Welcome to Ash Wednesday, when thinking and rethinking are required as we contemplate life and death and the inevitability that we are all dust and will return to it in good time. When markets don’t react the same way with the same stimulus, investors need to rethink the logic of what got them into their position and what will force them out. Geopolitical risk reduction was a key part of 2019’s bull run with a patient FOMC thrown on top for fun. The rise of US non-manufacturing ISM puts that into question and leaves the jobs report Friday as an event risk for rates again. The hope for a soft and easy Brexit was dashed again overnight as EU/UK talks ended with no agreement last night. The US/China trade deal has been priced as both Xi and Trump want and need a deal, but the fallout from that is in doubt as the quantitative targeting of buying US goods at the expense of other nations – Europe, emerging markets – means higher prices, less USD from exports. There is a rising view that any deal is not good enough for the longer-term sustainability of global trade and growth unless you believe that the US can thrive alone. Yesterday’s push from Trump to scrap India’s and Turkey’s participation in privileged trading programs is another warning signal of such fears. Overnight the biggest headline was about the fallout from the failed second Kim/Trump summit in Vietnam. There is a nuclear arms race in play across the world. North Korea appears to be rebuilding its Launch Site for missile testing, Saudi and Iran are in a race to join India and Pakistan and North Korea with nuclear bomb technology. Rethinking the world after WWII continues as the Pax Americana, post the fall of the Berlin Wall, crumbles into a more dangerous world where the US no longer wears the white hat, nor does anyone else. There is rising geopolitical risks as authoritarian nations see there own unhappy citizens and act to the extremes, just as the democracies see the rise of the populist. Both undermine faith in the rule of law and the order of things. The USD was the winners today in such a world and that is without much rethinking but the real dust-up overnight was in the weaker AUD, which broke .7050 support and looks set to test .68 again.

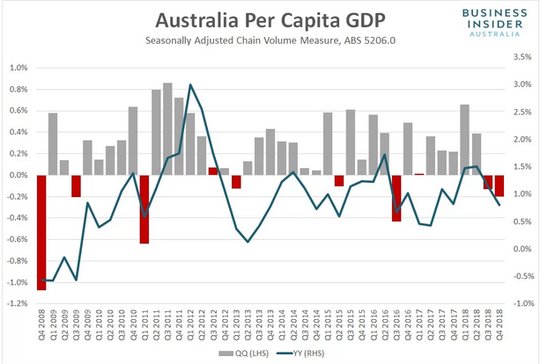

The AUD weakness is important as it contrasts with the China share rally for the 3rdday. Manipulation of the China equity market during the National People’s Congress and its push for stimulus to support the economy isn’t as believable as the AUD and the GDP report today. The per capita growth recession hasn’t been a topic since 2003.

Question for the Day: Has US divergence returned? The US GDP against that of Europe or Asia returns as the explanation for USD strength and US equity gains. Today’s 4Q Australian GDP is a case in point for the AUD where a 0.2% q/q gain versus 0.3% q/q expected leads to FX volatility. The logic goes that US growth at 2-2.5% in 2019 will outshine Europe, Japan and elsewhere in the G15, will be competitive with emerging markets when viewed against their FX risks and will lead to another FOMC rate hike or two. The playing out of the Goldilocks story rests on US inflation remaining tame and no other shocks or surprises being delivered. The compare and contrast to consider is from the forecasts for GDP against the rest of the world.

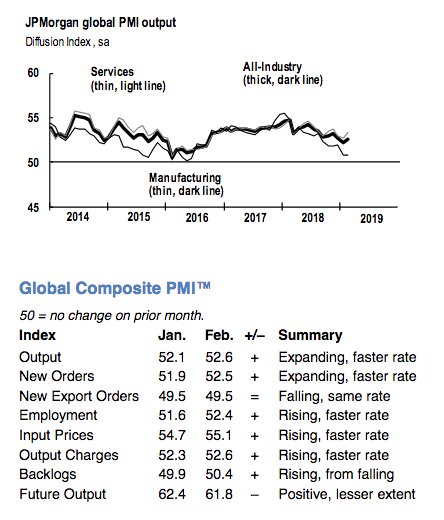

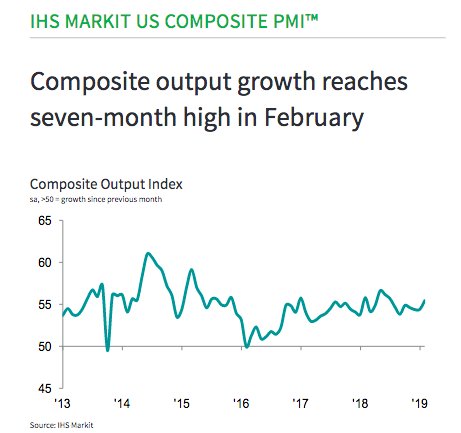

Throw in the stark contrast of the JPM global composite PMI against that of the US composite PMI and you have a clear signal that stabilization in the rest of the world looks weak compared to the US trend – with the composite 55.5 from 54.4 – at 7-month highs. Throw in that the US is much more service focused and the only weakness was in manufacturing linked back to US trade issues and you have further expectations for USD outperformance.

What Happened?

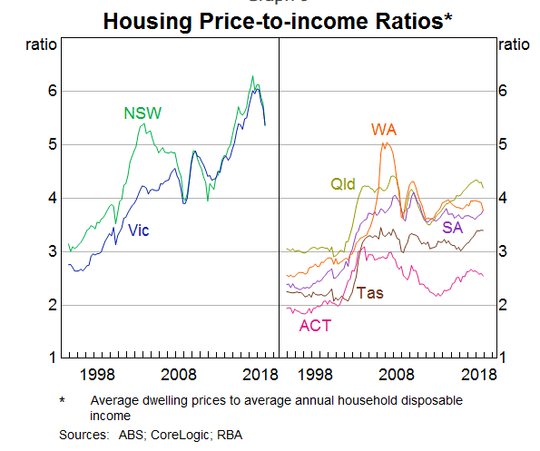

- RBA Lowe: Housing and labor keys for policy. The RBA Governor speech on the housing market and the economy linked back the role of housing wealth to consumers. He also noted that job demand and wages were essential for continued consumer spending and price inflation. This is the key part of the housing argument and focus: “Today, I would like to focus on the effect of housing prices on household consumption. My colleagues at the RBA have examined how changes in measured housing wealth affect household spending. They estimate that a 10 per cent increase in net housing wealth raises the level of consumption by around ¾ per cent in the short run and by 1½ per cent in the longer run. They have also examined how this wealth effect differs by type of spending. They find that it is highest for spending on motor vehicles and household furnishings and that for many other types of spending the effect is not significantly different from zero. Part of the effect on spending on furnishings is likely to come from the fact that periods of rising housing prices are often associated with higher housing turnover, and turnover generates extra spending.”

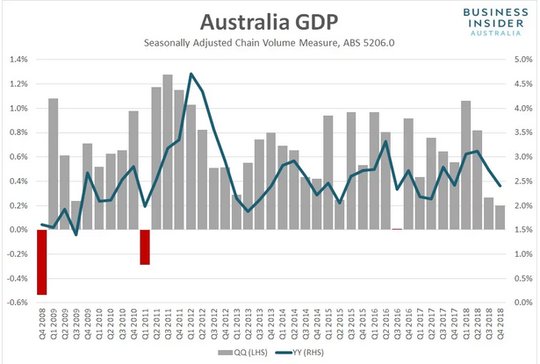

- Australia 4Q GDP slows to 0.2% q/q, 2.3% y/y from 0.3% q/q , 2.8% y/y – weaker than 0.3% q/q, 2.6% y/y expected. Soft household spending at 0.4% q/q, less investment in housing fell 3.4% (taking 0.1pp q/q) both were notable drivers for the slowdown. Inventories added 0.2pp to growth offsetting 0.2pp from private sector investments. Government spending added 0.3pp to growth. With Australian population growth running around 0.4% per quarter, and real GDP growing by 0.2%, per capita GDP went backwards during the quarter, falling 0.2%. Combined with a 0.1% decline in the prior quarter, that means Australia has officially entered a per capita recession.

- BOJ Harada: Ready to ease if risks threaten price goals."If the economy deteriorates to the extent that achieving the inflation target in the long term becomes difficult, it's necessary to strengthen monetary easing without delay," Harada said in a speech to business leaders in Kofu, eastern Japan.

- Eurozone February construction PMI rose to 52.6 from 50.6 – better than 51 expected. Increases in commercial and infrastructure activity led the bounce as they reversed from 3-months of contraction. Housing also recovered from 3-month lows. New orders increased.

- German February construction PMI jumps to 54.7 from 50.7 – better than 50.5 expected. This was the best since Jan 2018 – led by housing. New orders and employment were best since Jan 2018.

- Italy February construction PMI slips to 50.7 from 51.8 – weaker than 51.5 expected. This is 11-month lows with new business dragging but employment rose at the best pace since March 2007.

- French February construction PMI recovers to 51.3 from 49.5 – better than 50 expected. The growth remains well below the 53 average of 2018. Rebounds in output and new orders didn’t help employment, which fell for the 4th month and is worst since Aug 2018.

Market Recap:

Equities: The US S&P 500 futures are off 0.15% after a 0.11% loss yesterday. The Stoxx Europe 600 is flat with focus on banks and autos. The MSCI Asia Pacific was up 0.1% as China gains offset Japan.

- Japan Nikkei off 0.60% to 21,696.81

- Korea Kospi off 0.17% to 3,222.84

- Hong Kong Hang Seng up 0.26% to 29,037.60

- China Shanghai Composite up 1.57% to 3,102.10

- Australia ASX up 0.72% to 6,326.80

- India NSE50 up 0.60% to 11,053.00

- UK FTSE so far up 0.2% to 7,198

- German DAX so far off 0.2% to 11,595

- French CAC40 so far off 0.1% to 5,290

- Italian FTSE so far up 0.3% to 20,784

Fixed Income: Back to doubt – bonds holding bid – with ECB next key focus for Europe, US data and FOMC for UST. German 10-year Bund yields off 1bps to 0.15%, French OATs off 1bps to 0.55%, UK Gilts off 3bps to 1.26% - with Brexit talks sour. In periphery – chase for yield continues, Italy catches some headlines with its support for the China Belt and Road push – Italian BTPs off 3bps to 2.69%, Portugal off 2bps to 1.44%, Spain off 2bps to 1.15% and Greece up 3bps to 3.73%.

- UK DMO sold GBP3bn of 5Y 1% Gilts at 0.966% with 1.99 cover from 1.018% previously.

- US Bonds are bid waiting for ADP and Fed speakers– 2Y off 1bps to 2.54%, 5Y off 1bps to 2.52%, 10y off 1bps to 2.72%, 30Y flat at 3.09%

- Japan JGBs are bid with BOJ and negative equities– 2Y flat at -0.14%, 5Y off 1bps to -0.15%, 10Y off 1bps to -0.01%, 30Y off 1bps to 0.63%.

- Australian bonds are bid on weaker GDP and Lowe speech– 3Y off 5bps to 1.62%, 10Y off 5bps to 2.11%, NZ 10Y off 3bps to 2.17%.

- China bonds quiet with curve flatter– 2Y up 1bps to 2.77%, 5Y up 1bps to 3.08%, 10Y off 2bps to 3.22%. The PBOC drained CNY60bn as reverse repos matured today – citing abundant liquidity – as it continued to skip open market operations.

Foreign Exchange: The US dollar index up 0.1% at 96.93. In emerging markets the USD is bid – EMEA: ZAR off 0.4% to 14.216, RUB off 0.1% to 65.846, TRY off 0.2% to 5.3930; ASIA: INR up 0.3% to 70.266, KRW off 0.25% to 1127.60

- EUR: 1.1300 flat. Range 1.1290-1.1310 with focus on ECB tomorrow – economic stability vs. politics with 1.1250 key.

- JPY: 111.85 flat. Range 111.72-111.92 with EUR/JPY 126.40 flat watching equities vs. BOJ vs. US/China and 112 cap.

- GBP: 1.3135 off 0.1%. Range 1.3124-1.3179 with EUR/GBP .8605 up 0.1%. EU/UK talks negative so GBP off a touch but 1.3050-1.3350 holding.

- AUD: .7025 off 0.7%. Range .7024-.7092 with NZD off 0.3% to .6770 – all about weaker GDP and RBA Lowe focus on housing/jobs. .7050 break opens .6970 and .6835 next.

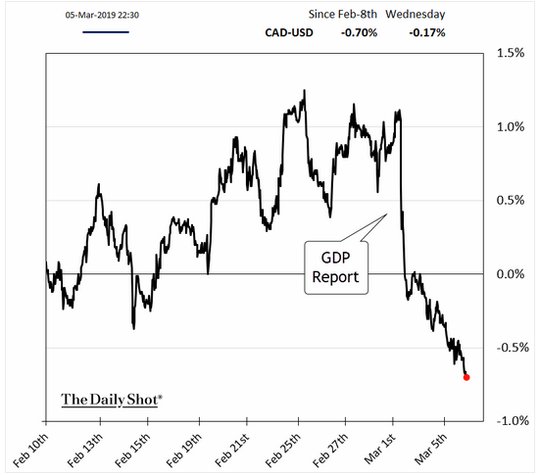

- CAD: 1.3375 up 0.2%. Range 1.3348-1.3381 with focus on BOC today and 1.3450 breakout risks. Politics background issue.

- CHF: 1.0045 up 0.1%. Range 1.0036-1.0055 with EUR/CHF 1.1360 up 0.1%. Risk isn’t the driver and 1.0080 is back in focus.

- CNY: 6.7075 flat. Range 6.7010-6.7180. PBOC fixed 6.7053 from 6.6998 with focus on GDP target and tax cut.

Commodities: Oil lower, Gold higher, Copper off 0.3% to $2.9610

- Oil: $56.17 off 0.7%. Range $55.80-$56.32 with Brent flat at $65.87. API reported crude supply up 7.3mb much more 2mb expected. EIA key again to confirm. The WTI market still watching $55 as key base support.

- Gold: $1286.60 up 0.15%.Range $1285.70-$1291.80 with $1282 support holding and focus on USD/global risks – Silver flat at $15.11, Platinum off 0.5% to $833.50 and Palladium up 0.2% to $1469.00.

Conclusions: Will the Bank of Canada matter today? Short answer is yes but it’s complicated. The US and Canadian trade deficits will be the economic backdrop for another rate meeting in Canada where the risk of an about face on tightening seems warranted. The BOC Poloz risk is reflected in the C$ post the disappointing 4Q GDP. Canada economic weakness and housing fear is sufficient for more than US like patience. The off-set is that a much weaker C$ could help on trade and increase price pressures making the BOC work more challenging.

However, the real issue for the BOC is in the politics unwinding in Canada as Trudeau faces his biggest political crisis with allegations that he interfered in a corruption case with SNC-Lavalin. The reaction of markets to political risks varies – just watch the US Congress and Trump battle it out as an example – but the present Trudeau problem is in some ways more problematic given he has lost two cabinet members and has the opposition party asking him to step down. The political turmoil in Canada makes the international relationships with the UK, EU, China and the US less certain and so hurts capital flows and investment. More importantly, is the hit to the polls as the Liberal party is now tied with the Conservatives and Trudeau’s bid for re-election (set for Oct 21 or earlier) suffers leaving a gridlock or weak government gloom over Canada.

Economic Calendar:

- 0800 am Poland central bank rate decision no change from 1.5% expected.

- 0815 am US Feb ADP employment change 213k p 190k e

- 0830 am Canada Dec trade deficit C$2.06bn p C$2.39bn e

- 0830 am US Dec trade deficit $49.3bn p $57.3bn e

- 1000 am Canada Feb Ivey PMI 54.7p 53e

- 1000 am Bank of Canada rate decision– no change from 1.75% expected – dovish tilt expected

- 1030 am US weekly EIA oil inventories -8.647mb p +2.8mb e

- 1210 pm NY Fed Williams speech

- 0200 pm US Fed Beige Book

Good Luck

Comments

Log in or sign up to join the conversation.