Celebrating age seems out of favor in a world obsessed with youth and technology but the turn of the markets in October lingers over November despite the best efforts to make it a party for All Saints’ Day. November brings anniversaries from the end of WWI to the Spanish Flu to the assignation of Martin Luther King, Jr. There are two anniversaries to consider today – the start of the EU in 1993 and the start of Bitcoin in 2008 – both matter to financial markets but contrast in their philosophical underpinnings with the EU focused on centralization and BTC focused on decentralized, distributed ledgers. Overnight, both show up as GBP gains on Brexit deal hopes and CNY gains on government support hopes.

- GBP rallied as UK PM May strikes a deal with EU that gives financial services continued access to their market after Brexit. The UK Brexit Secretary Raab in a letter to the Commons committee expects a wider deal in 3-weeks.

- CNY rallied as further stimulus plan hopes drive up shares for the first time in 7-months. After the Wednesday Politboro meeting and weaker PMI reports, Bloomberg reported another round of stimulus plans are in the works– including tax cuts, more deficit spending, more local government special bonds, lower RRR from PBOC, more private lending support, more reform support but nothing for property purchases.

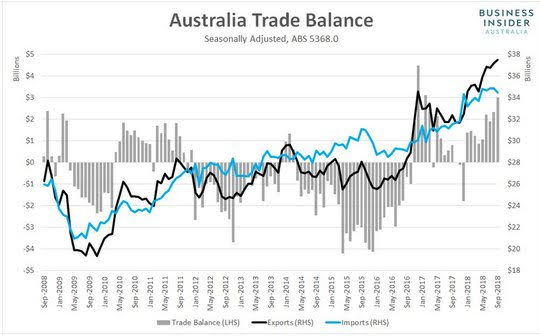

For other FX moves that are notable today pay attention to EUR/SEK as its testing the 200-day support at 10.27, the rebound in tech shares has helped and the Riksbank minutes tomorrow will be critical in determining if rates move in December or February. The AUD gained on commodity demand as shown by the record trade surplus. The economic data was focused on Australian trade which showed a big jump thanks to LNG and Iron Ore linked to China while the PMI reports were mixed with Japan better, UK worse, Australia lower, China Caixin stable. This leaves the day looking risk-on and happy to be rid of October, though the volumes are thinner due to All Saint’s Day holidays in Europe. Many see the Bank of England meeting ahead as the least important part of the GBP uptick story but the role of rates in driving markets remains the key driver with the US markets locked in on ISM and Jobs as the FOMC focus. Risk today is that the BOE sounds more hawkish than priced with just 60% chance for a hike in 2019. Growth in the UK seems linked to the BOE reaction function and the confidence game of Brexit. GBP is the bellwether for keeping risk-on today similar to the CNY holding the 7.00 line still. GBP holding 1.2650 seems important and opens a test for 1.31 should the USD hegemony shift on the data ahead.

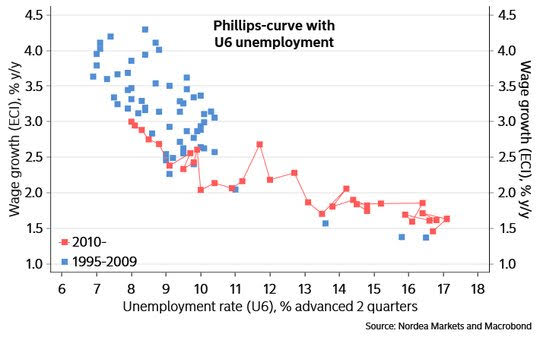

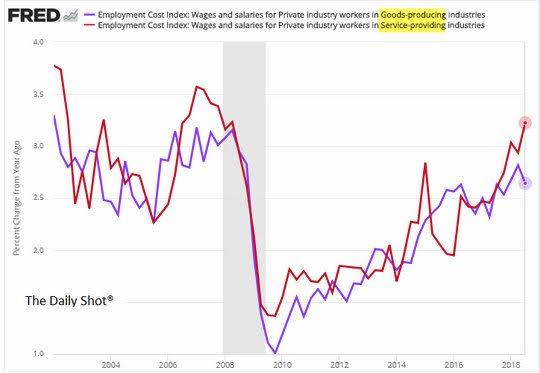

Question for the Day: Is the Phillip’s Curve dead? Many see the only risk to a rally back in November and December coming from inflation – with the impact of tariffs the lesser concern to the FOMC given the focus on jobs and wages. The uptick in the ECI yesterday is important but not sufficient for changing the landscape. The FOMC rate hike for December is mostly priced, but its 2019 that isn’t so obvious.

The effect of tariffs on prices is discounted a bit because many hope that this is just a temporary blimp as Trump negotiates bigger deals – as the NAFTA reworking to USMCA showed. Others note that the bigger losers in tariffs are manufacturers rather than service providers and that showed up clearly in the wage data yesterday. Perhaps this is the problem for Trump politics into the mid-term.

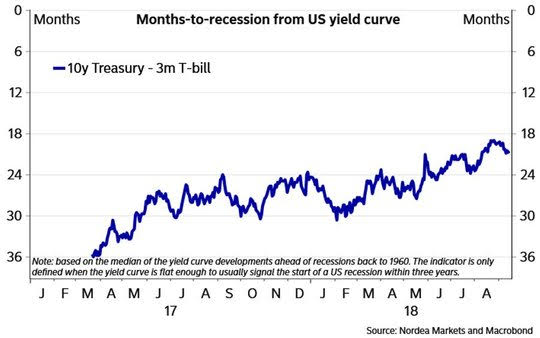

The key maybe less the Phillip's Curve and more the yield curve still as rate moves in the US continue to drive global risk doubts and the ever important US peak earnings, recession fears.

What Happened?

- Australia September trade surplus A$3.017bn from A$2.342bn – much higher than A$1.70bn expected – new record. Exports rose 1% m/m to A$37.499bn while imports fell 1% m/m to A$34.493bn. Aircraft imports fell, capital goods fell and industrial transport equipment fell. Exports were lifted due to metal ores up 7% and fuels (LNG) up 6% but coal fell 3%.

- Australia October AIG Manufacturing PMI drops to 58.3 from 59 – better than 56 expected. The expansion continued from 25 months led by lumber and food. 7 of 8 sectors expanded. Input prices fell 5.6 to 72.8 still higher than 71.1 average blamed on A$ weakness while lower sales were blamed on the drought. Employment fell 5.4 to 52.6 – below the 1-year average, New orders fell 3.8 to 58.8 also below the 1-year average at 9.3. Exports fell 3.8 to 55.1 above the 54.3 average. Input

- Japan October final Manufacturing PMI 52.9 from 52.5 – four-month highs. Foreign demand rose for the first time in 5-months, output prices rise the most in a decade. Output growth bounced from September’s 14-month lows. Order growth led to higher employment – with job creation at 6-month highs. Input prices rose the fastest since Mar 2011 with metals and fuels but firms offset margin erosion with higher output prices.

- China October Caixin Manufacturing PMI rises to 50.1 from 50 – as expected. Output was unchanged, new work rose, input prices rise sharply. Total new business rose only slightly with subdued sales linked to weaker foreign demand, export sales fell for the 7thmonth. Employment also fell, but marginally better contraction. Business Confidence (12-month outlook) dips to 11-month lows.

- UK October Manufacturing PMI 51.1 from 53.6 – weaker than 53 expected. September revised from 53.8. Both new orders and employment fell for the first time in 27-months, but input and output prices ease. Weakness in new orders was both domestic and foreign with consumer goods weakest while investment goods rose. Output was the weakest since August 2016. The IHS Director of the survey Dobson noted: “October saw a worrying turnaround in the performance of the UK manufacturing sector. At current levels, the survey indicates that factory output could contract in the fourth quarter, dropping by 0.2%.”

- Swiss 4Q SECO consumer climate improves to -6 from-7 – slightly above average. The consumer is less confident in 2H2018 than in 1H but still above the -9 long-term average. In particular, consumers have remained confident about the future development in the economy in general and in unemployment. At 9 points, the sub-index on anticipated economic growth has exceeded its long-term average (-9 points) while, at 38 points, the sub index on the expected unemployment development was below average (48 points), thus indicating encouraging prospects on the labor market. This is underpinned by the assessment of job security, which remains above average.

- Swiss October CPI up 0.2% m/m, 1.1% y/y from 1.0% y/y – as expected. The core CPI (ex fresh food/energy) rose 0.1% m/m, 0.4% y/y – also as expected. The imported inflation rose 0.9% m/m, 2.8% y/y while domestic -0.1% m/m, +0.5% y/y.

Market Recap:

Equities: The US S&P500 futures are up 0.3% after 1.09% gain yesterday. The Stoxx Europe 600 is up 0.5% with autos and miners leading – with earnings key driver. The MSCI Asia Pacific was mixed off 0.1% with Japan lower offset by Hong Kong. The MSCI EM index bounced 0.9% to the best in a week.

- Japan Nikkei off 1.06% to 21,687.65

- Korea Kospi off 0.26% to 2,024.46

- Hong Kong Hang Seng up 1.75% to 25,416

- China Shanghai Composite up 0.13% to 2,606.24

- Australia ASX up 0.21% to 5,925.90

- India NSE50 off 0.06% to 10,380.45

- UK FTSE so far up 0.50% to 7,165

- German DAX so far up 0.95% to 11,554

- French CAC40 so far up 0.45% to 5,116

- Italian FTSE so far up 1.00% to 19,242

Fixed Income: European markets trading on thin volume given holidays but Asia started with selling US bonds and US/China trade focus, with UK Brexit deal adding to story for risk-on. UK 10-year Gilt yields up 2bps to 1.455% into BOE while German Bunds up 2.5bps to 0.405% and French OATs up 1bps to 0.76%. The periphery gains led by Italy front end – 10Y BTPs off 7bps to 3.35%, Spain off 1bps to 1.535%, Portugal off 1.5bps to 1.85% while Greece off 1bps to 4.18%.

- US Bonds see curve steepening tracking equities, waiting for data– 2Y flat at 2.867%, 5Y up 1.2bps to 2.987%, 10Y up 1.5bps to 3.159%, 30Y up 2.1bps to 3.412%.

- Japan JGBs gain with Nikkei lower, strong 10Y sale– The MOF sold Y1.7699trn of 10Y JGBs at 0.135% with 4.33 cover – previously 0.141% with 4.21 cover. 2Y flat at -0.133%, 5Y off 0.5bp to -0.096%, 10Y off 0.7bps to 0.109%, 30Y off 0.7bps to 0.853%.

- Australian bonds lower with trade surplus, China hopes, US move– 3Y up 2.7bps to 2.02%, 10Y up 2bps to 2.645%

- China PBOC skips open market operations, net drains CNY100bn. Money market7-day repo rats ease 6.5bps to 2.645%, O/N rises to 14bps to 2.541%. China bonds see rally back with belly lagging– 2Y of 2.8bps to 3.005%, 5Y off 0.2bps to 3.30%, 10Y bonds off 4bps to 3.48%.

Foreign Exchange: The US dollar index fell 0.55% to 96.59 from 97.11 highs to 96.51 lows so far. USD lower in EM – EMEA: ZAR up 1.7% to 14.53, TRY up 0.35% to 5.56, RUB up 0.35% to 65.65; ASIA: TWD up 0.2% to 30.895, KRW up 0.15% to 1138.25, INR up 0.7% to 73.45.

- EUR: 1.1385 up 0.65%.Range 1.1309-1.1388 with bounce from 1.1310 key linked to Brexit, risk-on mood.

- JPY: 112.95 flat. Range 112.72-113.00 with EUR/JPY 128.60 up 0.65% - despite Nikkei pain, 112.70-80 base with 114 back in target.

- GBP: 1.2895 up 1%.Range 1.2763-1.2920 with 1.2905 key pivot for 1.30 test, EUR/GBP off 0.35% to .8830.

- AUD: .7160 up 1.2%.Range .7072-.7165 with trade surplus, China hopes key. NZD up 1.4% to .6610 on for A$ ride with .6680 next.

- CAD: 1.3110 off 0.35%.Range 1.3096-1.3169 with focus on China/commodities and crosses, 1.3050 base with data ahead key.

- CHF: 1.0025 off 0.6%.Range 1.0025-1.0091 with EUR/CHF 1.1425 up 0.15% - less Italy fears, more risk-on, mixed data.

- CNY: 6.9670 fixed 0.05% weakerfrom 6.9646, trades stronger up 0.4% to 6.9495 into London. Now up 0.45% to 6.9450 with 6.9731-6.9431 range.

Commodities: Oil lower, gold higher, Copper up 0.5% to $2.7640.

- Oil: $64.83 off 0.75%.Range $64.65-$65.20 with break of 200-day yesterday key technical for further pain, focus now on $63.50 August lows and $62.35 June lows. Brent off 1% to $74.25 with $72.64 the key 200-day now the focus against $75 pivot and $78.70 55-day.

- Gold: $1223.70 up 0.7%. Range $1214-$1224. Focus is on USD, risk-on moods with $1225 and $1236 key resistance against $1212 yesterday lows. Silver $14.42 up 1.2% with $14.24 base holding opens $14.45 trend resistance test and then $14.80 again. Platinum $849 up 1.4% while Palladium off 0.1% to $1079.30.

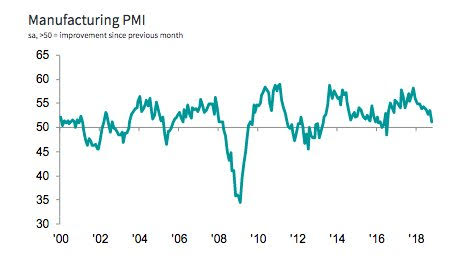

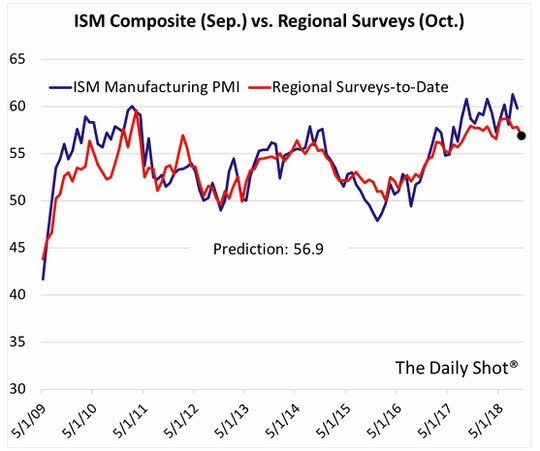

Conclusions: Will ISM matter today? The data from US will be compared to that of China, Europe, and others with ISM the key and with many seeing it slowing modestly. The risk of a larger drop comes from the regional Fed surveys. The role of trade policy and confidence matters for business spending and while the forward-looking parts of the ISM maybe imperfect, they set the tone for risk moods into year-end.

Economic Calendar:

- 0800 am BOE rate decision – no change from 0.75% expected.

- 0830 am BOE Carney news conference

- 0830 am US weekly jobless claims 215k p 215k e

- 0830 am US 3Q productivity 2.9%p 2.0%e / ULC -1%p +1.2%e

- 0930 am Canada Oct Manufacturing PMI 54.8p 54.5e

- 0945 am US Oct final Manufacturing PMI 55.6p 55.9e

- 1000 am US Oct Manufacturing ISM 59.8p 59.0e

- 1000 am US Sep construction spending 0.1%p 0.1%e

- 0330 pm US Oct total vehicle sales 17.44m p 17.10m e

Comments

Log in or sign up to join the conversation.