- What is behind the negative sentiment in risk markets?

- FOMC meeting minutes suggest a slower pace of tightening than “Fed Dots.”

- Challenger Job Cuts data hit lowest level in 15 years. Is the economy in late cycle?

- The 10-year UST yield remains below 2.20%, in spite of EM central bank selling.

- China removes circuit breakers following a 29 minute equity trading session.

Numbers:

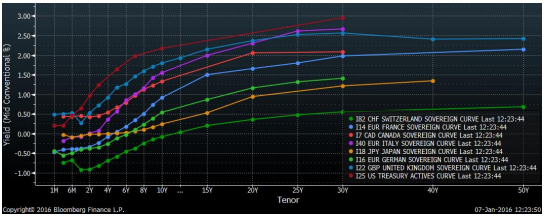

Yield Curves:

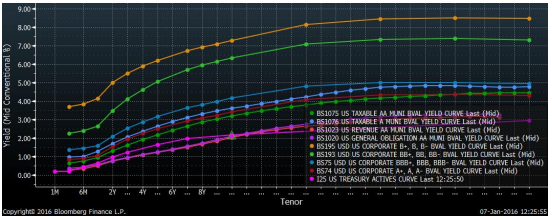

Credit Curves:

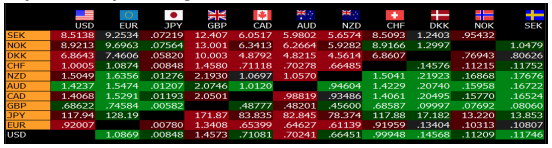

Major Currency Exchange Rates:

Making Sense:

Equity market strategists are scrambling to get time on nearly every media outlet to do damage control on their (in my opinion) overly bullish calls. However, I find myself sympathizing with the equity folks. Economic conditions in the U.S. are not terrible. China is slowing and should continue to experience growing pains for years to come, but is unlikely to implode. Just as the risk markets were overly bullish on unrealistic perceptions, the downturn among risk assets is, in my opinion, more of a change in perception than any real changes in the global economy.

It’s all in the Mind

The problem in the risk asset markets (equity, EM and HY bonds) is that market participants, strategists and analysts relied on mean reversion to make their forecasts. They assumed that low interest rates would fuel growth based on leveraged spending. They assumed that China would grow at 8.0% to 10.0% ad infinitum. They assumed that the size of China’s economy would grow unabated and demand for commodities would grow accordingly. It was assumed that Chinese leadership knew what it was doing when it was building so-called ghost cities. Capital markets have become convinced that government policymakers could engineer sustainable recoveries without economic bubbles. This in spite the fact that this has never happened before. During the past two years, the bond market has been sending out warnings that global and U.S. growth were in danger of slowing. For two years, equity market participants and media pundits 3 have questioned what the bond market was seeing or simply called the bond market “wrong.” The evidence is in and it says that the bond market was not wrong. The bond market is pricing in 2.0%- area U.S. GDP, inflation settling in to the mid-1.0% area, developed foreign markets underperforming and China maturing and growing at a slower pace (thereby hammering EM commodities producers). Now investors and market participants are asking: When will markets and economies recover and normalize? In my view, low long-term interest rates and bumpy equity markets are closer to the new normal conditions than many market participants believe. The Bond Squad outlook is: Focus on quality, rein in your expectations for investment performance in 2016 and avoid the temptation to invest for 2016 annual returns. Depending on suitability (goals objectives and risk tolerance), opportunities are out there, but they are probably multi-year stories. I am avoiding adding to high yield at the present time. Although the high yield market may look attractive, it could look even more attractive in the coming weeks or months. I would rather miss the bottom than catch falling knives. I see no reason to be a hero at the present time.

Slow Ride, Take it Easy (clearing the fog)

If volatility persists and economic data disappoints, look for the Fed to moderate its rate hike forecast. My base case still calls for two rate hikes in 2016, but there is greater risk for fewer hikes rather than more rate hikes. In my view, popular inflation expectations are misguided. Yes, headline inflation data should rise as the year over year deflationary forces from energy prices abate, but the result should be a convergence of headline and core inflation rather than both measures moving much higher. According to the December FOMC meeting minutes, Fed officials agree. Some takeaways from the minutes were:

- The December FOMC meeting minutes were almost dovish in tone. Fed officials favored a gradual approach. FOMC members emphasized need to adjust path of policy as economy evolves, “and to avoid appearing to commit to any specific pace of adjustments”

- Some Fed officials said that it would “probably take some time” for data to confirm that inflation would return to 2% over “medium term.”

- A Gradual approach to tightening would allow the FOMC to adjust course as the data comes in.

- The minutes indicated that although most Fed officials believed conditions for tightening were met, the decision to tighten was a close call.

- The minutes emphasized that the Fed is committed to a gradual pace of tightening as the neutral short-term real interest rate was seen as close to zero at the present time and was expected to rise “only slowly” as headwinds recede.

The minutes clearly indicated that Fed tightening should be gradual. What caught my attention was the belief that headwinds would recede. The Fed has gone out of its way to portray low inflation and slower GDP growth as transitory. They probably will be transitory. Everything is transitory and subject to change. The Ice Age was transitory, but it lasted a heck of a long time. I expect that the Fed’s transitory headwinds could be longer lasting and far more structural than the Fed believes. We shall soon see.

Can’t Dodge Challenger (Gray and Christmas)

No surprises in today’s Initial Jobless Claims data. Initial Claims for the week ended January 2 nd came in at 277,000. This was down from a prior 287,000, but was slightly higher than the Street consensus of 275,000.

Challenger Job Cuts fell 27.6%. According to data provided by Challenger Gray and Christmas, job cuts are at a 15 year low. John Challenger opined that the data indicate the economy is near full employment. If one believes (as I do) that the majority of the people who have left the labor force will not return, then the economy might be at full employment. Although this could result in a moderate pickup in wages, it may also signal that the economy is later in its expansion cycle than previously thought. Mr. Challenger stated that the data indicate that an economic recession could be on the horizon, in two years or so.

The economy is already experiencing a manufacturing recession and could fall into an earnings recession. The major concern for Bond Squad is that contagion could materialize and infect the broader U.S. economy. There are signs of contagion in recent data, but whether or not there will be sufficient contagion to drag the broader U.S. economy into recession is questionable at the present time. A broader U.S. recession is not my base case scenario, but 1.75% to 2.25% 2016 U.S. GDP is.

“So if you wake up with the sunrise, and all your dreams are still as new “

At the time of this writing, the yield of the benchmark UST 10-year note stood at 2.18%. This is just one basis point higher than where the 10-year note yield ended 2014 and 9 bps lower than it ended 2015. Maybe the bond market is “wrong” on its outlook for GDP and inflation, but I doubt it. My view is; if China was not trying to stem the slide of the yuan (renminbi) and other emerging central banks were not trying to defend their currencies, long-term UST yields would be even lower than they are today.

Tonight’s the Night

This morning, China announced it was removing stock market circuit breakers. This was after selling pressure tripped circuit breakers overnight, resulting in a 29 minute trading session. The removal of circuit breakers is in response to criticism that China was preventing price discovery. U.S. 5 equity markets reacted positively to the news on the hope that a removal of circuit breakers would enable buyers to enter the market after a downturn and establish price discovery. Tonight should be interesting. Bond Squad will be paying close attention.

Comments

Log in or sign up to join the conversation.