Jaded Investors

Investors who follow the fundamentals have become jaded. You can tell because there were discussions on FinTwit about how the stock market would rise after the weekend protests and riots. These investors are wrong to suggest the fundamentals don’t matter and they have recency bias.

We are faced with an extremely overbought market and a negative event, yet investors still don’t believe a correction is coming. They feel this way because the stock market has been ignoring COVID-19 and the terrible economy. Their mistake compounded.

The stock market should have rallied off the March low because we are learning more about COVID-19 and how to limit its growth. That reduces uncertainty. Secondly, we know the economic openings will help the economy recover since COVID-19 is the only reason the economy is in a recession.

Traders like to jump the gun which means they price in a recovery before it happens. Stocks had already rallied significantly before the first decline in continuing claims came out. In other words, traders made a correct opinion that the economy would recover.

To be clear, in the past couple weeks the rally has gone overboard. A problem jaded investors have is they think the entire rally shouldn’t have happened. It’s easy to feel this way if you didn’t buy stocks in late March. You needed to fight that urge and buy stocks in April even after they had rallied significantly.

Now that the stock market is about to fall because it is overbought and the riots are shutting down cities, these jaded investors won’t take advantage of the pullback, just like they didn’t take advantage of the prior corrections. Even if stocks fell 10% from here, they wouldn’t buy.

Tech Stocks Are Too High

There is extreme recency bias and a heard mentality when it comes to tech stocks. I spoke to a trader who was advising people to go long Apple with leverage. I think that’s a big mistake as it’s a crowded trade. There is a lot of truth to what is driving mega-cap tech and cloud stocks higher. Most bubbles are based on truth.

For example, the 1990s tech bubble predicted how important tech would become. Problem is many of those businesses didn’t survive to benefit from it. Furthermore, the ones that did survive were very expensive. They needed to grow profits for years to justify such valuations. They eventually became really cheap in the late 2000s.

Shopify is doing better than it ever has, but the valuation is so optimistic that even in the best-case scenario, the stock won’t provide investors with great long term returns. Personally, I like to buy stocks where even in the worst-case scenario the stock is a hold. Even if a lot of things go wrong, the stock still won’t crash. Valuations are extremely important. You know the bubble has gotten out of hand when very few tech investors care about valuations.

Cloud investors aren’t worried about competition. It’s amazing how investors own 10 cloud firms and don’t realize they all will compete. To be fair, when a business has a high retention subscription service that increases services to existing customers, it’s a great sign. Furthermore, the trend of digitizing businesses is only just beginning. However, whenever everyone agrees with you on an uncertain topic, you must consider running away.

For example, if you are bullish on oil and no one even questions that stance, it’s time to sell. Trends tend be near their end when no one would even question it ending. Only people who are bearish on Amazon are the ones who haven’t liked it for years. However, once it starts falling, shaky investors will sell out, creating volatility.

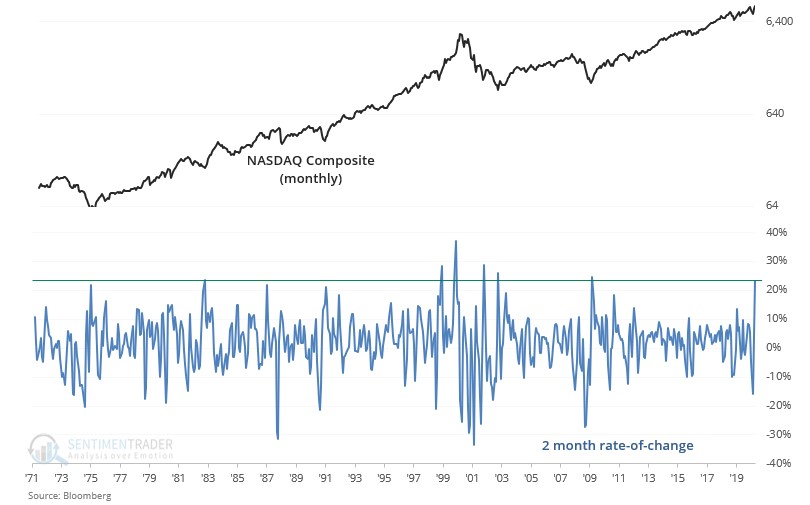

Recent Momentum

As you can see from the chart below, the 2 month rate of change of the Nasdaq composite (monthly) is the highest since 2009 which was the start of the last bull market. Since 1970, this reading has been reached 6 times. 4 of those were before and after the tech bubble.

Obviously, Nasdaq components weren’t the same types of businesses in the 1970s and 1980s as they are now. Regardless, it’s clear this rally has gone too far. At the very least, the speed of the rally will diminish. Question is if the next correction is the start of a large decline or if it will quickly be reversed.

Extreme SaaS Valuations

To answer the question about whether this is the start of a minor correction in tech stocks or a major bear market, I have the chart below which shows SaaS valuations. As you can see, the equal weighted enterprise value to next 12 months revenue multiple for SaaS stocks has skyrocketed to 20.4 as of May 15th. That’s above the peak last year of 15.2 and much higher than the 5 year average of 9.5. It’s probably even higher now than it was 2 weeks ago.

Equal weighted index is double its average multiple. That’s because the smaller cloud stocks have exploded the most. They have higher valuations because they have faster growth and more potential. However, they also have the most risk and the most uncertainty. These firms aren’t profitable and face increased competition. Their operating leverage increases as they grow.

A question is whether they can reach profitability before competition erodes margins. Many would rather buy the dominant firms that are already profitable. Anaplan is one of the cloud firms that isn’t profitable yet. Analysts don’t even expect it to be profitable in 2023. I won’t get exuberant over a company that won’t be profitable for years because one bad quarter can tank its stock.

Conclusion

Sentiment is clear. Investors who are bearish on the fundamentals are resigned to thinking stocks will go up no matter what. That’s a sign a correction is coming. If stocks rally this week, the NAAIM investor exposure index will give off an extreme reading.

As the economy reopens, the positive momentum the work from home cloud plays have had will fade. You need to expect extreme volatility when you buy an unprofitable firm or a commodity stock. Valuations for cloud stocks are out of line. They will underperform in the next 6 months to a year.

Comments

Log in or sign up to join the conversation.