Here are some things I think I am thinking about this weekend.

1) Is the Stock Market a New Bubble?

There’s a lot of bubble talk brewing again. We’ve covered this topic a lot over the last 15 years and my general conclusion is “there’s a bubble in bubble calls”. But maybe this time is different? Or maybe not? Let’s explore.

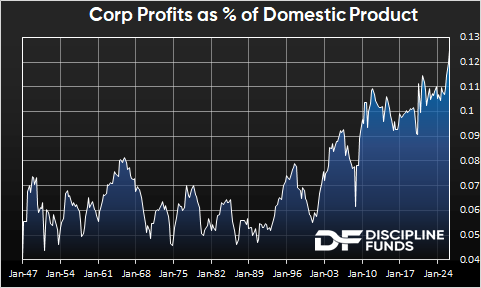

To me, a bubble is an irrationally priced market with no sustainable fundamental basis for being able to continue its prior price momentum. What results is a market that is so detached from reality that it must collapse back down to much lower values before it can find a sustainable floor for continued appreciation. In my opinion, the problem with today’s market and the “bubble” narrative is that it’s very fundamentally driven. The AI trade is causing corporate profits and margins to blow out to record levels. Here’s the latest on profits as a percentage of domestic product:

People wonder why US valuations have surged in the last 40 years and whether they’re sustainable. Well, as long as this chart remains elevated the way it has been in the last 20 years, yes, high valuations are warranted. I think people too often look at charts of valuations and say “well, this is the same level as 1999 therefore we must collapse”. That’s a pretty loose conclusion.

At the same time, I wouldn’t necessarily downplay the worries. When expectations surge like this the margins for error thin. So, I’d also argue that someone with a short time horizon has to be careful being overly expose to high valuation and high growth names. The way I think about it is that the reliable time horizon over which an asset might recover becomes longer when its valuations expand. It becomes riskier because its expected returns increase which means that if the asset disappoints for any reason it causes you significantly more sequence of return risk.

This is what I love about viewing asset allocation through time horizons. To me, an international value sector is a completely different animal than a US growth sector in today’s environment. It doesn’t mean the US growth sector is wrong to own today. But if the foreign value sector has a Defined Duration of 15 and the US growth sector has a Defined Duration of 25 and you have a 15 year time horizon then you just need to be more thoughtful about how much exposure you have to that 25 year instrument. On the other hand, if you’re a 20 year old with a 50 year time horizon then you should probably be loaded to the gills with growth. It all depends on your time horizons.

So, I think two things can be two here:

This market is not a bubble because it has real fundamental drivers underlying it.

This market is riskier in certain elements because the expectations embedded in certain sectors are very high which reduces margin for error and creates potentially higher sequence risk.

2) Are Bond Yields Going Even Higher?

Bonds are getting dinged again as inflation expectations tick a bit higher. That’s not totally surprising given the continued surge in oil prices. The market had been expecting rate cuts with a new Fed Chief, but now the expectations have flipped. Despite this, I think a little nuance is required to put this in perspective because a reversal in expectations doesn’t suddenly mean bonds are going to blow up.

There has been renewed chatter in recent weeks that we’re headed back to the 70s (again). People love this chart from Larry Summer showing the 2014 starting point compared to the 70s. As if there’s some sort of temporal relationship between the two time periods because…because!

Are we going to get another big surge in inflation? We’re seeing a surge! It’s surged from 2.4% to 3.8% in just 5 months. That’s a pretty sizable jump. The problem is, it’s mostly cost push inflation driven by the war in Iran. Consumers will eat the price hike until they can’t. But here’s the thing – in order to get a 1970s style inflation you need a much larger boom in oil and commodities. And I mean MUCH larger. You see, in the 70s that second big jump in prices coincided with a 150% surge in oil prices after the first big surge. So, if we’re expecting inflation to go to 14% year over year (or anything remotely close to that) then you need a record breaking surge in oil prices and broader commodities on top of what we’ve already had. The equivalent sort of price action is a move to something like $300 oil. But that brings in another problem – the US economy isn’t nearly as oil dependent as it was in the 1970s. So it would take a much broader and much larger commodity rally to cause this. And it would need to be supported by some sort of underlying stimulus from global governments. None of which is completely out of the realm of possibility, but I still don’t see it in the data.

As for the date – our leading inflation index, which has been ahead of this entire move in inflation, is up to 3.4%. That’s not great and it’s well above the Fed’s target, but it’s nothing to panic over. So, I view this recent move in yields as more of an adjustment to expectations and not some sort of fundamental shift in inflation trends that portends a repeat of 2022 or the 1970s.

Speaking of bond yields – I did a small software update on our Escape Velocity Tool. This is one of my favorite bond market metrics as it measures the theoretically optimal point on the yield curve by comparing current yields and current durations. In short, when the yield equals the duration you have a level of “escape velocity” where an interest rate shock is offset by the bond’s interest over a one year period. We added a historical look at how this metric would have positioned you in the yield curve over time and also added a shock analyzer where you can change the size of the interest rate shock. Right now the optimal point on the curve is about 4.5 years, which is pretty consistent with an environment in which interest rate risk is still high, but you also don’t want to be too long or too short.

3) A Tough Fed Chair, Just in Time!

We got an official Kevin Warsh confirmation this week for new Fed Chair. It’s interesting because Warsh was notoriously hawkish in the past. And this week he was talking tough about the size of the Fed’s balance sheet. It’s funny timing because inflation is bumping up a bit and I don’t think you can justify cutting rates here. But Warsh was obviously nominated because Trump expects a more dovish Fed Chief. Gulp.

So, how is this one going to play out? Well, the good news is the Fed Chief doesn’t control the FOMC and I think the Chief would have a pretty hard time convincing all the members to vote for a cut in this sort of environment. But it’s going to be interesting to see how this one plays out in the coming months because I don’t think Warsh can fight the pressure from Trump for long. But at this point the inflation battle seems to be more in the hands of the President than anyone else. After all, if we want low future inflation during an AI boom then it seems pretty obvious that ending the Iran conflict and getting oil back to $75 is a slam dunk way to get there. And that is a decision by the Executive branch, not the FOMC.

Well, that’s all I have for you this week. As always, stay disciplined out there.

Comments

Log in or sign up to join the conversation.