UroGen Pharma Ltd. Company (Pending:URGN) filed for its IPO on April 7, 2017, outlining its plans up its IPO.

The company is excepted to go public this Thursday, offering 3.46 million shares at an expected price range of $12 to $14. It has an additional 519,230 shares available for purchase by underwriters. The company expects to raise $48.5 million ($55.7 million if the underwriters exercise their option to purchase additional shares).

Company insiders have indicated interest in purchasing $20M worth of shares in the offering. Although this is not binding, it is a positive signal.

Assuming it prices at the midpoint of its price range, it would have a market capitalization of $150 million.

Underwriters for the IPO include: Cowen & Company, Jefferies LLC, Oppenheimer & Co., and Raymond James & Associates

Business Summary: Clinical-stage Biopharmaceutical Developing Treatments for Urological Diseases

UroGen Pharma is a clinical-stage biopharmaceutical company focused on developing treatment for urological disorders and diseases. Its leading product candidate are VesiGel and MitoGel, which are formulations based upon the chemotherapy drug Mitomycin C. Mitomycin C is currently prescribed off-label for urothelial cancer as a supplemental post-surgery treatment. UroGen is developing its product candidates as chemoablation agents, which means it is designed to remove tumors without surgery (typically required in current treatment method). The objective is to treat several forms of invasive urothelial cancer, low grade bladder cancer, and low-grade upper tract urothelial carcinoma.

Because product candidates are based on novel formulations of already approved drugs, it hopes this will enable them to streamline regulations more quickly.

In 2016, UroGen Pharma entered into an exclusive license agreement with Allergan Pharmaceuticals. The company received $17.5 million and is eligible to receive additional milestone payments in the future. Allegan will be responsible for developing, securing regulatory approvals, and marketing the licensed products globally and UroGen will receive tiered royalties on global net sales.

Currently, the annual expenditures in the United States for the treatment of urothelial cancer is about $4 billion. That number is expected to increase to a minimum of $5 billion by 2020. However, the FDA has not approved any new treatments for these urological diseases in over 15 years.

Executive Management Highlights

Ron Bentsur has served as CEO since August 2015 and director since October 2015. His previous experience includes executive positions at Stemline Therapeutics, Keryx Biopharmaceuticals, Leumi Underwriters, and ING Barings Furman Selz. Bentsur holds a B.A. in Economics and Business Administration from the Hebrew University of Jerusalem, Israel and an M.B.A. from New York University's Stern School of Business.

Gil Hakin has served as President since August 2010. His previous experience comes from senior positions at Medispec, MTRE Advanced Technologies, Omrix Biopharmaceuticals, and Biosense-Webster. Hakim holds a B.Sc. in Life Sciences from Ben-Gurion University, Israel.

Financial Overview

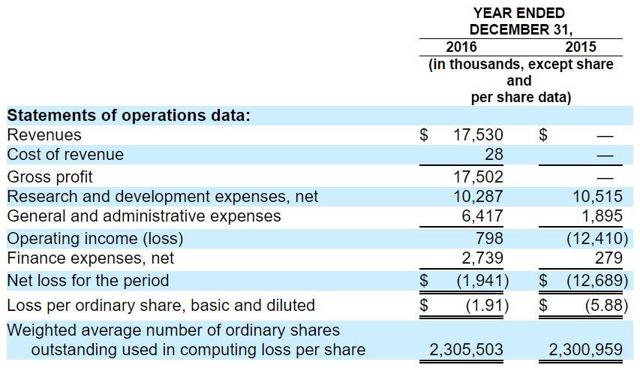

The company has incurred net losses since its inception in 2004, and none of its current product candidates are available for commercial sale. The company incurred net loss of $12.7M and $1.9M in 2015 and 2016. As of December 31, 2016, the company's accumulated deficit was $27.2 million and cash/ cash equivalents of 21.3M. Revenue generated in 2016 was $17.5M, all from the exclusive license agreement with Allergan Pharmaceuticals.

UroGen intends to use the net proceeds of this IPO to fund further clinical trials for its product candidates and expects expenses associated with clinical trials to increase substantially.

(F-1/A)

Conclusion: Consider a Modest Allocation

Projections for significant growth in the market is uplifting, however competition in the industry is strong with several other notable biopharmaceuticals developing therapies for urological diseases (i.e. Handok Inc., Taris Biomedical, Spectrum Pharmaceuticals).

The partnerships with Allergan and the interest of insiders in purchasing close to half of the shares in the offering, make up optimistic about that the company with have a successful market debut.

However, to continue growth, it will need further capital and continued success in its trials.

We are hearing that the deal is oversubscribed and building.

We recommend no a modest allocation given the risks laid out above.

Comments

Log in or sign up to join the conversation.