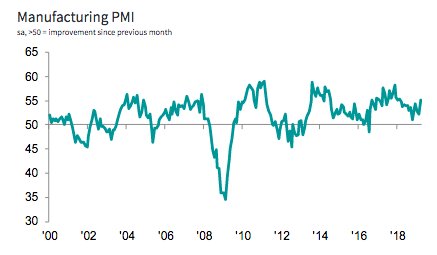

- Eurozone March final manufacturing PMI 47.5 from 49.3 – slightly weaker than 47.6 flash. New orders saw their biggest drop since late 2012 while export orders fell at the worst rate since Aug 2012. Production fell but inventories increased. Confidence fell to 6-year lows. IHS Markits sees manufacturing output falling at 1% in March.

- Spain manufacturing PMI 50.9 from 49.9 – better than 49.6 expected – broad divergence across groups with consumer goods higher, capital goods weaker

- Italy manufacturing PMI 47.4 from 47.7 – as expected – with new orders dropping most in 6 years, output off for 8thmonth.

- France final manufacturing PMI 49.7 from 51.5 – weaker than 49.8 flash – output and new orders contract.

- German final manufacturing PMI 44.1 from 47.6 – weaker than 44.7 flash – 80-month lows

- UK March manufacturing PMI 55.1 from 52.1 – better than 51 expected – 13-month highs. The trends for output, new orders and employment all gained. The build-up of inventories rose to record rates. Overall, Brexit continued to weigh on confidence but optimism edged slightly higher from subdued levels. Much of the increase in March appears to be in preparation for Brexit disruptions according to IHS Markit.

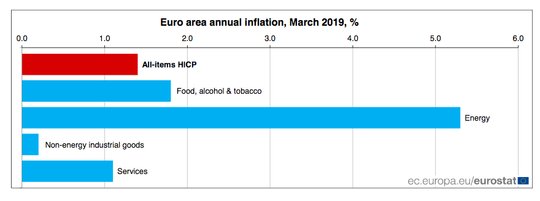

- Eurozone March flash HICP drops to 1.4% y/y from 1.5% y/y – less than the 1.5% y/y expected. The core HICP slips to 0.8% y/y from1.0% y/y – also less than the 0.9% y/y expected. Energy rose 5.3% y/y from 3.6% y/y while Services fell to 1.1% from 1.4% y/y, fresh food fell to 1.2% from 2.9% y/y, processed foods fell to 2.0% from 2.1% y/y, and industrial goods fell to 0.2% from 0.4% y/y.

Market Recap:

Equities: The S&P500 futures are up 0.6% after gaining 0.67% Friday. The Stoxx Europe 600 is up 0.8% holding gains from the open after the MSCI Asia Pacific jumped 1.4% with China leading after PMI reports.

- Japan Nikkei up 1.43% to 21,509.03

- Korea Kospi up 1.29% to 2,168.28

- Hong Kong Hang Seng up 1.76% to 29,562.02

- China Shanghai Composite up 2.58% to 3,170.36

- Australia ASX up 0.61% to 6,299.70

- India NSE50 up 0.22% to 11,649.10

- UK FTSE so far up 0.6% to 7,324

- German DAX so far up 1.2% to 11,669

- French CAC40 so far up 0.7% to 5,387

- Italian FTSE so far up 0.6% to 21,422

Fixed Income: Risk-on means bonds off. Focus is on US while EU bonds hold with lower PMI and lower HICP. German 10-year Bund yields flat at -0.07%, French OATs up 4bps to 0.36%, UK Gilts flat at 1% while periphery mixed with Italy up 1bps to 2.52%, Spain up 1bps to 1.13%, Portugal up 2bps to 1.28% and Greece flat at 3.74%.

- US Bonds are lower, curve flatter with belly focus– 2Y up 4bps to 2.27%, 5Y up 4bps to 2.24%, 10Y up 3bps to 2.44%, 30Y up 1bps to 2.82%.

- Japan JGBs sold with US and China PMI, while Tankan ignored– 2Y up 1bps to -0.17%, 5Y up 1bps to -0.19%, 10Y up 2bps to -0.08%, 30Y up 2bps to 0.52%.

- Australian bonds sold off with China PMI, ignore NAB business confidence ahead of RBA – 3Y up 2bps to 1.43%, 10Y up 3bps to 1.81%, NZ 10Y up 3bps to 1.86%. Australia sold A$700mn of 5.5% 5Y Apr 2023 bonds at 1.4064% with 3.99 cover.

- China bonds bid with focus on Barclays Agg additions driving– 2Y off 3bps to 2.60%, 5Y off 1bps to 2.93%, 10Y off 1bps to 3.13%. The PBOC skips open market operations for 9thday leaves liquidity neutral.

Foreign Exchange: The US dollar index off 0.2% to 97.10. Emerging Markets are mostly USD offered – ASIA: INR off 0.2% to 69.304, KRW up 0.05% to 1135.65; EMEA: ZAR up 1.7% to 14.234, RUB up 0.35% to 65.429 while TRY off 1.1% to 5.603.

- EUR: 1.1235 up 0.15%. Range 1.1220-1.1250 with focus on 1.12-1.1280 for momentum and ECB/FOMC contrast.

- JPY: 111.00 up 0.15%. Range 110.88-111.19 with EUR/JPY 124.75 up 0.35%. All about risk-on and 110-112 still.

- GBP: 1.3090 up 0.45%. Range 1.3009-1.3105 with EUR/GBP .8580 off 0.3% - Brexit and politics still key with 1.30-1.33 holding for now – voting today key.

- AUD: .7115 up 0.35%. Range .7104-.7132 with China PMI pulling up A$ despite weaker NAB confidence and mixed PMIs – NZD .6825 up 0.35%.

- CAD: 1.3360 up 0.1%. Range 1.3338-1.3363 with focus on oil, politics, and crosses. 1.3320-1.3450 keys.

- CHF: .9940 off 0.1%. Range .9935-.9964with EUR/CHF 1.1170 up 0.1% - less fear as equities lead – still .9880 and 1.1180 pivots.

- CNY: 6.7175 off 0.1%. Range with focus on PMI reports and trade talks still. PBOC fixes 6.7193 from 6.7335.

Commodities: Oil up, Gold off, Copper up 0.4% to $2.9540

- Oil: $60.59 up 0.75%.Range $60.13-$60.87 with focus on $60 base for $62.50 next – Brent up 1.25% to $68.44 with $69-$70 key resistance.

- Gold: $1295 off 0.3%.Range $1292.60-$1298.50 with $1302 cap and $1286 support – risk-on move driving. Silver off 0.4% to $15.05, Platinum off 0.3% to $851.40 and Palladium up 0.3% to $1346.30.

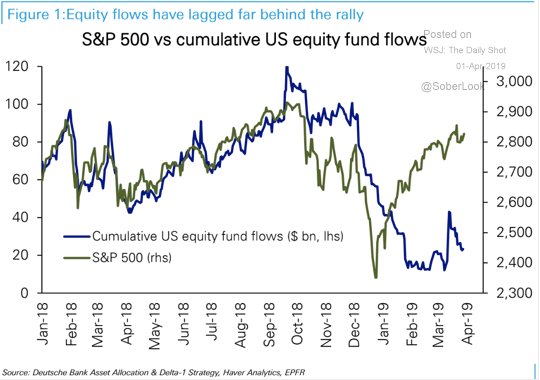

Conclusions: Will momentum prevail?FOMO driving markets in April maybe the next focus – as fear of missing out on better times dominates into this week filled with key US data. The biggest story for the S&P500 isn’t in the 1Q bounce but in the lack of equity fund flows chasing it. The buying for April maybe FOMO related. Expect the balancing act of data against hope for 2Q bounces to be in play as earnings reports start to roll out.

Economic Calendar:

- 0830 am US Feb retail sales (m/m) 0.2%p 0.3%e / ex autos 0.9%p 0.4%e

- 0930 am Canada Mar RBC manufacturing PMI 52.6p 52.8e

- 0945 am US Mar final manufacturing PMI 53p 52.5e

- 1000 am US Mar manufacturing ISM 54.2p 54.5e

- 1000 am US Jan business inventories (m/m) 0.6%p 0.4%e

- 1000 am US Feb construction spending (m/m) 1.3%p -0.3%e

- 0310 pm BOC Poloz speech

Comments

Log in or sign up to join the conversation.