(Photo Credit: Tinou Bao)

Over the next three weeks we will get a read on the health of the US consumer, as a slew of retailers begin to report. This week the focus will be on the department stores, with Macy’s, Kohl’s, Nordstrom and J.C. Penney scheduled to report and provide their outlook for the holiday shopping season.

The retail sector is full of haves and have-nots this quarter. Despite saving more due to lower gas prices, wages haven’t improved much, causing consumers to carefully consider how they allocate their discretionary income. The National Retail Federation has already warned us not to expect a great holiday season; retailers will have to offer deep discounts in order to compete. Add to that unseasonably warm weather in the Northeast and Midwest, leading to a build up of fall and winter inventory at many of the apparel names. The departments stores in particular have been losing out to specialty retailers for the past couple of years. Here’s what expectations look like for the third quarter:

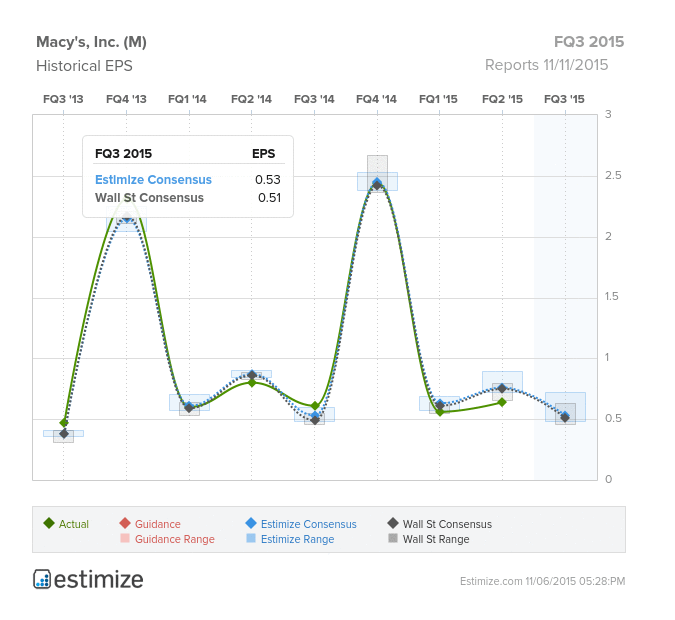

Macy’s (M)

Consumer Discretionary - Multiline Retail | Reports November 11, before the open.

The Estimize consensus calls for EPS of $0.53, two cents higher than the Wall Street estimate. Revenues of $6.162B are just slightly above the Street’s expectation for $6.155B.

What to watch: This year has not been kind to Macy’s which has reported two negative quarters of profits and revenues. The company blamed those losses on the West Coast port strikes, lower spending by international tourists due to the strong dollar, and weakness in key segments such as jewelry. Heading into the holiday season the company is focusing on many growth initiatives to boost performance. The department store has been refining their M.O.M strategy, which stands for My Macy’s localization (catering to different types of customers based on location), Omnichannel integration (helping customers shop seamlessly on-line and in stores) and “Magic selling” (improved customer service initiative). The company is rapidly expanding it’s beauty business through its acquisition of Bluemercury earlier in the year, and is also considering opening “off-price” locations like those of competitors Saks and Nordstrom. Several partnerships are also in the works, including one with Best Buy to make consumer electronics available in stores, and a collaboration with online fashion tech startup, Nineteenth Amendment.

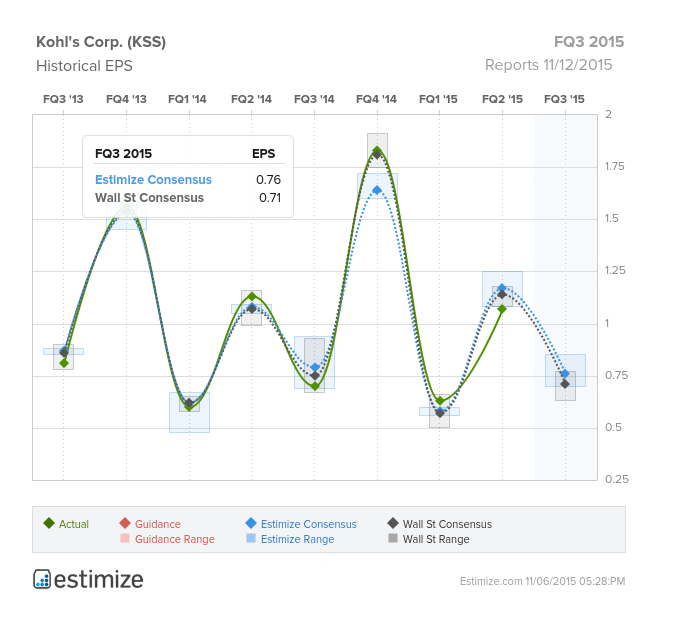

Kohl’s (KSS)

Consumer Discretionary - Multiline Retail | Reports November 12, before the open.

The Estimize consensus calls for EPS of $0.76, a nickel higher than the Wall Street estimate. Revenues of $4.464B are above the Street’s expectation for $4.445B.

What to watch: Kohl’s numbers came in light last quarter, with EPS missing by 10 cents and profits falling 5% YoY, estimates indicate growth will improve to 10% in Q3. Even more disappointing were the company’s same store sales figures, coming in at a measly 0.1%, after the company reported it was expecting to post 2 - 3% for the year. The blame was put on the shift of sales in tax-free states from July into August. This quarter should benefit from a strong back-to-school shopping season, with Kohl’s already announcing in August that their inventory receipts were “well-positioned for the back-to-school and fall seasons.” A series of new endeavors should also help, such as a revamping of their loyalty program (members are spending $80 more per year at Kohl’s than other shoppers), a personalized marketing campaign, and investments in omnichannel shopping ahead of the holiday season making it “easier than ever” to shop their website. Success has also been found in teen and women’s apparel collaborations with designer Lauren Conrad and brand Madden Girl. Like Macy’s, Kohl’s is also investing heavily in beauty, launching full-fledged beauty departments with top brands, and capitalizing on strength in that space. The department store will have to at least meet expectations for Q3 to avoid any further selling-off of its stock, which is already down 24% this year.

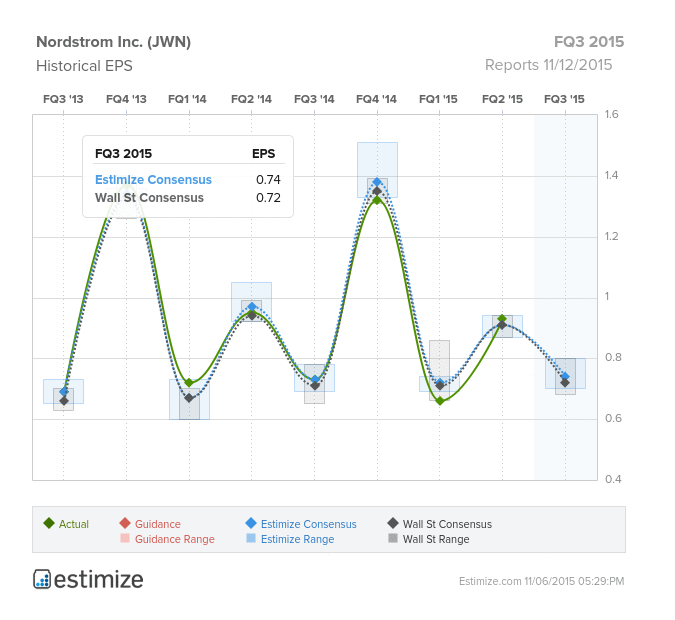

Nordstrom (JWN)

Consumer Discretionary - Multiline Retail | Reports November 12, after the close.

The Estimize consensus calls for EPS of $0.74, two cents higher than Wall Street. Revenues of $3.394B are slightly above the Street’s expectation for $3.388B.

What to watch: Muted expectations for Nordstrom only put YoY profit growth at 1.4%, a return to positive growth after 3 down quarters. In a surprising juxtaposition, revenue growth has actually been relatively strong, coming in at 13% and 12% for the first two quarters of the year. Of the department stores, Nordstrom is considered higher-end, a hard spot to sit as the US consumer becomes more value-focused and less willing to spend on apparel. However, same store sales have remained strong, coming in at 4.4% and 4.9% in Q1 and Q2, outpacing many of its competitors. A large part of the company’s success during the first half of the year can be attributed to Nordstrom Rack, Nordstrom’s discount store. That segment saw sales grow 13% in Q2, the 26th consecutive quarter of double-digit growth. Other initiatives such as the launch of Nordstromrack.com, entry into Canada and the acquisition of Trunk Club drove a third of total sales growth in the latest quarter and are expected to do so again in the third quarter.

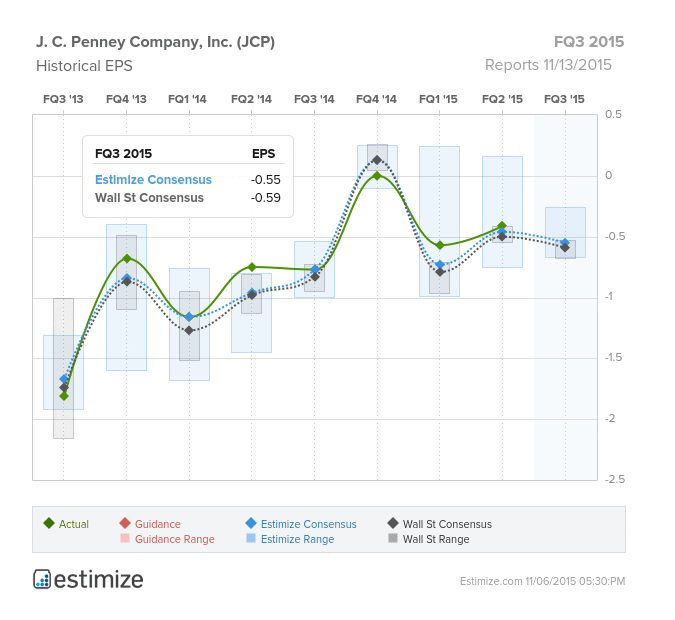

J.C. Penney (JCP)

Consumer Discretionary - Multiline Retail | Reports November 13, before the open.

The Estimize consensus calls for EPS of -$0.55, better than the Street’s expectation for -$0.59. Surprisingly, however, the Estimize community is more bearish on sales. Revenues of $2.850B are below Wall Street’s estimate for $2.869B, which would still be an increase on 3% YoY.

What to watch: Years later and J.C. Penney is still digging out from mistakes made by former CEO Ron Johnson, who replaced discounts and coupons with everyday low prices to the chagrin of loyal customers who have yet to fully return. While profit growth has been improving, in the high double-digits for the past 7 quarters, revenues have been very light, only in the low single digits. Same store sales has been a positive metric for the retailer, up 4.1% in Q2 and expected to be in the mid-single digits for Q3. The company has already commented on what they believe was a very strong back to school season, but will likely suffer from unseasonably warm weather. Like its competitors, JCP is investing in beauty by expanding the Sephora beauty shops within its stores and upgrading its beauty salons. The retailer recently announced its plan to cut 9% of the workforce at its headquarters in Plano, Texas. That decision came weeks after the company announced it would be reducing its pension obligation by 25% to 35% ($5B), a change that could affect up to 43,000 retirees and their beneficiaries.

Get your estimates in for these retailers here!

Comments

Log in or sign up to join the conversation.