Image: Bigstock

Johnson & Johnson (JNJ - Free Report) has quietly reemerged as one of the stronger-performing large-cap healthcare stocks in 2026.

After hitting fresh all-time highs of $269 a share last week, investors are turning their attention to the healthcare giant's Q2 report, which is scheduled for Wednesday, July 15, before the opening bell.

While many tech stocks continue to command premium valuations, Johnson & Johnson offers investors a combination of defensive characteristics, consistent earnings growth, a premier dividend, and one of the strongest balance sheets in corporate America.

That combination has helped fuel recent momentum, but the question now is whether another strong quarterly report can send JNJ shares even higher after spiking more than 20% year to date.

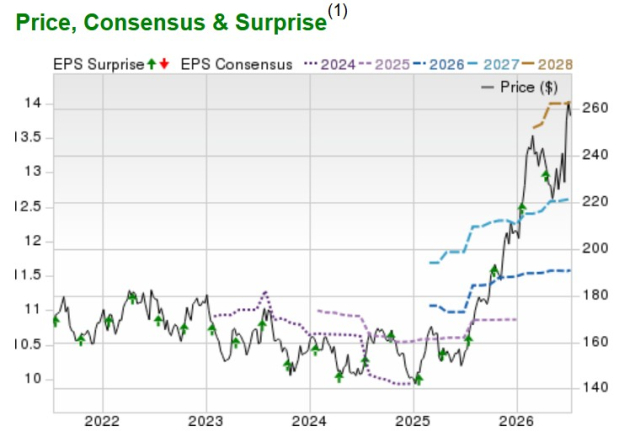

Image Source: Zacks Investment Research

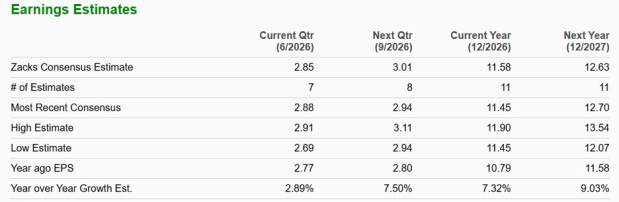

Johnson & Johnson's Q2 Expectations

Wall Street expects Johnson & Johnson to post another solid quarter despite ongoing patent headwinds across portions of its pharmaceutical portfolio.

Consensus estimates currently call for Q2 EPS of approximately $2.85 on revenue of $25.18 billion, representing modest growth of 3% and 6% from the prior-year quarter, respectively.

Investors will likely be paying close attention to several key areas:

Continued growth from the Innovative Medicine segment

Sales of blockbuster cancer therapies such as Darzalex, which continues to be one of J&J's largest growth drivers

Momentum in the MedTech business, particularly cardiovascular products

Any updates to full-year guidance following the company's stronger-than-expected first quarter

Another encouraging sign is that J&J continues to invest aggressively in future growth. Recent pipeline developments, oncology expansion, and strategic acquisitions have strengthened its long-term growth outlook while helping offset future patent expirations.

The company also has one of the longest track records of exceeding earnings expectations, with an average EPS surprise of 1.89% in its last four quarterly reports.

Image Source: Zacks Investment Research

JNJ's Valuation Still Looks Reasonable

Despite recently reaching new highs, Johnson & Johnson's valuation remains relatively attractive compared to many large-cap healthcare peers and the broader market.

JNJ currently trades at 22X forward earnings, which is slightly beneath the benchmark S&P 500 while trading near its Zacks Large Cap Pharmaceuticals Industry average of 20X.

Image Source: Zacks Investment Research

That valuation appears attractive considering the company's:

Diversified pharmaceutical portfolio

Growing medical device business

Consistent free cash flow generation

Exceptional balance sheet

Stable earnings profile

Analysts also project adjusted EPS to continue growing in the high single digits over the next two fiscal years, supporting the argument that today's valuation is supported by improving fundamentals rather than speculative enthusiasm.

For long-term investors seeking quality rather than rapid multiple expansion, JNJ still offers an attractive risk-reward profile.

Image Source: Zacks Investment Research

JNJ Remains a Dividend Powerhouse

One of JNJ's biggest investment attractions remains its dividend.

Johnson & Johnson is a Dividend King, having increased its dividend for more than six consecutive decades, making it one of the longest-running dividend growth stories in the market.

JNJ's dividend yield of 2.09% is roughly on par with its industry average and remains comfortably above the S&P 500’s 1.03% average, while being supported by:

Strong recurring cash flows

Investment-grade balance sheet

Diversified healthcare operations

Conservative payout ratio (48%)

Unlike many high-yield companies that sacrifice growth to support payouts, Johnson & Johnson has consistently demonstrated its ability to invest heavily in research, acquisitions, and innovation while continuing to reward shareholders through annual dividend increases.

For income-oriented investors, that combination of dependable dividend growth and capital appreciation potential remains difficult to match among large-cap healthcare companies.

Image Source: Zacks Investment Research

Can JNJ Stock Reach Higher Highs?

Momentum has clearly improved over the past several weeks, with investors rotating back toward high-quality defensive names as the Q2 earnings season approached.

If Johnson & Johnson delivers another earnings beat, raises guidance, or provides encouraging commentary surrounding its pharmaceutical pipeline and MedTech businesses, the stock could have room to extend its recent breakout.

Of course, expectations have also risen following the recent rally, meaning management's guidance could prove just as important as the quarterly results themselves.

Fortunately, Johnson & Johnson's diversified business model has historically allowed it to navigate economic uncertainty better than many companies, making it an appealing option for investors seeking steady long-term compounder rather than highly volatile growth stocks.

Bottom Line

Johnson & Johnson may not deliver the explosive upside of many AI leaders, but its combination of earnings consistency, reasonable valuation, industry-leading dividend growth, and improving business momentum continues to make the healthcare giant an attractive long-term holding.

A strong Q2 report could provide another catalyst for JNJ shares to push toward fresh highs, although much will depend on management's outlook for the remainder of 2026.

For now, Johnson & Johnson stock currently lands a Zacks Rank #3 (Hold), suggesting investors may want to await additional earnings estimate revisions following its upcoming Q2 report before initiating or expanding positions.

Comments

Log in or sign up to join the conversation.