In January and early February, the recession trade was on. U.S. economic data for Q4 was beginning to stream in and it was not pretty. Japan reported negative GDP (-1.4% initially, since revised to -1.1%) and the BOJ instituted negative interest rate policy. The data out of China was not good and continues to slip. Europe is well, Europe; a dead man walking in the global economy.

On all this bad news, market participants began to put on shorts in everything from commodities to junk debt to growth stocks. This move by institutional speculators pushed asset prices and indices to levels which have, in the past, indicated recessionary conditions. This prompted individual investors and some retail market participants to react to what the charts were saying and began to panic. It appears that little attention was paid to underlying economic and business conditions.

Beginning February 11th, when several OPEC and Non-OPEC members agreed (in principal) to production freezes the institutional short-sellers said: Enough!” The short-covering rally commenced. Once indices reached certain levels, investors and even some strategists believed that a sustainable recovery was in place. They, for the most part, ignored the possibility that the rebound in high yield debt, commodities and some areas of the equity markets were due mainly to short covering. Instead, retail money poured into high-risk assets. As usual, when retail plunged into risk assets, they plunged in after prices ran up a bit, This is supported by data, last week,from the high yield market that retail cash pouring into junk debt at a record pace.

Credit spreads of BB (H0A1) and CCC & lower (H0A3) vs. UST benchmarks (Source BAML):

For the past two weeks, I have been vocal that I am not a believer in the high yield debt rally. This is not to say that there are not good values to be found (based on suitability) in the high yield debt market. However, I am not a believer that junk debt is out of danger. This is because nothing has changed.

Critics might argue that much has changed. I.E. a U.S. recession is off the table. Actually, nothing has changed for me (and Bond Squad) because I was not a believer in the recession story in the first place. I am also not a believer in a growth acceleration story or the OPEC story. We must consider the following:

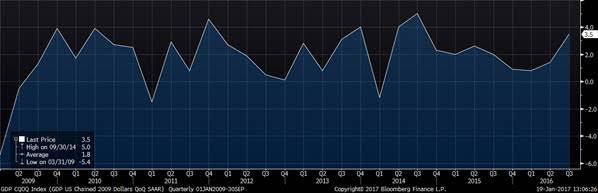

- The U.S. economy has rebounded to 2.0%-area growth. The Atlanta Fed’s GDPNow forecast is calling for 2.2% Q1 U.S. GDP. This might actually be a little hot as there is some catch-up from a weak Q4 2015. However, it is probably only a little hot.

- OPEC is a toothless tiger. Yes, OPEC could cut production and oil prices could approach $50, in a best case scenario, but as WTI approaches $40 per barrel, U.S. shale production that has gone off line will probably come back.

- European economic data continues to falter. Japan is dead in the water, with Q4 GDP printing a revised -1.1% (up from -1.4%). China continues trying to keep its crippled economy flying with contradictory policies. China’s exports fell 25.4% as its largest export customers, including the EMU and Brazil, continue to founder.

- The U.S. economy continues to glide along. If the U.S. economy was a motorcycle, it could be described as a touring bike (Road King, Goldwing, etc.). It is large, steady, and fairly-comfortable, and will travel along with little fuss. However, market participants, investors and some strategists continue to expect the U.S. economy to eventually speed along like a sport bike (GSXR, CBR, etc.). This is probably not realistic at present, but at least the U.S. economy is not a 50cc scooter like Japan and Europe. It is also not China, a sport bike clone with a powerful engine, but suspect brakes and suspension.

Thus, I believe that high yield debt and commodities could be reflecting overbought conditions. I would not be surprised if we learn that the sellers on the other side of retail buys are institutional speculators re-entering short positions.

I read a marketing piece published by a fixed income portfolio manager (SMA) which argued that junk debt looks attractive because the last several times high yield credit spreads have widened-out like they have in recent months, they represented buying opportunities. However, there is a significant difference between then and now. In the past, when high yield credit spreads widened as they have in recent months, a cathartic even occurred (credit defaults) which cleansed the market. This has not occurred this time around. As such, I believe that there should be another round of spread widening to reflect the eventual cleansing of the credit markets.

If one can carefully select bonds which are suitable for their specific purposes and ride out the volatility, there appears to be some value in the BB, crossover and BBB areas of the corporate credit markets, but to invest in this area of the fixed income markets one must be able to ride out more potential volatility and have the ability to hold until maturity. Contact me directly to discuss this further.

Comments

Log in or sign up to join the conversation.