The world post the US Labor Day Holiday is getting back to work on the usual worries, and with the new month, investors seem busier jockeying for positions into the end of the year race for returns. The fear of missing out on a larger rally up in risk assets balances against the significant doubts from emerging markets, ongoing geopolitical fears about US Trump trade policy and increasingly doubts about Brexit. For today, the USD is back in the driving seat winning despite an RBA that was not dovish, helped by weaker UK Construction PMI, ongoing concerns in the EU about trade both with the US and UK and the rising Balkans conflict.

The Croatia/Serbia border discussions remind investors of the 1990s war and chaos there. Russia may use this as justification for its Crimea take-over and further EU expansion may stall if the EU blinks. Against that new story, the old one about Italian politics seems to be better – or at least mean reverting – as the League gains in the latest SWG polls to 32.2% from 17.4% in the March elections and 30.3% back in July. This has lifted periphery bonds but it hasn’t led to EUR/CHF higher. Argentina is going to be under the microscope again today with Macri unveiling his austerity plan yesterday and battle plan against the crisis measured by ARS which is off 0.43% at 38.5 now with 40 the line in the sand to watch. For trading today, the biggest mover is oil and it is mostly due to the Gulf Hurricane Gordon which seems set for disruption of oil production and refineries. Oil breaking out means more trouble for central bankers as the wrong kind of inflation hits consumers and trade concerns hit corporations. This is a day where the USD bid has implications for risk-off more than risk-on. The USD bid maybe more about weakness abroad than at home but the correlation matters more than the causality. A retest of 96.60 seems underway.

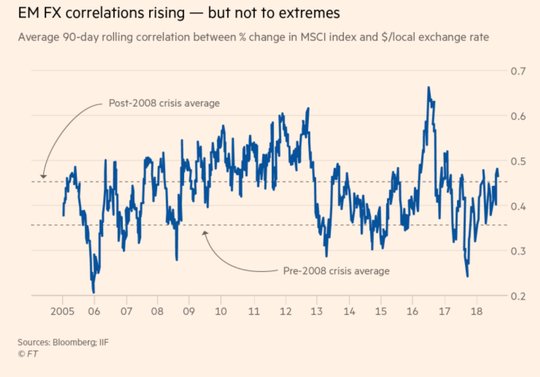

Question for the Day: Are EM markets at the extremes? The depreciation of ARS and TRY has led to a shift in policy from central bankers in EM. They are raising rates to fight the inflation from weaker FX. The correlation of rates to FX to stocks is rising and its important as this is the transmission mechanism for contagion to developed markets. The FT and WSJ are all about EM contagion analysis. This is the key for understanding risk taking in September and whether you buy the dip or not will be linked back to the argument that Emerging Markets. as a whole, have reached extreme oversold levels for stocks, bonds and FX. Value buying rests on these assumptions. For my two-cents, the pain trades in FX are not fully fed through to real economies in emerging markets and the rate hikes needed to bring capital flows back haven’t yet convinced investors – 60% in Argentina perhaps being the exception.

What Happened?

- Australia 2Q Current Account Deficit $13.5bn after A$11.7bn – worse than A$11.5bn expected. The net primary income deficit rose A$1.1bn in Q2 to A$15.9bn. The main reason for the higher deficit was increase in direct investment liabilities, income on equity and investment fund shares which rose A$715 million. The balance on goods and services was A$2.8bn in Q2 compared with A$3.3bn in Q1. In seasonally adjusted chain volume terms, the balance on goods and services deficit fell in Q2, and is expected to contribute 0.1% to Q2 GDP growth. Also adding to 2Q GDP is government spending up 1% q/q, adding 0.2% to 2Q growth. Terms of trade fell 1.3% in Q2, following a 3.3% rise in Q1. The fall was due to an increase of 1.4% in the implicit price deflator (IPD) for goods and services credits, and an increase of 2.7% in the PID for goods and services

debits. - RBA leaves cash rate unchanged at 1.5% - as expected – upbeat on growth outlook despite US trade policy uncertainty. “The Bank's central forecast is for growth of the Australian economy to average a bit above 3 per cent in 2018 and 2019. In the first half of 2018, the economy is estimated to have grown at an above-trend rate. Business conditions are positive and non-mining business investment is expected to increase. Higher levels of public infrastructure investment are also supporting the economy, as is growth in resource exports. One continuing source of uncertainty is the outlook for household consumption. Household income has been growing slowly and debt levels are high. The drought has led to difficult conditions in parts of the farm sector.”

- Spanish August unemployment rose 47,047 up 1.5% m/m to 3,182,068 after falling 27,141 or -0.86% in July – near expectations. The seasonality of jobs in Spain notable.

- Swiss August CPI 0% m/m, 1.2% y/y after -0.2% m/m, 1.2% y/y – more than 1.0% y/y expected. The core (ex-fresh food and energy) CPI was 0% m/m, 0.5% y/y while the HICP was 0% m/m, 1.3% y/y.

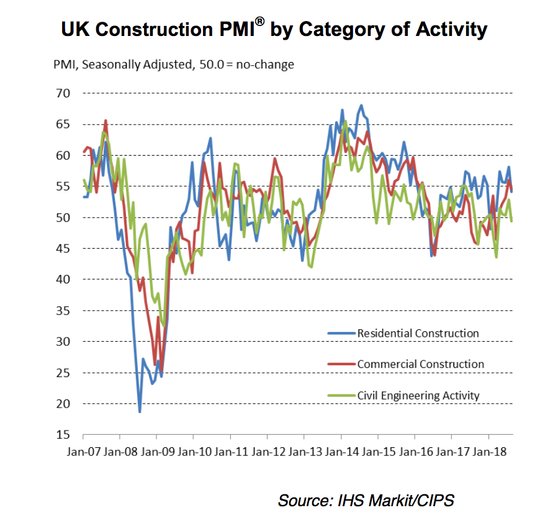

- UK August Construction PMI 52.9 from 55.8 – weaker than 54.8 expected – 3-month lows. Supplier delivery times lengthen to Mar 2015 levels but input cost inflation eases to 25-month lows. Commercial activity lead gains, residential building moderated back to March levels and engineering contracted. Outlook for the next 12M remains positive but eases back to May levels with Brexit concerns the number one concern.

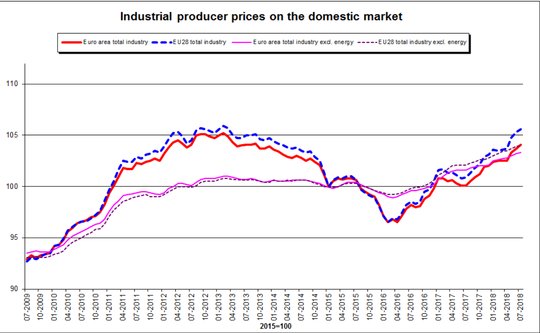

- Eurozone July PPI up 0.4% m/m, 4% y/y after 0.4% m/m, 3.6% y/y – more than 0.3% m/m, 3.9% y/y expected. The energy PPI rose 1.1% m/m, 10.7% y/y after 9.5% y/y while the ex-energy rose 0.1% m/m, 1.7% y/y after 1.6% y/y. Price growth across all other categories remained subdued in comparison, with intermediate goods, capital goods, durable consumer goods and non-durable consumer goods prices all rising by 0.1% m/m

Market Recap:

Equities: US S&P500 futures are up 0.07% - were up 0.25% yesterday – after 0.01% gain Friday. Nike in focus with controversial ad. The Stoxx Europe 600 is off 0.4% with early gains of 0.1% reversed with miners and automakers leading weakness. The MSCI Asia Pacific rose 0.2% with China leading, JPY gains hit the Nikkei. The MSCI all-country World Index is off 0.3% - to 1 week lows and the MSCI EM index is off 0.2% to 2-week lows.

- Japan Nikkei off 0.05% to 22,696.90

- Korea Kospi up 0.38% to 2,315.72

- Hong Kong Hang Seng up 0.94% to 27,973.34

- China Shanghai Composite up 1.1% to 2,750.58

- Australia ASX off 0.27% to 6,398.90

- India NSE50 off 0.54% to 11,520.30

- UK FTSE so far off 0.15% to 7,495

- German DAX so far off 0.70% to 12,261

- French CAC40 so far off 1% to 5,360

- Italian FTSE so far up 0.4% to 20,479

Fixed Income: Risk-on mood from Asia set up EU bonds to drift lower from the open, with RBA less dovish than some thought a driver and China shares holding bid. The flip-flop in equities led to a similar turnabout in bonds today. Auctions were also well supported and added a bit of noise. German 10-year Bund yields up 1bps to 0.34% while France is off 0.5bps to 0.687% and UK Gilts are up 0.2bps to 1.405% waiting for BOE inflation testimony. The periphery is bid – Italy off 7.5bps to 3.077%, Spain off 2bps to 1.425%, Portugal off 3bps to 1.857% and Greece up 1bps to 4.405%.

- Germany sold E0.75bn of linkers with mixed demand (technically failed auction) – E0.5bn of 12Y 0.5% Apr 2030 BundEiat -0.97% with 1.26 cover – previously -1% and 1.4 cover. Also E0.20bn of 30Y 0.1% Apr 2046 BundEi at -0.67% with 0.87 cover – previously -0.68% with 1.17 cover – after the Bundesbank, cover rose to 1.1 vs. 1.8 previously.

- Austria AFFA sold E1.1bn of bonds at lower rates and good demand – E600mn of 4Y 0% Sep 2022 RAGB at -0.294% with 2.3 cover – previously -0.04% with 2.5 cover – E500mn of 10Y 0.75% Feb 2028 RAGB at 0.534% with 3.3 cover – previously 0.554% with 2.1 cover.

- Belgium sold E1.617bn of 4&6M bills with mixed results – E902mn of 4M Jan 2019 TC at -0.605% with 2.8 cover – previously -0.554% with 3.78 cover – and E715mn of 6M Mar 2019 TC at -0.56% with 3.38 cover – previously -0.603% with 3.42 cover.

- US Bonds sold from Holiday highs focus is on Trump and key data ahead – 2Y up 0.6bps to 2.633%, 5Y up 0.7bps to 2.745%, 10Y up 1.1bps to 2.871%, 30Y up 1.9bps to 3.038%.

- Japan JGB curve steepens, BOJ Rinban focus – 2Y -0.124% off 0.2bps, 5Y -0.075% flat, 10Y up 0.1bps to 0.109%, 30Y up 0.5bps to 0.85%. The BOJ Rinban increased size of 1-5Y buying, and the offer to cover ratios were lower in the front and higher in the back of the curve – 1-3Y 2.91 from 3.29, 3-5Y 2.85 from 3.41, 10-25Y 3.31 from 3.47 and 25+Y 4.08 from 3.69.

- Australian bonds sold on RBA not sounding dovish enough, watching US/China still – 3Y up 1.5bps to 1.978%, 10Y up 0.5bps to 2.522%

- China PBOC skips open market operations for 10th day, leaves liquidity neutral. There are no reverse repos maturing this week but there is CNY176.5bn in 12M MLF settling. Money market rates fell with O/N off 6.5bps to 2.18% and 7-day off 6.5bps to 2.513%.10Y bond yields rose 2bps to 3.62%.

Foreign Exchange: The US dollar index up 0.5% to 95.52 with range 95.13-95.57 – focus is back on 95.95 and 96.10 resistance against 95.10 and 94.95 support. Emerging Markets continue USD bid with focus on ARS, TRY and ZAR. ASIA is USD bid: TWD off 0.15% to 30.76, INR off 0.45% to 71.53, KRW off 0.4% to 1115. EMEA is USD bid: ZAR off 2.25% to 15.19, RUB off 0.5% to 68.255, TRY off 0.9% to 6.697

- EUR: 1.1555 off 0.55% Range 1.1552-1.1621 with Italy better but trade worries rising and EU/Balkan story negative with 1.1510 pivotal.

- JPY: 111.45 up 0.3%. Range 110.90-111.53 with weakness of $ in Asia reversed focus is on stocks and 110.70 pivot for 110 or 112 again. EUR/JPY 128.75 off 0.25% with 128-130 consolidation.

- GBP: 1.2825 off 0.35%. Range 1.2814-1.2876 with focus on Brexit and BOE still 1.2750 key for 1.26 vs. 1.30 again. EUR/GBP off 0.15% to .9015 – trade more than Brexit matters here.

- AUD: .7175 off 0.5%. Range .7157-.7235 with RBA not dovish helping but metals and C/A, terms of trade negative with .72 break opening .7050 tests. NZD off 0.85% to .6545 with return to new yearly lows driving technical washout with .6450 risks.

- CAD: 1.3155 up 0.45%. Range 1.3090-13157 with BOC and trade talks balancing – 1.30-1.32 consolidation.

- CHF: .9745 up 0.55%. Range .9689-.9745 with EUR/CHF 1.1255 off 0.05% - still blinking yellow for risk. .9650-.9800 consolidation for USD.

- CNY: 6.8183 fixed 0.24% stronger from 6.8347, trades weaker into London at 6.8294 from 6.8165 official close yesterday, now 6.8360 off 0.2% with 6.8401 USD highs.CNH flat at 6.8485 with range 6.8221-6.8514

Commodities: Oil up, Gold down, Copper off 1.4% to $2.6755

- Oil: $70.97 up 1.7%. Range $69.53-$71.22. WTI watching $71.05 July 10 highs for $71.63 May 22 and $72.50 target. Brent up 1.25% to $79.11 watching $79.15 May 22 highs then $80 resistance against $74.80 the 55-day m.a. base. US hurricane watch for Gulf coast driving oil and products higher.

- Gold: $1195.60 off 0.5%. Range $1195-$1202. Gold watching $1160.40 Aug 16 lows again with USD driving and $1217.1 the Aug 10 highs resistance. Silver $14.26 off 1.8%,now watching $13.984 the Aug 26 lows against $14.50 resistance. Platinum off 1.8% to $774.70 and Palladium off 2% to $963.25.

Conclusions: Can the Bank of Canada normalize? While the RBA was on hold today and didn’t directly address the mortgage rate hikes from some banks there, many expect that to be in the minutes and to be dovish. For the BOC, the talk is expected to be more hawkish but for the fear of politics and trade deals. The BOC is balancing good but not great growth against the need to normalize rates to match the US. The 1.5% level isn’t going to cut it for C$ support if NAFTA talks fail.

Economic Calendar:

- 0930 am Canadian Aug RBC Manufacturing PMI 56.9p 57.1e

- 0945 am US Aug final Manufacturing PMI 55.3p 54.3e

- 1000 am US Aug Manufacturing ISM 58.1p 57.7e

- 1000 am US July Construction Spending (m/m) -1.1%p +0.6%e

- 1000 am US Sep IBD/TIPP Economic Optimism 58p 57.7e

- 1030n am US Chicago Fed Evans Speech

- 0330 pm US Aug Total Vehicle Sales 16.77m p 16.80m e

Comments

Log in or sign up to join the conversation.