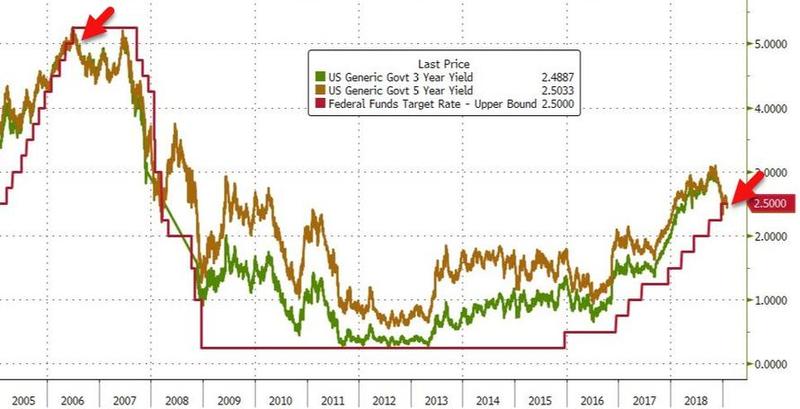

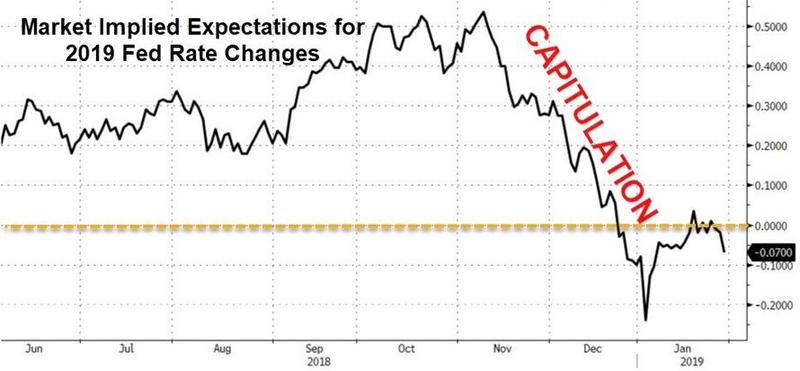

For the first time since the financial crisis, the bond market is now pricing in no more rate hikes in this cycle.

Instead it is expecting lower rates ahead.

But, as Bloomberg reports, not everyone is convinced that the market has this right and that The Fed is done.

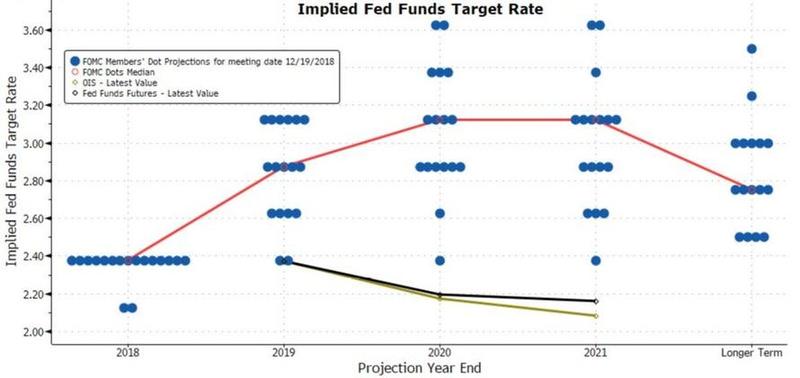

For one, the Fed's dot-plots are vastly out of line with what is priced into the market and to adjust so violently would likely spook investors more than the doivish tilt could be expected to calm them...

Sonal Desai, chief investment officer for the $150 billion fixed-income group at Franklin Templeton, has a stronger perspective, writing in her blog that:

“The market’s assumption that the Fed will not raise interest rates at all this year is very misguided, against a background of continued economic strength,”

“Expectations that the U.S. economic cycle is coming to an end are highly overstated.”

Additionally, Desai forecasts at least two hikes this year as policy makers respond to the risk that wage growth fans inflation.

"I think the Fed will continue to normalize monetary policy because the US economy has already shown it can withstand higher interest rates compared to where we are today. When we saw the US 10-year Treasury move above 3% last year, there was some panic, some dislocation in the short term. But then financial markets stabilized, and the economy kept growing at a robust clip. Therefore, rising rates should not be a reason for investors to panic, in our view.

We will get periods of volatility in the year going forward, but active managers can take advantage of these periods to seek out potential opportunities."

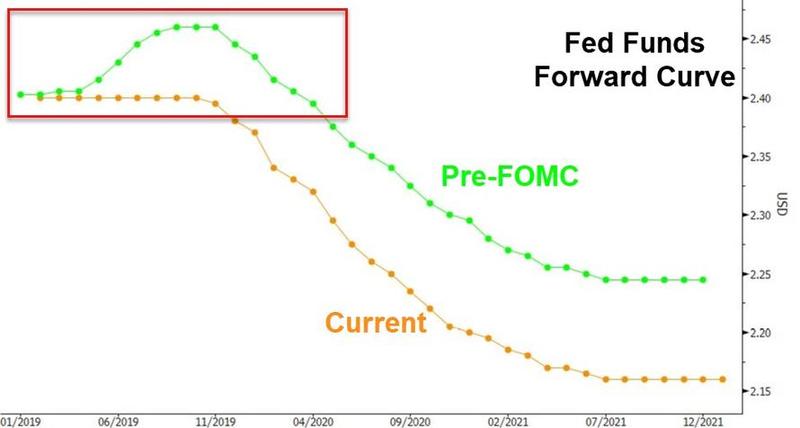

That’s at odds with traders who’ve priced out the hiking cycle and have upped wagers on cuts in 2020.

And at odds with history, as Raoul Pal points out:

The Fed have never, ever “paused” a full hiking cycle. The always end up cutting. Each cutting cycle has led to a recession except mid 1990’s and 1987. Odds are in favour of the Fed having gone too far already and the stock market figuring it out in due course...

— Raoul Pal (@RaoulGMI) January 30, 2019

Additionally, recession or not, pause or not, fundamentals are fragile at best; dismal at worst...but for now, stocks don't care as the squeeze continues.

Neil Dutta, head of U.S. economics at Renaissance Macro, indicated as much when observing the risk-on move in the wake of Powell.

His colleague, technical guru Jeff deGraaf, agrees:

“A 7 basis point contraction in 2s is hard for us to ignore and qualify as bullish.”

Or is QE4 on its way?

Comments

Log in or sign up to join the conversation.