The latest JOLTS report (Job Openings and Labor Turnover Summary), with data through July, is now available. From the press release:

The number of job openings increased to 6.6 million on the last business day of July, the U.S. Bureau of Labor Statistics reported today. Hires decreased to 5.8 million in July. Total separations was little changed at 5.0 million. Within separations, the quits rate rose to 2.1 percent while the layoffs and discharges rate decreased to 1.2 percent. These changes in the labor market reflected an ongoing resumption of economic activity that had been curtailed due to the coronavirus (COVID-19) pandemic and efforts to contain it. This release includes estimates of the number and rate of job openings, hires, and separations for the total nonfarm sector, by industry, and by four geographic regions.

Job Openings

On the last business day of July, the number and rate of job openings increased to 6.6 million (+617,000) and 4.5 percent, respectively. Job openings rose in a number of industries, with the largest increases in retail trade (+172,000), health care and social assistance (+146,000), and construction (+90,000). The number of job openings increased in the South and Midwest regions. (See table 1.)

Coronavirus (COVID-19) Pandemic Impact on July 2020 JOLTS Data

Data collection for the Job Openings and Labor Turnover Survey was affected by the coronavirus (COVID-19) pandemic. More information is available at the end of this news release and at www.bls.gov/covid19/job-openings-and-labor-turnover-covid19-july-2020.htm.

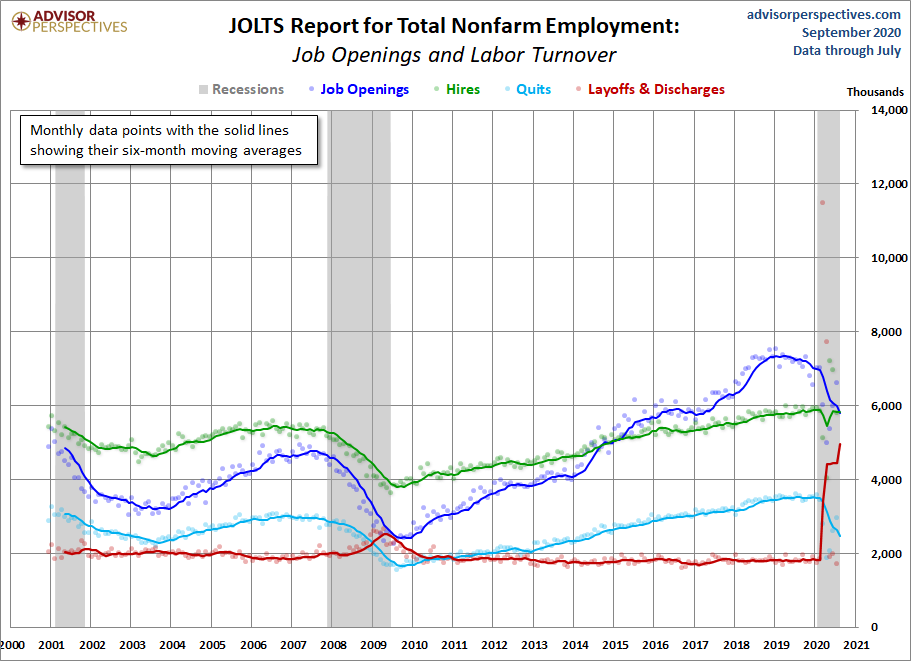

The first chart below shows four of the headline components of the overall series, which the BLS began tracking in December 2000. The time frame is quite limited compared to the main BLS data series in the monthly employment report, many of which go back to 1948, and the enormously popular Nonfarm Employment (PAYEMS) series goes back to 1939. Nevertheless, there are some clear JOLTS correlations with the most recent business cycle trends.

The chart below shows the monthly data points four of the JOLTS series. They are quite volatile, hence the inclusion of six-month moving averages to help identify the trends. The moving average for openings was above the hires levels for over five years, as seen in the chart below. The openings MA dipped below the hires for a brief two months (May and June 2020), only to climb above once more in July.

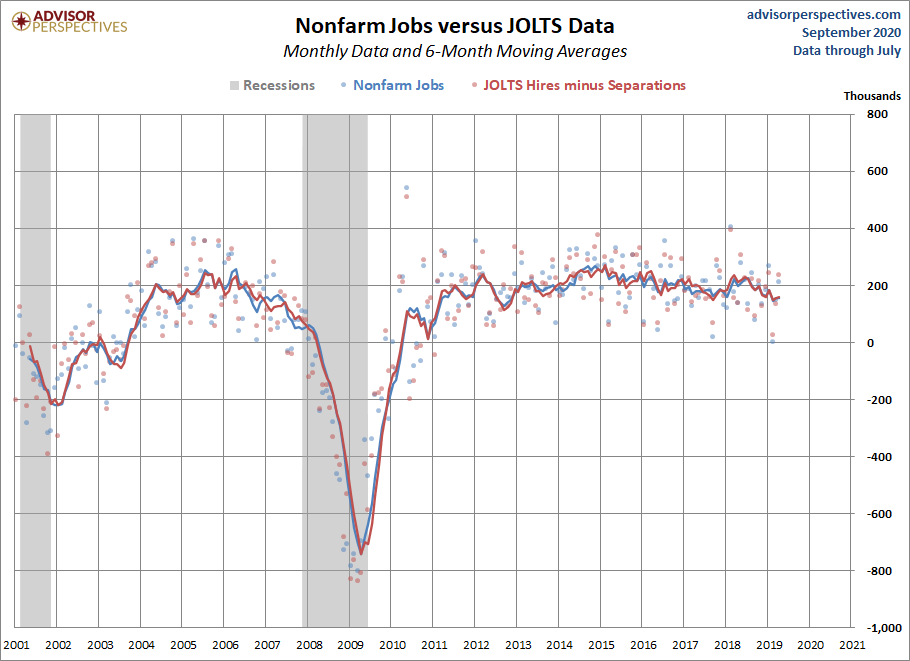

For comparison, here is the monthly BLS Employment Situation Summary charted with JOLTS data:

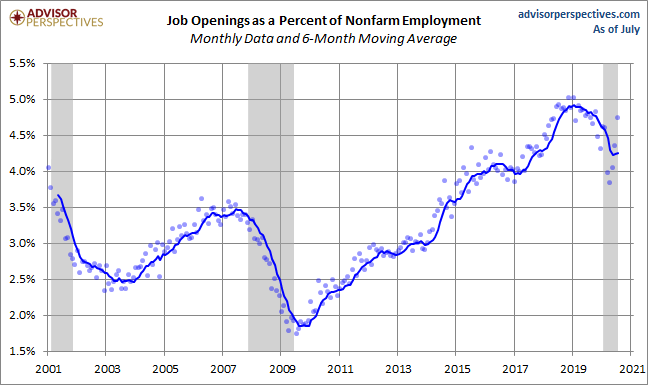

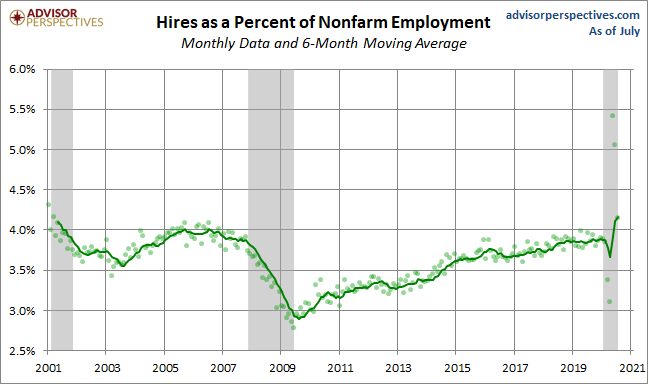

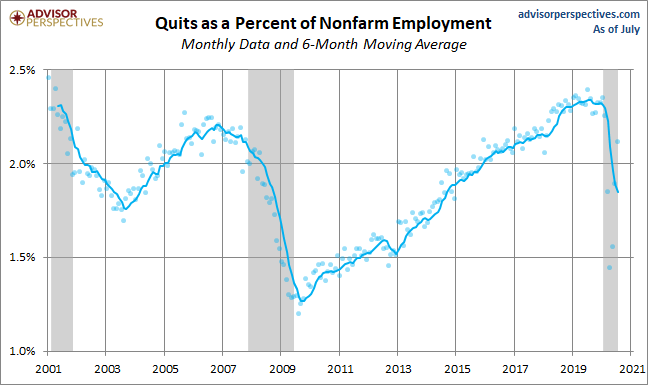

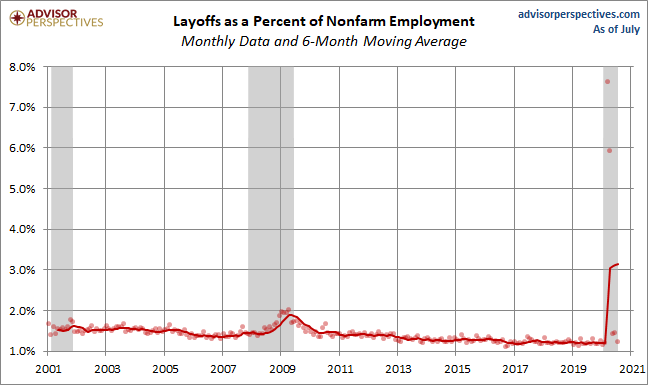

A Population-Adjusted Perspective on JOLTS

The chart above is based on the actual numbers in the JOLTS report. A better way to view the numbers is as a percent of Nonfarm Employment, which essentially gives us a population-adjusted version of the data. Here is that adjustment for four of the JOLTS series. Note that the vertical axis for each is optimized for the high-low range to facilitate an understanding of the individual trends.

Where Are We Now in the Business Cycle?

Based on the six-month moving averages, we can see that:

- Openings are at levels last seen in 2017 and the moving average is above the hires levels after two months below.

- Hires are at their all-time high.

- Quits have fallen to levels last seen in 2015.

- The Layoffs and Discharges series is at its all-time high.

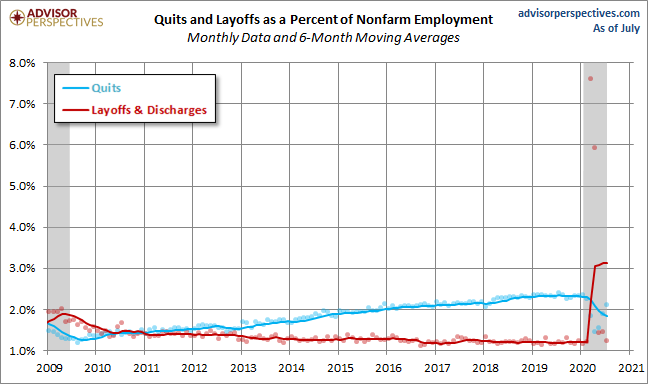

The Trend in Quits

To reiterate a previous point: Increases in Quits suggest employment flexibility. Quits tend to be inversely correlated with Layoffs & Discharges, which are associated with business cycle weakness. Following the last recession, Quits began increasing in 2010, and the rate accelerated in 2013 and continued to rise. Layoffs & Discharges fell post-Great-recession and leveled out for many years. Due to the COVID-19 pandemic, layoffs and discharges are seeing an all-time high.

It would, of course, be excellent if we had historical JOLTS data stretching back through several business cycles. But alas we do not.

The JOLTS reports will be interesting to watch in the months ahead. But the volatility of the data, which is also subject to revisions, encourages caution in taking the data for any given month very seriously.

Comments

Log in or sign up to join the conversation.