Strong/ Weak Index October 3, 2017

Highlights:

- The Reserve Bank of Australia held rates at 1.5% as Philip Lowe left AUD Bulls wanting. There was little hawkish fodder as the unchanged statement argues that Bank is not yielding to the global tightening approach taken by the Bank of Canada, Bank of England, and other central banks. On the positive, Lowe did highlight the rise in capacity utilization as investment outside of mining has picked up. The immediate affect was a near 0.5% drop in AUD/USD, which bounced into the London/US session. The earliest priced in hike by the RBA is July ’18.

- JPY weakness remains a focus for many traders as yields push higher and equities around the world trade at record levels. In such an environment, JPY weakness appears to be the path of least resistance. Overnight, USD/JPY traded to 113.20 and within a whisper of the Sept. 27 high of 113.27. Insight from the options market is showing JPY calls (USD/JPY lower) are finding good demand with expiries near the Oct. 22 election in Japan. Therefore, if the election passes without a negative surprise to the market, we could see a sharp unwind of the bearish USD/JPY (JPY long) trade, and a move higher ensue. Per sentiment, this would likely play nicely on the SW pair, GBP/JPY with a sharp increase in weekly net-long exposure of ~50%.

- The EUR has been able to pair some of Monday’s losses despite the Catalonia independence fight from Spain persisting. The key level a lot of traders are watching with EUR/USD is the August 2015 high of 1.1714. A close below 1.1714 would open up short-term support at 1.1662, and a break further still could signal a larger Bullish move developing in the US Dollar Index while EUR longs unwind.

- The New Zealand Dollar continues to lose ground with the short-term reason being a disappointing milk auction, which argues further for the RBNZ to remain on hold. The medium-term scope for a weaker NZD is the counting of special votes on October 7th for the formation of the new government. NZD/USD has fallen nearly 4% since September 20th, and a further breakout in USD could see a test sub-0.7000.

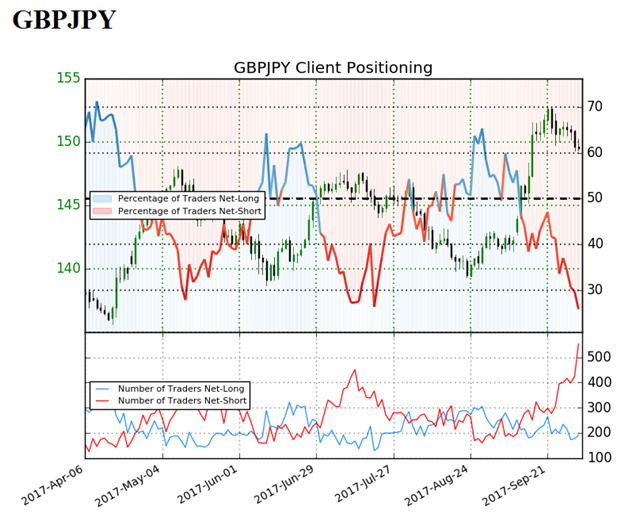

IGCS Highlight: Sharp rise in GB/JPY shorts favors SW trend continuation

GBPJPY: Retail trader data shows 25.8% of traders are net-long with the ratio of traders short to long at 2.88 to 1. In fact, traders have remained net-short since Sep 22 when GBPJPY traded near 152.636; price has moved 2.1% lower since then. The number of traders net-long is 2.5% lower than yesterday and 10.3% lower from last week, while the number of traders net-short is 28.7% higher than yesterday and 48.8% higher from last week.

We typically take a contrarian view to crowd sentiment, and the fact traders are net-short suggests GBPJPY prices may continue to rise. Traders are further net-short than yesterday and last week, and the combination of current sentiment and recent changes gives us a stronger GBPJPY-bullish contrarian trading bias (emphasis added.)

Comments

Log in or sign up to join the conversation.