Qualitative Assessment

Copper has garnered increased focus from investors in recent months for several reasons:

-

Inflation fears are on the rise. Copper has historically been one of the better inflation hedges.

-

The perception that electric vehicles (EVs) are on the rise and the reality that they require more copper.

-

The perpetual dream of infrastructure spending in the U.S. with a greenish tint for some.

-

Supply disruptions in South America and relatively strong Chinese demand.

-

The price has risen above $3 per lb. and remained firmly there.

An investor taking a serious look at copper producers may come to the Global X Funds Copper Miners ETF (COPX) which generally holds copper producers and diversified base metals who include copper in their lineup. One of these holdings is Canadian-based Lundin Mining (LUN.TO; LUNMF), which ironically has no mines in Canada. Lundin currently derives about 2/3s of its revenue from the red metal.

I have been following Lundin on and off for several years and have occasionally been bullish on the stock. Here is my qualitative take.

Lundin is run by accountants. If not literally, then in a philosophical sense. This has advantages and disadvantages but the disadvantages have become heavier in my mind.

There are a few ways that investors can make exceptional returns in the mining industry. A less riskier way is to buy a mid-tier or soon-to-be mid-tier producer with a quality organic growth pipeline. To have a quality organic growth pipeline, you need an exploration unit with good geologists and people on the ground who can connect with local communities and native indigenous groups. What you want to see is management getting down and dirty with the locals and building relationships with them. In recent weeks, this picture has stuck with me:

source: Barrick Gold 2019 Annual Report [Mark Bristow is President of Barrick Gold]

Alternatively, or as part of this approach, mid-tiers can invest in junior explorers doing the same thing and come alongside them with the greater resources that they have available. The main advantage of this approach, for example, is that $100 million investments can become projects worth $1 billion or more which can lead to much higher returns on capital and exceptional returns for shareholders, even absent some kind of major metals boom. Another advantage of this approach is that it leads to personnel networks that can enhance the ability of the mid-tier producer to attract talent.

Lundin Mining has no development pipeline. Their approach is to periodically buy assets so their pipeline is backroom deals and investment bankers. One disadvantage to this approach is that it circumvents the community engagement and an acquirer can unknowingly inherit trouble. This may very well be a non-issue for Lundin though, but it is something to consider as new assets are brought on. This also begins to explain why Lundin has no Canadian mines.

Lundin’s approach may have some advantages when it comes to eliminating some early-stage project risks and reducing various administrative costs but this is negated by them always seeming to have to pay full price for quality assets. Management has exercised discipline executing this approach in recent years, notably by its decision to not overpay for Nevsun’s Timok mine, but the main problem remains that it puts a lid on capital returns unless they are able to discover exceptional new mines within the districts they acquire. They overpaid for Candelaria in 2014 and they are now shackled with low capital returns.

Quantitative Assessment

When analyzing mining companies, I focus a lot on their net income and/or free cash flow returns on capital. A simple formula that an investor can use is:

net income / total equity + long-term liabilities + current portion of debt (contained within short-term liabilities (if applicable)

You want to do this over a number of years and consider the impact of different metal price environments and large one-off exceptions that can skew net income.

As I have continued to include this approach with my overall assessment of all types of companies I have noticed that a stock tends to be a decent value when its forward price to earnings (P/E) ratio is below this return on capital.

Over the last 4 completed fiscal years—years with a wide range of base metals prices—Lundin has averaged 4.6%. In a $3 copper environment, Lundin is good for about 7% which implies that the current share price is just about right. (7% is also my rough estimate for just Candelaria which is also their flagship project.)

Key Takeaway

The key issue with these low capital returns is that the business will not generate enough retained earnings to build the cash reserves necessary for acquisitions absent higher metals prices. If Lundin takes on more leverage for acquisitions, its cost of capital will be higher and 4.6% is a low threshold. The problem is that the environment that brings the higher metals prices will be accompanied by investor enthusiasm for copper and miners selling projects will demand premium prices. Moreover, the Chinese may be willing to pay even more which is another reason why organic growth is a preferred strategy nowadays. This will keep Lundin trapped in a cycle of low capital returns and the associated poor shareholder returns that come with it.

Lundin needs to ditch the accountant strategy and start investing in early stage exploration and development to at least have the potential for returns. That is the bottom line.

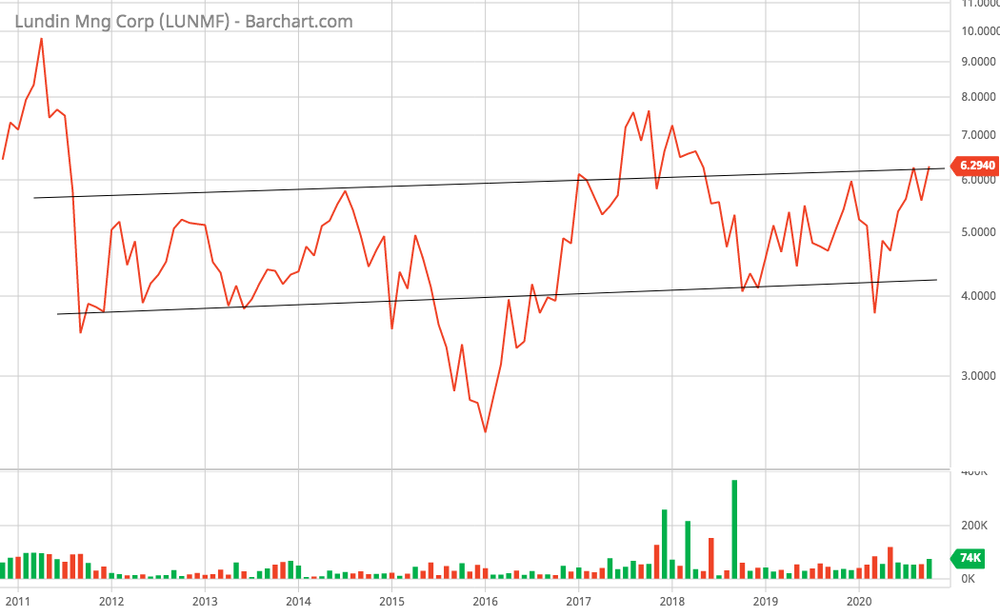

I will leave you with the following long-term, monthly log chart of Lundin’s share price in U.S. dollars:

(Click to view fullsize)

chart courtesy of Barchart.com

What we see here is a long-term range bound-to-gradually increasing chart pattern which echoes the low returns on capital that I have highlighted in this Letter.

Comments

Log in or sign up to join the conversation.