I’ve Got a Secret was a TV game show that aired from 1952 to 1967, where debonair white people would smoke cigarettes, sport bow ties and ermine stoles, and crack wise as they quizzed “contestants” about their secret pastime or accomplishment. My god, how I miss Kitty Carlisle.

Anyway, I thought a lot about I’ve Got a Secret when I saw the recent financial media brouhaha over Michael Burry and passive investing. But probably not for the reasons you think.

The Big Short’s Michael Burry Sees a Bubble in Passive Investing [Bloomberg]

“The bubble in passive investing through ETFs and index funds as well as the trend to very large size among asset managers has orphaned smaller value-type securities globally,”

The Big Short’s Michael Burry Explains Why Index Funds Are Like Subprime CDOs [Bloomberg]

“Central banks and Basel III have more or less removed price discovery from the credit markets, meaning risk does not have an accurate pricing mechanism in interest rates anymore. And now passive investing has removed price discovery from the equity markets. The simple theses and the models that get people into sectors, factors, indexes, or ETFs and mutual funds mimicking those strategies — these do not require the security-level analysis that is required for true price discovery.”

Okay. Whatever. The whole index-funds-are-like-subprime-CDOs thing is silly, but that’s the headline writer setting this article up for clicks. Burry – like every small cap value investor since the dawn of time – is saying that the market doesn’t appreciate the information he’s uncovered about his small cap value stocks, and that there are structural reasons why the market doesn’t appreciate that information. Not exactly fighting words.

But judging from the reaction on Fintwit and elsewhere in the financial blogosphere, you would have thought that Michael Burry had run over someone’s dog.

It’s the reaction to the Michael-Burry-says-passive-investing-is-a-bubble stories that made me think of I’ve Got a Secret.

I mean, you had celebrated former-alpha-guy-turned-asset-gatherer Cliff Asness leap to Twitter to call Burry a “monkey who typed Hamlet” (but don’t worry, it’s okay to say this because it was done in a self-deprecating way), “histrionic”, and full of “inarticulate nonsense.” I lost count of all of the urgent “debunking” blog posts to the Michael-Burry-says-passive-investing-is-a-bubble story.

It’s just weird.

To be fair, it’s also weird how passive investing becomes the scaffolding for any number of Grumpy Grandpa strawman positions, most notably the “this will blow up ANY DAY NOW” argument, the “those darn computers!” argument, and the “in praise of index-hugging active managers and their … [checks notes] … price discovery” argument. I claim zero association with those positions in what I’m about to say, so don’t @ me.

There IS a bubble here. It’s a behavioral bubble I’ll call ABB.

Always. Be. Buying.

And the Common Knowledge surrounding passive investing – what everyone knows that everyone knows about passive investing – is what blows this bubble.

Everyone knows that everyone knows that passive investing beats active investing.

Everyone knows that everyone knows that stocks as an asset class ALWAYS go up over time.

And if that’s the case, then why in the world would you pay more for someone to use their discretion in picking this stock or that stock? No, no … just harvest the inevitable returns that stocks in a general sense ALWAYS provide by putting your money in an inexpensive, systematic buying program. If you think yourself particularly clever, then by all means express this systematic buying program in terms of “factors” or “betas” instead of this index or that index, but the important thing is to ABB.

Index funds and any other passive investment vehicles are really important, excellent things for investors. I get that. I am not railing against their existence.

But you cannot separate the Always. Be. Buying. impulse from index vehicles and pretend that they are just the intellectually simple, straightforward expression of market exposure that they are in theory. They are loaded with “be long” MEANING for everyone.

THAT’S THE BUBBLE.

Now I know this will come to a shock for many, but there was a time when this was not the accepted faith of markets.

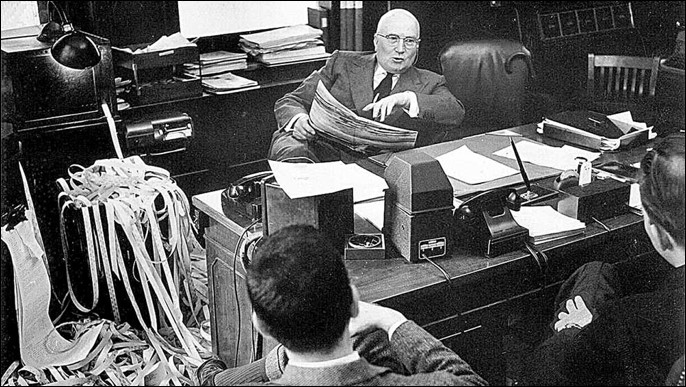

Gerald Loeb, co-founder of E.F. Hutton, happily immersed in the tape.

This is a picture of Gerald Loeb, who co-founded E.F. Hutton and was Warren Buffett-level famous back in the 1950's and 1960's … back when I’ve Got a Secret was in its heyday. And this was The Secret about markets that Gerald Loeb thought he knew:

Buy and hold is for chumps.

In the 1950s and 1960s, everyone knew that everyone knew that Gerald Loeb was right. This was the investment Common Knowledge of the day. This was the gospel and the MEANING of the business of Wall Street.

No one remembers Gerald Loeb today.

Which is a shame. But not surprising.

Did Gerald Loeb know The Secret to markets? Of course not. But did Gerald Loeb know A Secret to markets? Yes, he did. And did his secret WORK for the markets of his day? Absolutely. Would his secret work TODAY in a different Common Knowledge environment? Not a chance.

Do YOU know The Secret to markets, that stocks as an asset class ALWAYS go up over time?

Or do you know A Secret to markets, one that works because it is the Common Knowledge of the day?

I think it’s the latter. Which means it will work until it doesn’t. Which means it will work until the Common Knowledge changes.

That’s my Secret about markets. It’s far from Common Knowledge. But pass it along and let’s see what happens.

Comments

Log in or sign up to join the conversation.