The act of bending a bit can lead to greatness, trees can grow to the sky, but too much will break you. As the proverb suggests, nothing straight ever grows out of the crooked timber of humanity. Overnight, moods swung positive but Asia remains mired in China/US trade and growth fears while Europe bounces as Italy nears an agreement with the EU. Reports in Corriere della Sera suggest Italy's government has made concessions in order to reach a middle ground with Brussels.

This helped underpin the EUR but worry remains despite indications that a narrower deficit will be pursued, by bringing the deficit from 2.4% of GDP in 2019 to 2.2% in 2020 and 2.0% in 2021. La Stampa reported President Mattarella would refuse to sign a budget containing a 2.4% deficit over 3 years. The budget is expected to be presented to parliament today. There is a short-term easing of worries on this compromise but in the long-term, less growth from fiscal stimulus in Italy will only hurt and adds to expected ECB financial condition tightening. If Italian politics are the positives, then the global PMI reports are the negative – with Japan Services at 2-year lows, Europe mostly lower, UK lower, and EU retail sales lower.

Economic data support the view that the 4Q will reflect further pain from trade tariffs adding to the IMF warnings yesterday. Markets are set up for more concessions into 3Q earnings as the forward looking stories are not so optimistic given the growing view that US/China trade battles will last well beyond the US November mid-term elections. Any signals for trade talks or concessions maybe the upside driver for more volatility. Until then we are stuck balancing growth and politics like the wind in the trees trying to hold onto their leaves. The currency that faces the most risk today is the GBP with the UK PM May speech on deck and Brexit views sharply changing there. The FT notes today that UK opinions have been shifting quickly. If referendums are replayed or new elections called, expect further downside risks with 1.2950 a pivot on the day for 1.2650 retests.

Question for the Day: Is the IMF right about global growth risks? The IMF Lagarde speech Monday got a lot of play given the stark warnings on growth with trade tariffs and tightening monetary conditions cited. Today the IMF WEO is updated at 10 am and this is going to be important. The FOMC speakers today maybe viewed against this release. The WEO will have a 10-year lookback to 2008 and the crisis as well as a key chapter on emerging market economies and how they respond to financial conditions normalizing. The running consensus about the crisis and how it played out supports QE and zero rate policies. The Lagarde speech pushes for more government control and action to support economies, at odds with the bilateral pushes from the US to renegotiate trade and to cut back government plans. How this plays out will be the key for 2019 and likely adds to how budgets and Capex is set for the next year.

What Happened?

- Australia September Service PMI 52.5 from 52.2 – less than 53.8 expected. 4 of the 5 sub-indexes were higher, while 7 of 9 sub-sectors rose. The retail component sets new high up 2 to 59.2 – best since June 2016. New orders continue to expand – best run since Sep 2005.

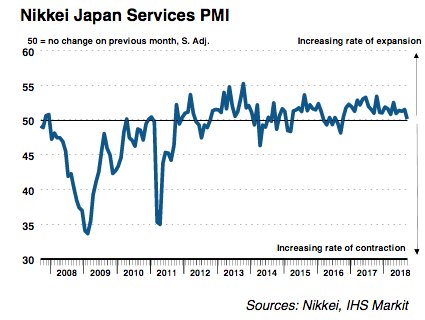

- Japan September Service PMI 50.2 from 51.5 – weaker than 51.8 expected – 2-year lows. The Composite drops to 50.7 from 52. Despite slower output, new business and employment expanded, albeit jobs fell back to 3M lows. Business confidence for Services remains positive near 2018 averages while Manufacturing was a 22-month lows on trade demand worries. Input prices continued to worry with fuel and labor prices higher.

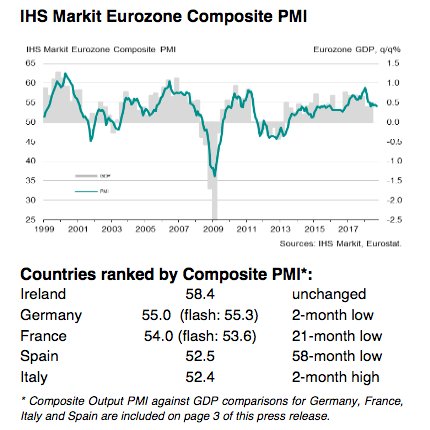

Eurozone September Final Service PMI 54.7 from 54.4 – same as flash – as expected – back to May 2016 levels. The Composite PMI 54.1 from 54.5 – weaker than 54.2 flash. Manufacturing led the slowdown in September while Services rose to 3M highs. Exports are a key worry as trade flows have stalled. Business confidence is near 2-year lows.

- Spanish Service PMI 52.5 from 52.7 – weaker than 52.9 expected. New orders at 21-month lows, sentiment at 5-year lows

- Italy Service PMI 53.3 from 52.6 – better than 52.8 expected.

- French final Service PMI 54.8 from 55.4 – better than 54.3 flash. The Composite 54 from 54.9 – also better than 53.6 flash

- German final Service PMI 55.9 from 55 – weaker than 56.5 flash – but 8-month highs. The Composite 55 from 55.6 – also weaker than 55.3 flash.

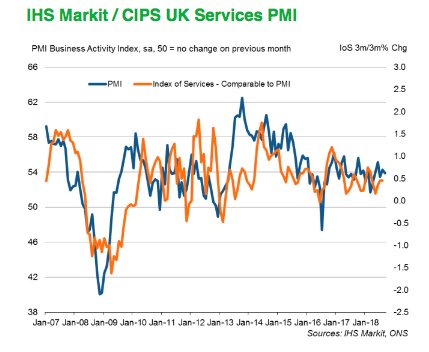

- UK September Service PMI 53.9 from 54.3 – weaker than 54 expected. Still, this is above the 2018 average ytd of 53.6. Notable points - the rise in costs 2nd largest over the last 12 months mostly linked to energy. The composite PMI suggests growth of 0.3% q/q in 3Q.

- Eurozone August retail sales -0.2% m/m, +1.8% y/y after revised -0.6% m/m, 1.1% y/y - weaker than +0.2% m/m expected. July revised from -0.2% m/m. This puts 3Q sales average unchanged after 0.8% q/q in 2Q.

Market Recap:

Equities: The S&P500 futures are up 0.2% after losing 0.04% yesterday. The Stoxx Europe 600 is up 0.2% while the MSCI Asia Pacific fell for the 3rd day off 0.7% - worst in 2-weeks. The MSCI EM also down 0.2% - to 2-week lows.

- Japan Nikkei off 0.66^ to 24,110.96

- Korea Kospi on holiday

- Hong Kong Hang Seng off 0.13% to 27,091.6

- China Shanghai Composite on holiday

- Australia ASX up 0.31% to 6,265.20

- India NSE50 off 1.36% to 10,858.25

- UK FTSE so far up 0.15% to 7,487

- German DAX closed for unification day holiday

- French CAC40 so far up 0.1% to 5,474

- Italian FTSE so far up 0.75% to 20,712

Fixed Income: All about Italy and risk-on/off mood swings with FOMC speakers key today along with more data. Slightly weaker PMI kept core from bigger moves, but German holiday exacerbates illiquidity – 10-year German Bunds up 2.5bps to 0.445%, French OATs up 1bps to 0.79% while UK waits for PM May speech and Gilts up 1bps to 1.537%. The periphery is mixed with Italy off 8.5bps to 3.36% while Spain off 0.5bps to 1.53% and Portugal off 0.5bps to 1.885% while Greece up 1.5bps to 4.26%.

- US Bonds sold with curve steeper – watching Fed Speakers– 2Y up 0.8bps to 2.819%, 5Y up 0.7bps to 2.958%, 10Y up 1.3bps to 3.076% and 30Y up 1.3bps to 3.231%.

- Japan JGBs stuck in tight ranges– BOJ kept Rinban buying Y1.1trn unchanged. Offer to cover ratios: 1-3 Year 3.95 (prev. 2.71), 3-5 Year 3.09 (prev. 2.41), 5-10 Year 3.17 (prev.1.96). 2Y off 0.2bpst o -0.127%, 5Y flat at -0.076%, 10Y up 0.5bps to 0.128%, 30Y flat at 0.907%.

- Australian bonds hold bid with good auction. The AOFM sold A$500mn of 10Y 3.25% Apr 2029 Bonds #TB138 at 2.6465% with 4.97 cover. 3Y off 3.7bps to 1.985%, 10Y off 3bps to 2.635%.

Foreign Exchange: The US dollar index off 0.05% to 95.45 with 95.25-95.55 range – stuck in consolidation with 94.95-95.75 keys. In EM, USD holds bid – EMEA: ZAR off 0.1% to 14.375, RUB off 0.1% to 65.58, TRY off 1.5% to 6.075; ASIA: TWD flat at 30.66, KRW up 0.1% to 1118 (but on holiday), INR off 0.45% to 73.23

- EUR: 1.1560 up 0.1%.Range 1.1536-1.1594 with focus on Italy and 1.15 base for 1.1620 again

- JPY: 113.85 up 0.15%.Range 113.52-113.90 with EUR/JPY 131.60 up 0.3% - despite Nikkei holding with EUR and Italy stories, 114 pivot for 115 barrier test

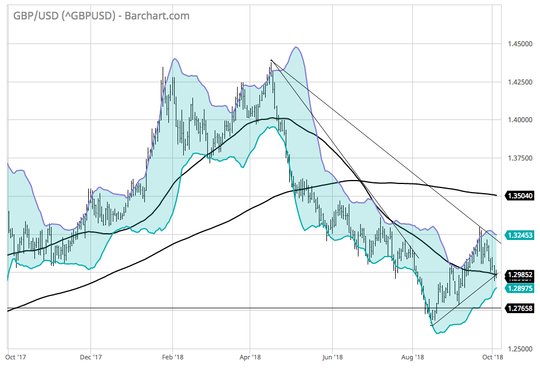

- GBP: 1.2985 up 0.1%.Range 1.2972-1.3017 with EUR/GBP .8900 – waiting for PM May Tory speech and more data.

- AUD: .7155 off 0.45%.Range .7149-.7197 with weaker A$ helping shares but China growth worries rising, NZD off 0.45% to .6560 with .6520 key.

- CAD: 1.2835 up 0.1%.Range 1.2808-1.2942 with USMCA gap filled, risk is 1.2750 again but for rates/oil and crosses.

- CHF: .9865 up 0.3%.Range .9834-.9873 with EUR/CHF up 0.4% to 1.1410 again – all about Italy. 1.1450 key along with .9920 resistance.

Commodities: Oil up, Gold up, Copper up 0.2% to $2.8345.

- Oil:$75.25 flat. Range $75.02-$75.57. WTI watching $70 base against $79 target with $74-$76.50 consolidation. API had a smaller build in crude stocks and a larger draw in gasoline – adding to Russia slower production story yesterday – supporting prices today. Brent $up 0.1% to $84.87 with $85 pivot for $87 target against $83.50 base.

- Gold: $1203.85 flat. Range $1202-$1205. Gold watching $1203 55-day as key pivotal break and $1200 base for $1214.4 Aug 28 highs. Silver $14.78 up 0.6% with 55-day at $14.77 breaking for $15 upside resistance against $14.50 pivotal base with $14.18 Sep 27 lows behind it. Platinum up 0.1% to $832 and Palladium up 0.15% to $1057

Economic Calendar:

- 0630 am Chicago Fed Evans Speech

- 0805 am Richmond Fed Barkin Speech

- 0815 am US Sep ADP employment change 163k p 185k e

- 0945 am US Sep final Service PMI 54.7p 53.4e / Composite 53.4p 54.1e

- 1000 am US Sep Service ISM 58.5p 58.1e

- 1030 am US weekly EAI crude oil stocks 1.853mb p -1.27mb e

- 0200 pm Fed Gov Brainard speech

- 0215 pm Cleveland Fed Mester speech

Comments

Log in or sign up to join the conversation.